The Role of Intermediaries: Banks, Bonds, and Stock Markets

Financial intermediaries such as banks, bond markets, and stock markets reduce the costs of moving savings from savers to borrowers and investors.

Equilibrium in the market for loanable funds does not come about automatically. Savers move their capital, sometimes around the world, to find the highest returns. Entrepreneurs invest time and energy to find the right investments and the right loans. Equilibrium is brought about with the assistance of financial intermediaries such as banks, bond markets, and stock markets.

Financial intermediaries reduce the costs of moving savings from savers to borrowers and help mobilize savings toward productive uses. At its core, a financial intermediary is an institution that helps to bring about the equilibrium in Figure 9.6 and to direct resources to more highly valued uses.

Banks

In their role as financial intermediaries, banks receive savings from many individuals, pay them interest, and then loan these funds to borrowers, charging them interest. Banks earn profit by charging more for their loans than they pay for the savings. To earn this money, they must provide useful “middleman” services by evaluating investments and spreading risk.

Imagine that you, as a bank depositor, had to decide which companies were worth lending money to. Is this guy Fred Smith with his FedEx idea a genius or a kook? Banks don’t always get it right, but by specializing in loan evaluation, they have a better idea than most of us of which business ideas make sense. When banks specialize, individual savers don’t have to evaluate which factories ought to be built or which businesses deserve to be supported.

Even if individuals could evaluate business ideas, it would be wasteful if every saver spent time evaluating the same business. Imagine that a business needs a million dollar loan. One thousand savers are each willing to lend the business $1,000. If each saver spent a day evaluating the quality of the business, that would be 999 wasted days of effort. It makes more sense for the lenders to appoint a single person to evaluate the business on behalf of all of them. That’s exactly what a bank does. Banks coordinate lenders and minimize information costs. Banks are thus an important example of the benefits of specialization and the division of labor.

Banks also spread risk. If Fred Smith, or some other borrower, defaults on his loan, banks spread that loss across the many lenders who deposit money in the bank. This avoids the risk that you have lent Fred Smith $1,000 and suddenly are out the entire sum. It’s less risky and no less profitable to lend one thousand firms $1 each than to lend one firm $1,000, so the spreading of risk encourages greater lending and investment.

Banks also play a role in the payments system. Money deposited in a bank can be drawn on with a check or debit card or via the ATM. We discuss banks and the payment system at greater length in Chapter 15.

Overall, banks make our lives simpler. We open our accounts, deposit our money, receive our interest payments, and write our checks; at the same time we are participating in the process of economic growth because the bank oversees a process by which our savings are turned into productive investments.

The Bond Market

Instead of borrowing from a bank, well-known corporations can borrow directly from the public. Your local pizza restaurant borrows from a bank, or perhaps even from relatives, because restaurants are a risky business and the finances of that company are difficult for outside investors to evaluate. But when it comes to IBM or Toyota, investors can more easily find information about the firm and so they are willing to bypass the bank as an intermediary and lend to the company directly.

A bond is a sophisticated IOU that documents who owes how much and when payment must be made.

