4.1 CHAPTER REVIEW

FACTS AND TOOLS

Question 4.11

1. If the price in a market is above the equilibrium price, does this create a surplus or a shortage?

Question 4.12

2. When the price is above the equilibrium price, does greed (in other words, self-interest) tend to push the price down or up?

Question 4.13

3. Jon is on eBay, bidding for a first edition of the influential Frank Miller graphic novel Batman: The Dark Knight Returns. In this market, who is Jon competing with: the seller of the graphic novel or the other bidders?

Question 4.14

4. Now, Jon is in Japan, trying to get a job as a full-time translator; he wants to translate English TV shows into Japanese and vice versa. He notices that the wage for translators is very low. Who is the “competition” pushing the wage down: Does the competition come from businesses who hire the translators or from the other translators?

Question 4.15

5. Jules wants to purchase a Royale with cheese from Vincent. Vincent is willing to offer this tasty burger for $3. The most Jules is willing to pay for the tasty burger is $8 (after all, his girlfriend is a vegetarian, so he doesn’t get many opportunities for tasty burgers).

How large are the potential gains from trade if Jules and Vincent agree to make this trade? In other words, what is the sum of producer and consumer surplus if the trade happens?

If the trade takes place at $4, how much producer surplus goes to Vincent? How much consumer surplus goes to Jules?

If the trade takes place at $7, how much producer surplus goes to Vincent? How much consumer surplus goes to Jules?

Question 4.16

6. What happened in Vernon Smith’s lab? Choose the right answer:

The price and quantity were close to equilibrium but gains from trade were far from the maximum.

The price and quantity were far from equilibrium and gains from trade were far from the maximum.

The price and quantity were far from equilibrium but gains from trade were close to the maximum.

The price and quantity were close to equilibrium and gains from trade were close to the maximum.

Question 4.17

7. When supply falls, what happens to quantity demanded in equilibrium? (This should get you to notice that both suppliers and demanders change their behavior when one curve shifts.)

Question 4.18

8.

When demand increases, what happens to price and quantity in equilibrium?

When supply increases, what happens to price and quantity in equilibrium?

When supply decreases, what happens to price and quantity in equilibrium?

When demand decreases, what happens to price and quantity in equilibrium?

Question 4.19

9.

When demand increases, what happens to price and quantity in equilibrium?

When supply increases, what happens to price and quantity in equilibrium?

When supply decreases, what happens to price and quantity in equilibrium?

When demand decreases, what happens to price and quantity in equilibrium?

No, this is not a mistake. Yes, it is that important.

Question 4.20

10. What’s the best way to think about the rise in oil prices in the 1970s, when wars and oil embargoes wracked the Middle East? Was it a rise in demand, a fall in demand, a rise in supply, or a fall in supply?

Question 4.21

11. What’s the best way to think about the rise in oil prices in the last 10 years, as China and India have become richer: Was it a rise in demand, a fall in demand, a rise in supply, or a fall in supply?

THINKING AND PROBLEM SOLVING

Question 4.22

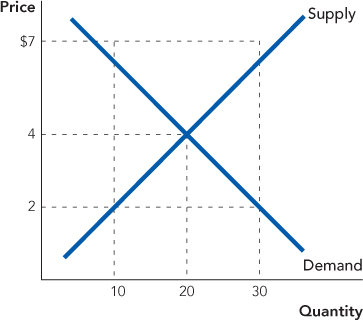

1. Suppose the market for batteries looks as follows:

What are the equilibrium price and quantity?

Question 4.23

2. Consider the following supply and demand tables for bread. Draw the supply and demand curves for this market. What are the equilibrium price and quantity?

|

Price of One Loaf |

Quantity Supplied |

Quantity Demanded |

|---|---|---|

|

$0.50 |

10 |

75 |

|

$1 |

20 |

55 |

|

$2 |

35 |

35 |

|

$3 |

50 |

25 |

|

$5 |

60 |

10 |

Question 4.24

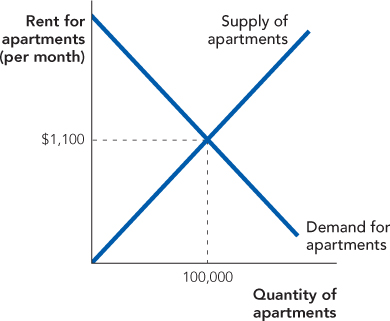

3. If the price of a one-bedroom apartment in Washington, D.C., is currently $1,000 per month, but the supply and demand curves look as follows, then is there a shortage or surplus of apartments? What would we expect to happen to prices? Why?

