USING CONSUMER AND PRODUCER SURPLUS: THE GAINS FROM TRADE

Markets are efficient when they generate the largest possible amount of net benefits to all parties involved. When transactions between a buyer and a seller take place, each party is better off than before the transaction, leading to gains from trade. We had previously looked at gains from trade in an earlier chapter from the perspectives of individuals, firms, and countries specializing in activities and engaging in mutually beneficial transactions. This is no different than our present market examples, in which buyers and sellers mutually gain from transacting with one another.

total surplus The sum of consumer surplus and producer surplus, and a measure of the overall net benefit gained from a market transaction.

At the equilibrium price, shortages and surpluses are nonexistent, and all consumers wanting to buy a good at that price are able to find a seller willing to sell at that price. The market efficiency that results maximizes the sum of consumer surplus and producer surplus, referred to as total surplus. Total surplus is a measure of the total net benefits a society achieves when both consumers and producers are valued components of an economy.

To see why markets are efficient at equilibrium, we need to analyze what happens to total surplus when markets deviate from equilibrium.

The Consequences of Deviating From Market Equilibrium

The market mechanism ensures that goods and services get to where they are most needed, because consumers desiring them bid up the price, while suppliers eager to make money supply them. Adam Smith termed this process the invisible hand to describe how resources are allocated efficiently through individual decisions made in markets.

But not all markets end up in equilibrium, especially if buyers or sellers hold inadequate information about products, or if buyers or sellers hold unrealistic or inaccurate expectations about market prices and behavior. Let’s examine two scenarios in the market for treadmills in which prices deviate from the equilibrium price.

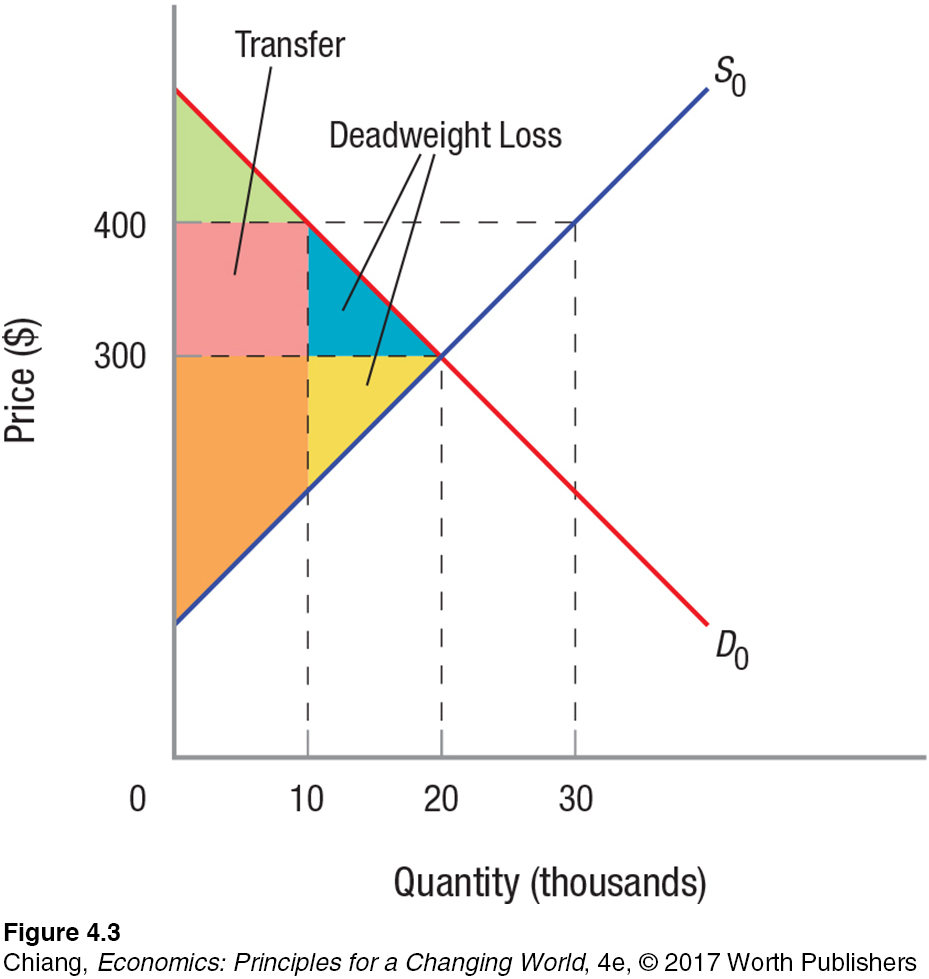

When Prices Exceed Equilibrium Figure 3 illustrates a market for treadmills with an equilibrium price of $300. Suppose that due to unrealistic expectations of demand, prices for treadmills are set at $400, above the equilibrium price. We know from the previous chapter that a price above equilibrium leads to excess supply, because consumers only demand 10,000 units while producers desire to sell 30,000. Our tools of consumer surplus and producer surplus allow us to evaluate the effects on buyers and sellers in this market.