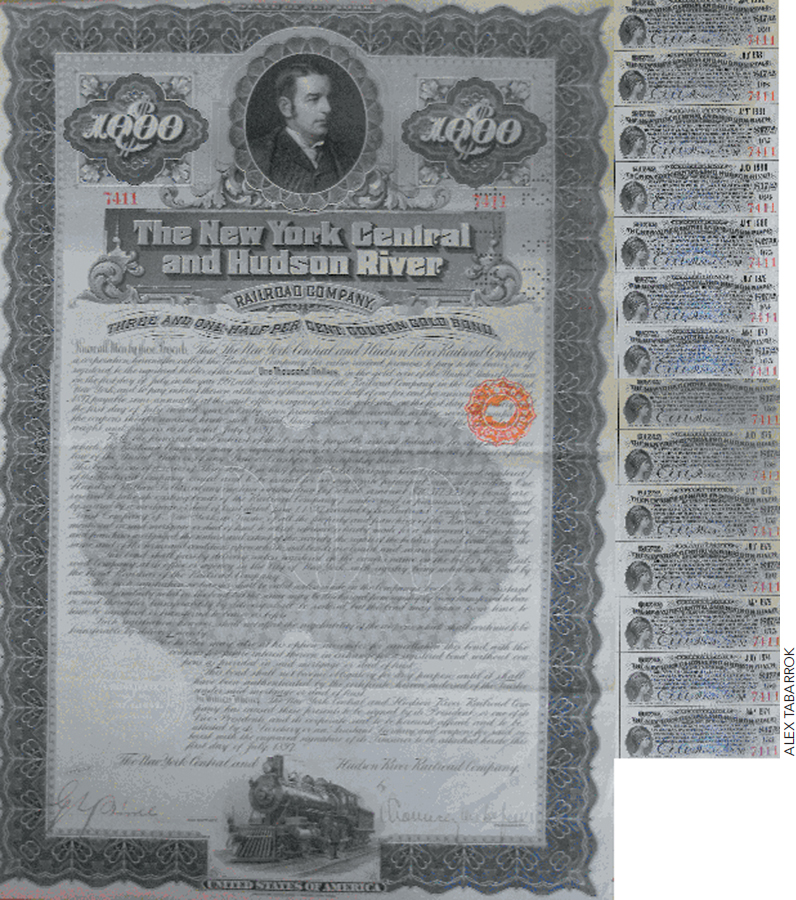

When a member of the public lends money to a corporation, the corporation acknowledges its debt by issuing a bond. A bond is a corporate IOU. The bond contract lists how much is owed to the bond’s owner and when payment must be made. In some cases, all the money is owed on a single day (the day of maturity); in other cases, periodic payments, called coupon payments, must be made in addition to a final payment.

The New York Central and Hudson River Railroad Company borrowed money in 1897 for which they issued bonds, one of which is pictured on the right. The bond is an IOU that promises the Central will pay the owner $1,000 in 1997. In addition, every six months until 1997, the Central promised to pay the owner $17.50. You can see from the picture why the periodic payments are called “coupon payments”: The coupons are on the right of the bond and can be clipped and sent to the issuer of the bond to receive payment.

Central’s bond illustrates one of the advantages of bond finance—large sums of money can be raised now and invested in long-lived assets such as railroad track. The money can then be paid back over a long period of time, in the case of the Central over a 100-year period.

All bonds involve a risk that when the payments come due, the borrower will not be able to pay; this is called “default risk.” The Central, for example, eventually defaulted when it went bankrupt, but it did pay its coupons until 1970. Major bond issues are graded by agencies like Moody’s and Standard and Poor’s. AAA, for example, is the highest grade issued by Standard and Poor’s; this grade indicates, according to the rating agencies, that the bond is very likely to be paid. Grades range all the way from AAA to D when a firm is in default. Bonds rated less than BBB- are sometimes called “junk bonds.” It’s important to remember that risk can never be perfectly quantified and the rating agencies can be wrong—a point we will return to later in this chapter when we discuss the 2007–2008 financial crisis.

If a risky company wishes to borrow money, it has to promise a higher rate of interest because lenders will demand to be compensated for a greater risk of default. Why lend to a risky firm unless you have some prospect of earning higher returns?

Thus, the marketplace grades the risks of major investments and charges interest rates accordingly. As of 2014, Berkshire Hathaway, the investment company managed by Warren Buffett, was still a very profitable company. In early 2014, it was borrowing two-year money at less than 1%, an extraordinary reflection of its perceived financial soundness. Elsewhere, in the United Kingdom, the soccer team Manchester United was borrowing money at about 9% for a seven-year bond; apparently their players and managers aren’t as good!

Collateral is something of value that by agreement becomes the property of the lender if the borrower defaults.

Can you think of one reason why interest rates on home loans are almost always lower than interest rates on vacation loans? The bank can repossess the house but not the vacation! The house is a form of collateral, something of value that by agreement becomes the property of the lender if the borrower defaults on the loan. Thus, the market for loanable funds is really a broad spectrum of markets; the interest rates differ depending on the borrower, repayment time, amount of the loan, type of collateral, and many other features of the loan.

