THE ROLE OF GOVERNMENT IN PROMOTING ECONOMIC GROWTH

Government plays an important role in how well a country utilizes its resources in production. The policies and incentives put into place affect a country’s total factor productivity. Now we discuss some of the key ways in which government plays a role in influencing productivity.

Government as a Contributor to Physical Capital, Human Capital, and Technology

The government is the single largest consumer of goods and services in the United States. Each year, the U.S. government spends over $350 billion on purchases including highways, bridges, transportation systems, public education, military equipment, and more. By investing heavily in capital goods, the government promotes a higher level of labor productivity in the country.

Physical Capital: Public Capital and Private Investment One of the reasons why some nations are rich and others are poor lies in the different levels of infrastructure development. The focus on infrastructure means that there is something important that lies behind our aggregate production: We do not just increase capital, increase labor, improve technology, and turn a crank to obtain economic growth.

infrastructure The public capital of a nation, including transportation networks, power-

Infrastructure is defined as a country’s public capital. It includes dams, roads, and bridges; transportation networks, such as air and rail lines; power-

The government also encourages private investment in physical capital through tax incentives and other subsidies to firms willing to invest in capital projects. Industries that receive the largest tax incentives include aerospace, defense, energy, and telecommunications.

493

Human Capital: Public Education and Financial Aid The government plays an important role in ensuring that every person has access to a minimum level of education. In the United States, state laws mandate that children stay in school until a minimum age, typically 16. Public schools and universities are highly subsidized by local and state governments to provide affordable access to educational opportunities.

Besides providing funding directly to schools and universities, the government offers various forms of financial assistance directly to students to use toward educational expenses. These include Pell Grants and the G.I. Bill, federal subsidized loans, and various types of tax incentives that allow qualified students (or their parents) to deduct a portion of their tuition and fees from their taxable income or from their taxes directly. The government also allows teachers to deduct certain expenses from their taxes, and provides tax-

Technology: Government R&D Centers and Federal Grants Some of the largest research centers in the country are government funded. These include Los Alamos National Laboratory and Sandia National Laboratories (part of the Department of Energy), the National Institutes of Health, the National Aeronautics and Space Administration (NASA), and the National Oceanic and Atmospheric Administration (NOAA), just to name a few. These government research centers employ thousands of scientists, researchers, and doctors for the purpose of advancing knowledge and inventing products that enhance the lives of all citizens and promote economic growth.

In addition to running research centers, the government provides funds directly to public and private research centers as well as to individual researchers. Among the largest grantors of funds is the National Science Foundation (NSF), founded in 1950. In 2016, the NSF provided over $7 billion in grants to around 11,000 projects, and has maintained its mission of promoting research essential for the nation’s economic health and global competitiveness.

Government as a Facilitator of Economic Growth

A second major role of government in promoting economic growth is to ensure that an effective legal system is in place to enforce contracts and to protect property rights, and that the financial system is kept stable. These are the less tangible yet equally important components of a country’s infrastructure.

Enforcement of Contracts The legal enforcement of contract rights is an important component of an infrastructure that promotes economic growth and well-

Protection of Property Rights A stable legal system that protects property rights is essential for economic growth. Many developing countries do not systematically record the ownership of real property: land and buildings. Although ownership is often informally recognized, without express legal title, the capital locked up in these informal arrangements cannot be used to secure loans for entrepreneurial purposes. As a result, valuable capital sits idle; it cannot be leveraged for other productive purposes.

In addition, a legal system that recognizes and protects ideas (or intellectual property) is critical to encouraging innovation. Common legal protections for ideas include patents (for inventions), copyrights (for written works, music, and film), and trademarks (for names and symbols). Every country has its innovators; the question is whether these people are offered enough of an incentive to devote their efforts to develop the innovations that drive economic growth. The extent to which countries establish intellectual property rights varies, and even when such protections exist, enforcement of the protections varies.

494

Stable Financial System Another important component of a nation’s infrastructure is a stable and secure financial system. Such a financial system keeps the purchasing power of the currency stable, facilitates transactions, and permits credit institutions to arise. The recent global financial turmoil is an example of the problems caused by financial instability. Further, bank runs, like those that caused major economic disruption in Uruguay and Argentina in 2001–

Unanticipated inflations or deflations are both detrimental to economic growth. Consumers and businesses rely on the monetary prices they pay for goods and services for information about the state of the market. If these price signals are constantly being distorted by inflation or deflation, the quality of business and consumer decisions suffers. Unanticipated price changes further lead to a redistribution of income between creditors and debtors. Financial instability is harmful to improving standards of living and generating economic growth.