When prices are above equilibrium, consumer surplus shrinks due to two effects. First, a price of $400 causes some consumers to not make a purchase, because these consumers were only willing to pay between $300 and $400. The area shown in blue represents the lost consumer surplus from these forgone purchases. Second, the consumers who still are willing and able to purchase a unit pay $100 more, which represents a loss in consumer surplus equal to the pink area. In sum, the pink and blue regions represent the total reduction in consumer surplus from the higher price.

Producers, on the other hand, will likely benefit from the higher price but face two opposing effects. First, the fact that the higher price causes some consumers to not purchase a unit causes a loss in producer surplus equal to the yellow area. However, this is offset by the additional money earned from the consumers who buy the unit at the higher price, which is represented by the pink area.

deadweight loss The reduction in total surplus that results from the inefficiency of a market not in equilibrium.

Therefore, the pink area represents a transfer of surplus from consumers to producers. The blue and yellow areas represent deadweight loss, the loss of consumer surplus and producer surplus caused by the inefficiency of a market not operating at equilibrium. Nobody gets the blue and yellow areas. Deadweight loss represents a loss in total surplus, because both buyers and sellers would have benefited from these transactions.

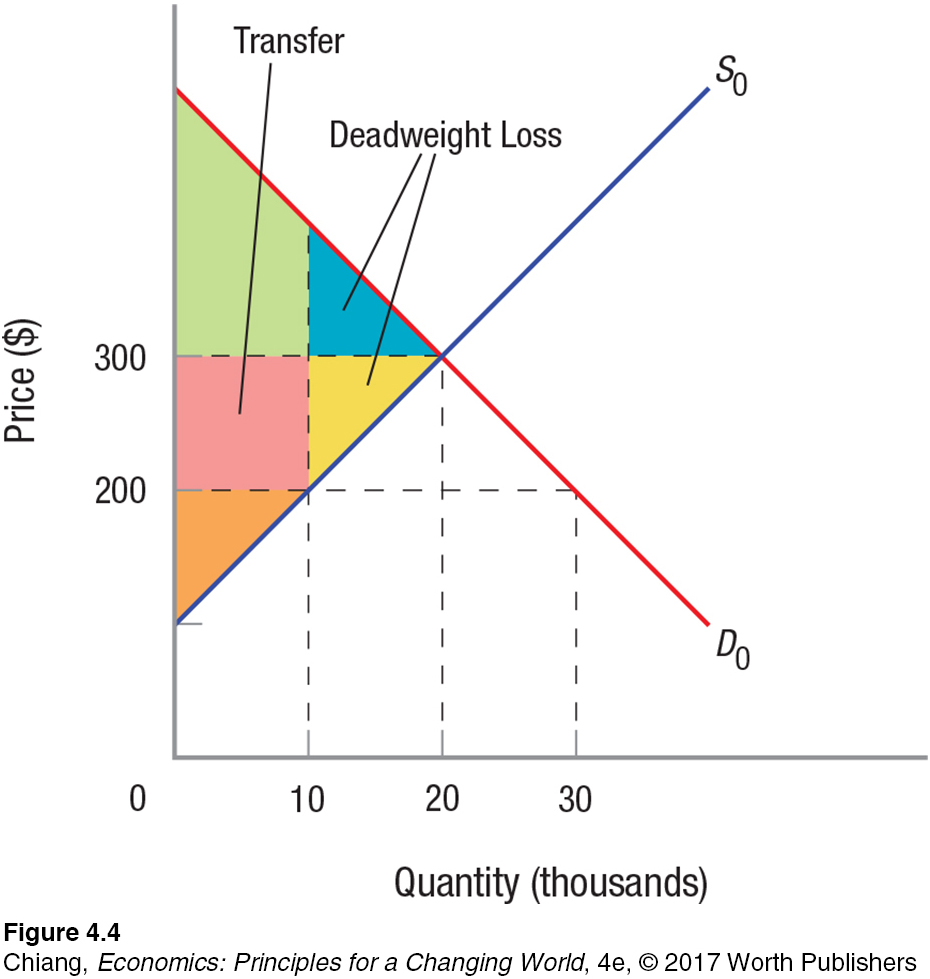

When Prices Fall Below Equilibrium When prices are below equilibrium, the opposite effects happen as a result of a shortage. Figure 4 shows the market for treadmills in which the price of $200 is below the equilibrium price. At that price, sellers provide 10,000 units for sale, while buyers demand 30,000 units, causing a shortage.