Greater risk can reduce the supply of funds to the market as a whole. If lenders expect a recession, for example, they may become concerned that many firms will go bankrupt and default on their debt. A lender who was willing to lend at 8% when he or she thought the risk was low will demand a higher return if the lender believes the risk of default has increased significantly.

Crowding out is the decrease in private consumption and investment that occurs when government borrows more.

Governments borrow money as well. As of 2014, the U.S. government owed about $12.6 trillion dollars to private borrowers (individuals, firms, and governments other than the U.S. federal government). When the government borrows a lot of money, private consumption and investment can be crowded out. Imagine, for example, that the government borrows $100 billion to cover a budget deficit. In Figure 9.10, the demand curve for loanable funds shifts to the right by $100 billion, increasing the interest rate from 7% to 9%. The higher interest rate has two effects. First, it draws an additional $50 billion of savings into the market so total savings increase from $200 billion to $250 billion. Since greater savings mean less consumption, we can also say that consumption is reduced by $50 billion. Second, the higher interest rate means that some investments and other projects are no longer profitable so at a higher interest rate, private borrowing falls. In Figure 9.10, we show private borrowing falling by $50 billion. Thus, the $100 billion necessary to cover the government’s budget deficit comes from a combination of reduced consumption and reduced private investment and other private borrowing.

FIGURE 9.10

We will return to the issues of crowding out, government debt, and deficits in Chapter 17 and Chapter 18.

When the U.S. government borrows, it issues a variety of different bonds. U.S. Treasury bonds or T-bonds are 30-year bonds that pay interest every 6 months. T-notes are bonds with maturities ranging from 2 to 10 years that also pay interest every 6 months. T-bills are bonds with maturities of a few days to 26 weeks that pay only at maturity. A bond that pays only at maturity is also called a zero-coupon bond or a discount bond since these bonds sell at a discount to their face value.

Treasury securities are desirable for many investors because they are easy to buy and sell and the U.S. government is unlikely to default on its payments. In general, short-term U.S. government securities tend to be the safest assets, and very short-term bonds, called commercial paper, issued by very large corporations tend to be safe as well. In addition, Treasury securities, especially T-bills, are important in monetary policy; the Federal Reserve buys and sells Treasury securities on a daily basis to influence the money supply (more on this in Chapter 16).

Bond Prices and Interest Rates It’s often convenient to express the price of a bond in terms of an interest rate; this is easiest to do with a zero-coupon bond. Suppose, for example, that a bond with very little risk exists that will pay $1,000 in one year’s time and that this bond is currently selling for $950. If you were to buy this bond today and hold it until maturity, you would earn $50 ($1,000 – $950), or a rate of return of  . Thus, every zero-coupon bond has an implied rate of return that can be calculated by subtracting the price from the value at maturity, often called the face value, and then dividing by the price:

. Thus, every zero-coupon bond has an implied rate of return that can be calculated by subtracting the price from the value at maturity, often called the face value, and then dividing by the price:

Sellers of bonds must compete to attract lenders, who compare the implied rate of return on bonds with the rate of return on other assets. Imagine, for example, that the interest rate on say a savings account at a bank increases to 10%. Would you buy a bond that pays 5.26%? Would anyone? Of course not. So if the interest rate rises to 10%, what must happen to the price of this bond? The price must fall. In fact, if the interest rate rises to 10%, the price of the bond must fall to $909. Why? Because at a price of $909, the rate of return on the bond is  . Thus, at a price of $909, sellers of bonds will be able to compete with banks, who are paying 10% on savings accounts, but at a higher price they won’t find any buyers.

. Thus, at a price of $909, sellers of bonds will be able to compete with banks, who are paying 10% on savings accounts, but at a higher price they won’t find any buyers.

Arbitrage, the buying and selling of equally risky assets, ensures that equally risky assets earn equal returns.

Our simple bond pricing example tells us two things of importance. First, equally risky assets must have the same rate of return. If they didn’t, no one would buy the asset with the lower rate of return and the price of that asset would fall until the rate of return was competitive with other investments. This is called an arbitrage principle and we discuss it at greater length in the appendix to this chapter.