Question 4.25

4. Determine the equilibrium quantity and price without drawing a graph.

|

Price of Good X |

Quantity Supplied |

Quantity Demanded |

|---|---|---|

|

$22 |

100 |

225 |

|

$25 |

115 |

200 |

|

$30 |

130 |

175 |

|

$32 |

150 |

150 |

|

$40 |

170 |

110 |

Question 4.26

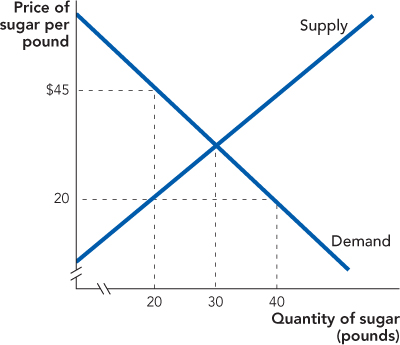

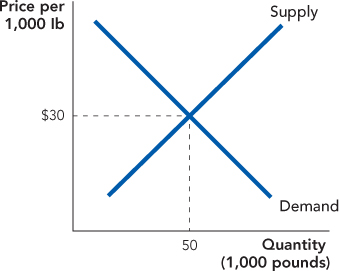

5. In the following figure, how many pounds of sugar are sellers willing to sell at a price of $20? How much is demanded at this price? What is the buyer’s willingness to pay when the quantity is 20 pounds? Is this combination of $20 per pound and a quantity of 20 pounds an equilibrium?

If not, identify the unexploited gains from trade.

Question 4.27

6. The market for marbles is represented in the graph. What is the total producer surplus? The total consumer surplus? What are the total gains from trade?

Question 4.28

7. Suppose you decided to follow in Vernon Smith’s footsteps and conducted your own experiment with your friends. You give out 10 cards: 5 cards to buyers with the figures for willingness to pay of $1, $2, $3, $4, and $5, and 5 cards to sellers with the amounts for costs of $1, $2, $3, $4, and $5. The rules are the same as Vernon Smith implemented.

Draw the supply and demand curves for this market. At a price of $3.50, how many units are demanded? And supplied?

Assuming the market works as predicted, and the market moves to equilibrium, will the buyer who values the good at $1 be able to purchase? Why or why not?

Question 4.29

8. If the price of margarine decreases, what happens to the demand for butter? What happens to the equilibrium quantity and price for butter? What would happen if butter and margarine were not substitutes? Use a supply and demand diagram to support your answer.

Question 4.30

9. The market for sugar is diagrammed:

What would happen to the equilibrium quantity and price if the wages of sugar cane harvesters increased?

What if a new study was published that emphasized the negative health effects of consuming sugar?

Question 4.31

10. If a snowstorm was forecast for the next day, what would happen to the demand for snow shovels? Is this a change in quantity demanded or a change in demand? This shift in the demand curve would affect the price; would this cause a change in quantity supplied or a change in supply?

Question 4.32

11. In recent years, the Paleo diet, which emphasized eating more meat and fewer grains, became very popular. What do you suppose that did to the price and quantity of bread? Use supply and demand analysis to support your answer.

Question 4.33

12. In recent years, there have been news reports that toys made in China are unsafe. When those news reports show up on CNN and Fox News, what probably happens to the demand for toys made in China? What probably happens to the equilibrium price and quantity of toys made in China? Are Chinese toymakers probably better or worse off when such news comes out?

Question 4.34

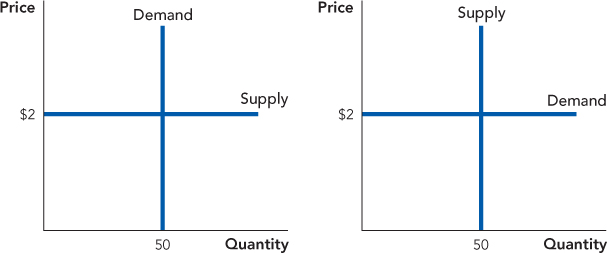

13. Here’s a quick problem to test whether you really understand what producer surplus and consumer surplus mean, rather than just relying on the geometry of demand and supply. For each of the two diagrams to the right, calculate producer surplus, consumer surplus, and total surplus. Assume the curves are perfectly vertical and perfectly horizontal.

Question 4.35

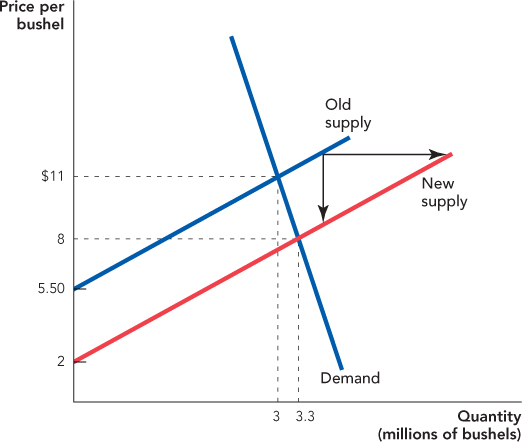

14. The diagram shows the market for agricultural products. The shift from the old supply curve to the new supply curve is the result of technological and scientific advances in farming, including the production of more resilient and productive seeds. Calculate the change in consumer surplus and the change in producer surplus caused by these technological advances. Are buyers better or worse off as a result of these advancements? What about sellers? (Note that you cannot calculate consumer surplus directly with the information given in the diagram, but you don’t need that information to calculate the change in consumer surplus.)

