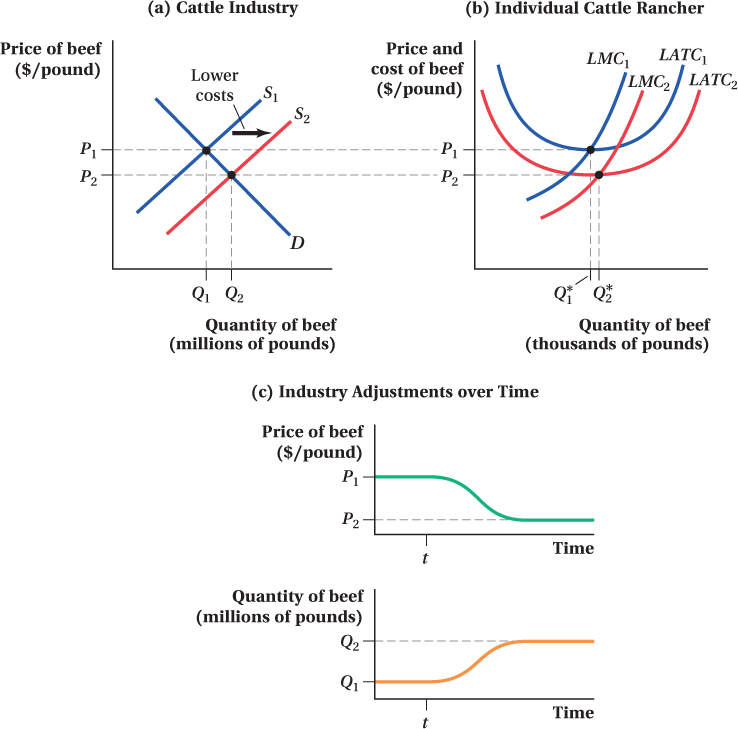

Figure 8.18 Long- Run Adjustments to a Reduction in Costs in a Perfectly Competitive Industry

(a) A decrease in industrywide marginal costs leads to an increase in the supply of beef from S1 to S2. Industry quantity increases from Q1 to Q2, and the market price decreases from P1 to P2 in the long run.(b) The decrease in industrywide marginal costs shifts the individual cattle rancher’s lon to

to  .(c) An increase in the supply of beef leads to a lon

.(c) An increase in the supply of beef leads to a lon