At a price of $200, producers are clearly worse off. Some producers are unable to sell at that low price, causing a loss of producer surplus equal to the yellow area, while those who still sell the product earn $100 less per unit, resulting in a loss of producer surplus equal to the pink area.

At first, you might believe consumers are better off with the lower price, and some in fact are. But these gains, shown by the pink area, are limited to consumers lucky enough to purchase the good. The rest of the consumers who are affected by the shortage are worse off, because consumer surplus equal to the blue area is lost because of trades never made. In sum, deadweight loss equal to the blue and yellow areas results.

The two scenarios shown in Figures 3 and 4 demonstrate that whenever prices deviate from equilibrium, total surplus as measured by the sum of consumer surplus and producer surplus falls, resulting in a deadweight loss from mutually beneficial transactions between buyers and sellers not taking place. But why would markets not achieve equilibrium? Sometimes a market will fail to achieve equilibrium because it is prevented from doing so on its own.

PAUL A. SAMUELSON (1915–2009)

NOBEL PRIZE

In 1970 Paul Samuelson became the first American to win the Nobel Prize in Economics. One could say that Paul Samuelson literally wrote the book on economics. In 1948, when he was a young professor at the Massachusetts Institute of Technology, the university asked him to write a text for the junior-

Samuelson’s interests were wide ranging, and his contributions include everything from the highly technical and mathematical to a popular column for Newsweek magazine. He made breakthrough contributions to virtually all areas of economics.

Born in Gary, Indiana, in 1915, Samuelson attended the University of Chicago. He received the university’s Social Science Medal and was awarded a graduate fellowship, which he used at Harvard, where he published eleven papers while in the graduate program.

He wanted to remain at Harvard, but was only offered an instructor’s position. However, MIT soon made a better offer and, as he describes it, “On a fine October day in 1940 an enfant terrible emeritus packed up his pencil and moved three miles down the Charles River, where he lived happily ever after.” He often remarked that a pencil was all he needed to theorize. Seven years later, he published his Ph.D. dissertation Foundations of Economic Analysis, a major contribution to the area of mathematical economics.

Harvard made several attempts to lure him back, but he spent his entire career at MIT and is often credited with developing a department as good as or better than Harvard’s. Samuelson was an informal adviser to President John F. Kennedy. A prolific writer, his Collected Works takes up five volumes and includes more than 350 articles. He was an active economist until his death in 2009 at the age of 94. As you read through this book, keep in mind that in virtually every chapter, Paul Samuelson created or added to the analysis in substantial ways.

Sources: David Warsh, Knowledge and the Wealth of Nations: A Story of Economic Discovery (New York: Norton), 2006; Paul Samuelson, “Economics in My Time,” in William Breit and Roger Spencer, Lives of the Laureates: Seven Nobel Economists (Cambridge, MA: MIT Press), 1986.

Market Failure

market failure Occurs when a free market does not lead to a socially desirable outcome.

Markets are inherently efficient mechanisms for allocating resources because of the incentives that drive consumers and firms to act in their own best interests. But like all things, exceptions occur when circumstances prevent the market from achieving the socially desirable outcome. When freely functioning markets fail to provide an optimal amount of goods and services, a market failure occurs.

There are four major reasons why markets fail: a lack of competition, a mismatch of information, external benefits or costs, and the existence of public goods. Each causes total surplus to fall, and deadweight loss to appear.

Lack of Competition When a market has many buyers and sellers, no one seller has the ability to raise its price above that of its competitors. But when a market lacks competition, a firm can raise its price in the market without worrying that other firms will undercut its price. For example, in most communities the local water provider is a firm that lacks competition. This can lead to inefficient production and higher prices unless the market failure is corrected using government regulation.

asymmetric information Occurs when one party to a transaction has significantly better information than another party.

Information Is Not Shared by All Parties An important condition for efficient markets is that buyers and sellers must possess adequate information about products. Sometimes, one party knows more about a product than the other, a situation known as asymmetric information. For example, a seller of a used car knows more about the true condition of the car than a potential buyer. Conversely, an art or antiques buyer may know more about the value of items than the seller at an estate sale. In these cases, a mismatch of information may lead to prices being set too high or too low.