Government as a Promoter of Free and Competitive Markets

A third role of government in promoting economic growth is maintaining competitive and efficient markets and the freedom for firms and individuals to pursue their interests.

Competitive Markets and Free Trade One of the challenges of government is choosing the right mix of policies to keep markets competitive and fair. Regulations are put into place to protect various interests, whether consumer welfare, worker rights and safety, or the environment. But government also must ensure that such regulations do not stand in the way of markets operating efficiently.

Competitive markets refer to the ability of firms to open and close businesses without unnecessary restrictions or other burdens. Also important is free trade, which refers to the ability to buy and sell products with other countries without significant barriers such as tariffs or quotas. Allowing the market to function freely within the confines of sensible regulatory laws generally creates more potential for economic growth.

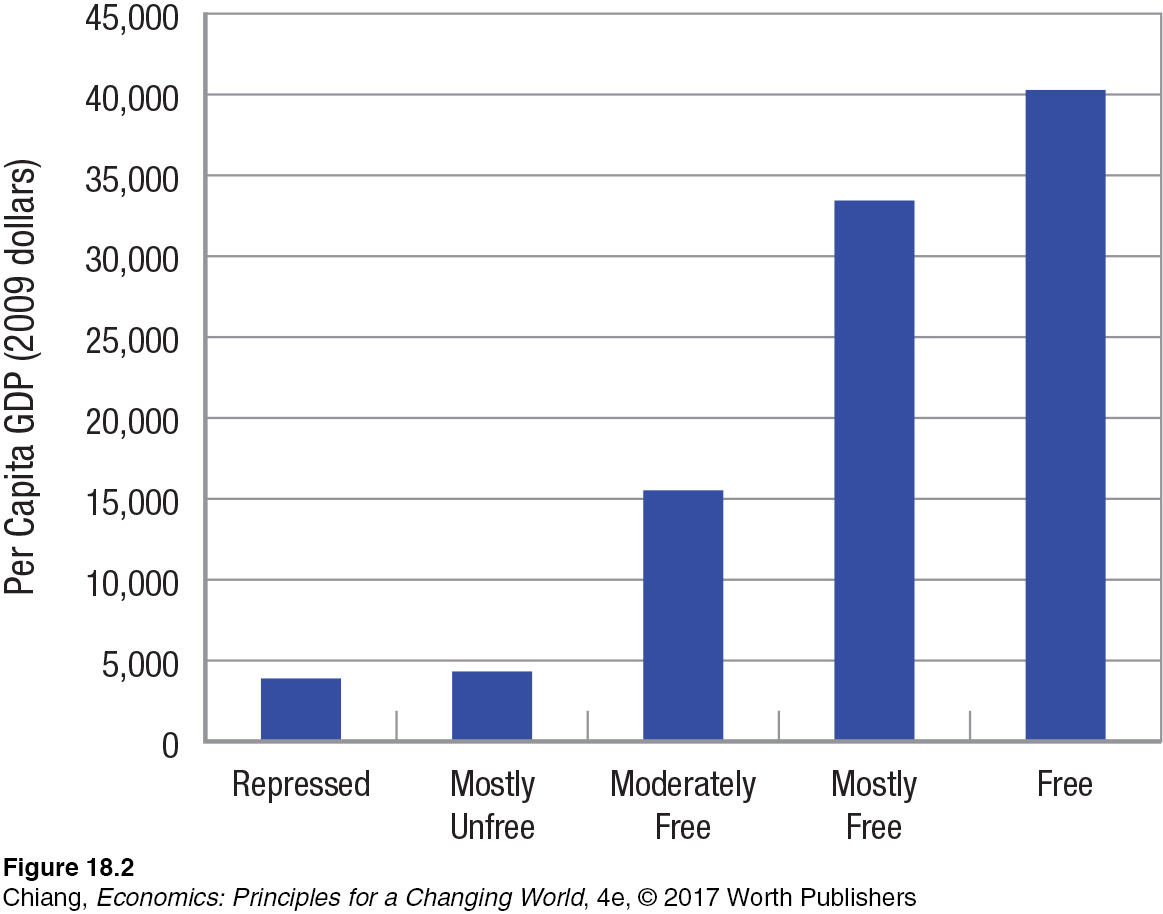

Economic Freedom One of the measures used to gauge the ability of individuals and businesses to make investment and production decisions freely is the Index of Economic Freedom.