The second important lesson is that interest rates and bond prices move in opposite directions. When interest rates go up, bond prices fall. When interest rates go down, bond prices rise. We will be referring to this principle several times throughout the textbook so do study the principle and make a note of it:

Interest rates and bond prices move in opposite directions.

Interest rates and bond prices move in opposite directions.

The inverse relationship between bond prices and interest rates tells us that in addition to default risk, people who buy bonds also face interest rate risk. For instance, perhaps a bond was issued in 2003 at an interest rate of 7%. If interest rates for comparable investments later rise to 9%, having bought a bond yielding 7% was in retrospect a mistake. If, instead, comparable interest rates were to fall to 3%, the bond purchase worked out for the better. The buyer locked in a 7% return when other rates of return were falling to 3%. In other words, bond buyers are making bets that interest rates will fall (bond prices will rise), or at least they are hoping that interest rates will fall. And similarly, bond sellers are betting or hoping that interest rates will rise, which means bond prices will—do you remember?—fall. Again, for more on the relationship between bond prices and interest rates, see the chapter appendix.

The Stock Market

A stock or a share is a certificate of ownership in a corporation.

Just as businesses fund their activities by taking out bank loans and selling bonds, they also issue shares of stock. Stocks are shares of ownership in a corporation. Owners have a claim to the firm’s profits, but remember that profit is revenue minus costs. In other words, profit is what is left over after everyone else—creditors, bond holders, suppliers, and employees—have been paid. If profits are high, shareholders benefit. They benefit directly if the firm pays out its profits in dividends or indirectly if the firm reinvests its profits in a way that increases the value of the stock. But if profits are low or negative, shareholders suffer losses.

An initial public offering (IPO) is the first time a corporation sells stock to the public in order to raise capital.

Stocks are traded on organized markets called stock exchanges. The New York Stock Exchange (NYSE) is the largest in the world. When new stocks are issued, that is called an initial public offering or an IPO. An IPO is the first time a stock is sold to the public.

You’ll recall from the beginning of this chapter that simply buying and selling existing shares of stock does not increase net investment in the economy. But when a firm sells new shares to the public, it typically uses the proceeds to fund investment, that is, to buy new capital goods. In addition, the possibility of offering equity or ownership in a firm opens the door to many business ventures that might never get off the ground, or might not be able to expand rapidly.

Consider Google. Google is today a household word, but when the company began in September 1998, it was headquartered in a garage. Yet in August 2004, Google founders Sergei Brin and Larry Page sold $1.67 billion worth of stock in an IPO. The money helped Google to fund new investments and pay for research and development. In addition, Google’s IPO turned the founders and the early investors into millionaires and billionaires. This big payoff was a reward for creating the company and making the early and risky investments that were necessary to get Google off the ground. Stock markets help people with great ideas become rich and that encourages innovation. It is no accident that the United States—one of the most innovative countries in the world—also has the best developed stock and capital markets.

CHECK YOURSELF

Question 9.8

![]() What is the primary role of financial intermediaries?

What is the primary role of financial intermediaries?

Question 9.9

![]() If your $1,000 corporate bond pays you $60 in interest every year and the interest rate falls to 4%, does the price of the bond rise or fall? What happens if the interest rate rises to 8%?

If your $1,000 corporate bond pays you $60 in interest every year and the interest rate falls to 4%, does the price of the bond rise or fall? What happens if the interest rate rises to 8%?

Question 9.10

![]() Why does an IPO increase net investment in the economy but your purchase of 200 shares of IBM stock does not increase investment?

Why does an IPO increase net investment in the economy but your purchase of 200 shares of IBM stock does not increase investment?

Selling part of Google to the public also let the founders diversify. If someday another search service bests Google, Brin and Page will not become paupers. This added safety also encourages innovation. People who come up with new ideas know that their wealth will not be locked into one firm.

We’ll have a lot more to say about stock markets in the stock markets chapter, but for now what you need to know is that stock markets encourage investment and growth.