Singapore: Resolving Traffic Jams and Reducing Pollution Using Price Controls

How did Singapore use economic tools to intervene in the market to improve traffic flow and to correct a potential market failure?

How much time is spent waiting in gridlock traffic in major cities? According to a study by the transportation analytics firm INRIX, in 2015, American drivers spent 8 billion hours stuck in traffic. Traffic creates an opportunity cost that leads to reduced productivity. Moreover, traffic jams reduce fuel efficiency and generate more air pollution. Is there an economic solution to these problems? Singapore may have the answer.

Singapore uses an electronic road-

Singapore is not the only city that uses congestion charges. It costs approximately $15 to drive in Central London between the hours of 7 A.M. and 6 P.M. Even in the United States, the introduction of express lanes in Los Angeles, Atlanta, Miami, and other cities has allowed motorists to pay a toll to bypass traffic. Similar to Singapore, these tolls vary throughout the day, with prices rising as roads become more congested.

Not only do congestion charges incentivize people to drive less; they also encourage companies to change the way they operate. Companies that do not need to operate during traditional business hours might encourage their employees to arrive at work later and return home later, avoiding times when congestion charges are at their peak. By reducing traffic congestion, less time is wasted, productivity rises, and pollution is reduced. Furthermore, the fees collected are a valuable source of government revenue.

Many economists believe that market-

GO TO  TO PRACTICE THE ECONOMIC CONCEPTS IN THIS STORY

TO PRACTICE THE ECONOMIC CONCEPTS IN THIS STORY

The Existence of External Benefits or Costs When you drive your car on a crowded highway, you inflict external costs on other drivers by adding to congestion. When you receive a flu shot, you confer external benefits on the rest of us by reducing the chances of spreading an illness. Markets rarely produce the socially optimal output when external costs or benefits are present. When deciding whether to drive or obtain a flu shot, you tend not to think of the costs and benefits you impose on others. As a result, more people drive and fewer people receive flu shots than would be ideal to achieve the socially optimal outcome.

The Existence of Public Goods Most goods we buy are private goods, such as meals and concert tickets; once we buy them, no one else can benefit from them. Public goods, however, are goods that one person can consume without diminishing what is left for others. Public television, for example, is a public good that illustrates nonrivalry (my watching of PBS does not mean there is less PBS for you to watch) and nonexclusivity (once a good is provided, others cannot be excluded from enjoying it). Because of these characteristics, public goods are difficult to provide in the private market.

Market Efficiency Versus Equity

Reducing the effects of market failure is an important goal of government, which can enact policies to address markets in which private transactions do not lead to the optimal outcome. But the role of government extends beyond that of achieving social efficiency. It is also tasked with the goal of achieving equity in markets. For example, is it fair when teachers or firefighters who earn modest salaries are unable to afford market rents for apartments, or when a single parent working full time is unable to earn enough to avoid poverty? If a policy creates considerable unfairness, while spurring only a small gain in efficiency, some other policy might be better. One tool used by government to balance efficiency with equity is price controls, which we turn to next.

CHECKPOINT

USING CONSUMER AND PRODUCER SURPLUS: THE GAINS FROM TRADE

The sum of consumer surplus and producer surplus is total surplus, a measure of the overall net benefit for an economy.

Markets are efficient when all buyers and all sellers willing to buy and sell at the market price are able to do so.

When buyers and sellers engage in a market transaction, gains from trade are created from consumer surplus and producer surplus.

Total surplus is maximized at a market equilibrium.

Deadweight loss is created when markets deviate from equilibrium.

Markets are typically efficient, although sometimes they can fail by not providing the socially optimal amount of goods and services.

Market failure is caused by a lack of competition, mismatched information, external costs and external benefits, or the existence of public goods.

QUESTION: Waiting for an organ transplant is an ordeal for patients. Some wait years for a compatible donor organ to become available. Some economists have suggested that offering monetary compensation to organ donors would increase the supply of available organs. Would such a system lead to gains from trade? Why are such incentives difficult to implement?

Answers to the Checkpoint questions can be found at the end of this chapter.

Although many people voluntarily become organ donors because of the goodwill they feel knowing that their actions can potentially save a life, still many others choose not to become organ donors because they do not see any monetary benefit from doing so. Compensating individuals for becoming organ donors, thereby raising the “price” of organs, would be a way to increase the supply of organs, allowing the shortage to dissipate until equilibrium is reached. In doing so, organ donors and recipients both benefit, resulting in gains from trade. However, moral objections to selling body parts have led to many laws preventing organ donors from being compensated. As a result, shortages continue to be a problem.