Question 4.36

15. Now that you’ve mastered interpreting shifts in demand and supply, it’s time to add another wrinkle: simultaneous shifts in both demand and supply. Most of the time, when we explore simultaneous shifts of demand and supply, we can determine the impact on either equilibrium price or equilibrium quantity, but not both. Fill in the missing cells in the following table to see why. Because two curves can shift in two directions, there are four cases to consider. The first column is done for you as an example.

|

|

Case 1 |

Case 2 |

Case 3 |

Case 4 |

|---|---|---|---|---|

|

Change in demand |

Increase |

Increase |

Decrease |

Decrease |

|

How demand change affects price |

↑ |

|

|

|

|

How demand change affects quantity |

↑ |

|

|

|

|

Change in supply |

Increase |

Decrease |

Increase |

Decrease |

|

How supply change affects price |

↓ |

|

|

|

|

How supply change affects quantity |

↑ |

|

|

|

|

Combined effect of demand and supply on price |

? |

|

|

|

|

Combined effect of demand and supply on quantity |

↑ |

|

|

|

Question 4.37

16. In the last problem, you saw how simultaneous shifts in demand and supply can leave us with uncertainty about the impact on price or on quantity. An increase in both demand and supply will increase equilibrium quantity but have an ambiguous effect on equilibrium price. However, if we knew that there was a significant increase in demand and only a small increase in supply, we could conclude that the price would probably rise overall, albeit not by as much as would have been the case if supply had not increased slightly.

In each of the following examples, there are a major event and a minor event. Determine whether each change relates to demand or to supply, and then figure out the impact on price and quantity; be sure to say something about the relative magnitudes of the price and quantity changes.

Market: Rock salt

Major event: A bitterly cold and unusually snowy winter season has significantly depleted the amount of available rock salt.

Minor event: There is another snow storm, and roads and sidewalks need to be salted.

Market: Smartphones

Major event: The proliferation of fast, reliable, affordable (or free) wi-fi and cellular signals increases the usability of smartphones.

Minor event: The production of smartphones is marked by modest technological advances.

Page 66Market: Canned tomatoes

Major event: A large canned tomato manufacturer begins to use cheap imported tomatoes from Mexico rather than domestic tomatoes.

Minor event: This causes a public relations fiasco, resulting in an organized effort to boycott canned tomatoes.

CHALLENGES

Question 4.38

1. For many years, it was illegal to color margarine yellow (margarine is naturally white). In some states, margarine manufacturers were even required to color margarine pink! Who do you think supported these laws? Why? (Hint: Your analysis in question 8 from the previous section is relevant!)

Question 4.39

2. Think about two products: “safe cars” (a heavy car such as a BMW 530xi with infrared night vision, four-wheel antilock brakes, and electronic stability control) and “dangerous cars” (a lightweight car such as _____ [name removed for legal reasons, but you can fill in as you wish]).

Are these two products substitutes or complements?

If new research makes it easier to produce safe cars, what happens to the supply of safe cars? What will happen to the equilibrium price of safe cars?

Now that the price of safe cars has changed, how does this impact the demand for dangerous cars?

Now let’s tie all these links into one simple sentence:

In a free market, as engineers and scientists discover new ways to makes cars safer, the number of dangerous cars sold will tend to ______.

Question 4.40

3. Many clothing stores often have clearance sales at the end of each season. Using the tools you learned in this chapter, can you think of an explanation why?

Question 4.41

4.

If oil executives read in the newspaper that massive new oil supplies have been discovered under the Pacific Ocean but will likely only be useful in 10 years, what is likely to happen to the supply of oil today? What is the likely equilibrium impact on the price and quantity of oil today?

If oil executives read in the newspaper that new solar-power technologies have been discovered but will likely only become useful in 10 years, what is likely to happen to the supply of oil today? What is the likely equilibrium impact on the price and quantity of oil today?

What’s the short version of these scenarios? Fill in the blank: If we learn today about promising future energy sources, today’s price of energy will ____ and today’s quantity of energy will _________.

Question 4.42

5. Economists often say that prices are a “rationing mechanism.” If the supply of a good falls, how do prices “ration” these now-scarce goods in a competitive market?

Question 4.43

6. When the crime rate falls in the area around a factory, what probably happens to wages at that factory?

Question 4.44

7. Let’s take the idea from the previous question and use it to explain why businesses sometimes try to make their employees happy. If a business can make a job seem fun (by offering inexpensive pizza lunches) or at least safe (by nagging the city government to put police patrols around the factory), what probably happens to the supply of labor? What happens to the equilibrium wage if a factory or office or laboratory becomes a great place where people “really want to work”? How does this explain why the hourly wage for the typical radio or television announcer is only $13 per hour, lower than almost any other job in the entertainment or broadcasting industry?

WORK IT OUT

Consider the following supply and demand tables for milk. Draw the supply and demand curves for this market. What are the equilibrium price and quantity?

|

Price of One Gallon |

Quantity Supplied |

Quantity Demanded |

|---|---|---|

|

$1 |

20 |

150 |

|

$2 |

40 |

110 |

|

$4 |

70 |

70 |

|

$6 |

100 |

50 |

|

$10 |

120 |

20 |