Unlike physical infrastructure such as roads and dams, which are easy to measure, attempting to measure the intangibles of doing business often requires subjective judgments. One reasonably objective measure is the 2016 Index of Economic Freedom.1 This index incorporates information about freedoms in ten categories: business, trade, fiscal policy, government size, monetary policy, investment, finance, property rights, corruption, and labor.

1 Heritage Foundation, 2016 Index of Economic Freedom (Washington, D.C.), 2016.

Clearly, assigning some of these items a numeric value requires a bit of subjective judgment. Even so, this index is one reasonable approach to measuring the overall infrastructure of a country.

Figure 2 portrays the relationship between economic freedom and per capita GDP measured by purchasing power parity (what income will buy in each country). Those nations with the most economic freedom have the highest per capita GDP and also the highest growth rates (not shown).

In this chapter, we have seen that economic growth in the long run comes from improvements in labor productivity, increases in capital, or improvements in technology. Investments in human capital and greater economic freedom also lead to higher growth rates and higher standards of living.

495

ISSUE

Did Economic Growth Peak a Century Ago? Prospects for Future Growth

When one thinks of life just 15 years ago, imagine what has changed. GPS technology was nearly nonexistent, digital music was in its infancy and downloaded using very slow Internet connections, and smartphones and tablets didn’t exist, at least in the way we know these products today. Certainly, life has changed from how we lived at the start of the new millennium. But was this a true transformation of our standard of living? According to one economist, the technological advances of the past few decades do not compare with the effect that inventions over a century ago had. In fact, he argues that U.S. economic growth peaked nearly a century ago. Are prospects for future growth in trouble?

Robert Gordon is a distinguished macroeconomist and economic historian who is skeptical about the technological “revolution” that has resulted from the development of the Internet and social media. In his book The Rise and Fall of American Growth, he argues that the true transformation of American standards of living occurred between 1870 and 1940. He argues that the tremendous period of growth a century ago may be a one-

He points to the five “great inventions,” which were (1) electric lights, (2) flush toilets, (3) chemicals and pharmaceuticals, (4) cars, and (5) the telephone. Each of these inventions occurred prior to 1940. Therefore, Gordon argues that life became modernized by the 1940s, and every invention since, while making life more comfortable, has not had the same effect. He makes the point that if a person today walked into a 1940s apartment, it would be functional, with indoor plumbing, lights, a refrigerator, and a telephone. But if a person from 1940 walked into an 1870s apartment, the same could not be said.

Is Gordon’s pessimistic view on future growth accurate? Only time will tell whether recent and future inventions will measure up to those of a century ago. What would be the contenders of the new “great inventions”? The obvious choices would include personal computers, Internet, social media, biotechnology, and artificial intelligence. But have these inventions been so transformative to our lives that living without them would be as burdensome as living without lights or the modern toilet? It’s a powerful thought to ponder as one considers the factors that will lead to future growth and the factors that will challenge it.

Prospects for future growth depend largely on the willingness of businesses to innovate and create new products, on the willingness of consumers to demand these new products, and on the willingness of government (and the people who elect policymakers) to foster an environment that promotes long-

Generating another strong and sustained period of growth will not be easy. First, many countries including the United States today face debt problems as populations rise and as people live longer. As a result, investing in long-

In the long run, all of these factors generate growth and higher standards of living. Yet, what are we to do if the economy collapses in the short run? The Great Depression of the 1930s was to prove that for a reasonably long period (a decade), the economy could be mired in a slowdown with high unemployment rates and negative growth. A deep economy-

496

CHECKPOINT

THE ROLE OF GOVERNMENT IN PROMOTING ECONOMIC GROWTH

Government has an important role in promoting economic growth by providing physical and human capital, ensuring a stable legal system and financial markets, and promoting free and competitive markets.

Infrastructure is a country’s public capital, including dams, roads, transportation networks, power-

generating plants, and public schools. Governments provide capital and technology by purchasing public capital and providing incentives for private investment, supporting education through subsidies and financial aid, and supporting research with grants.

Other less tangible infrastructure elements include protection of property rights, enforcement of contracts, and a stable financial system.

The Index of Economic Freedom measures a country’s infrastructure, which supports economic growth.

QUESTIONS: Imagine a country with a “failed government” that can no longer enforce the law. Contracts are not upheld and lawlessness is the order of the day. How well could an economy operate and grow in this environment?

Answers to the Checkpoint questions can be found at the end of this chapter.

Not very well. Large-