| Figure 29.8 | The Lon |

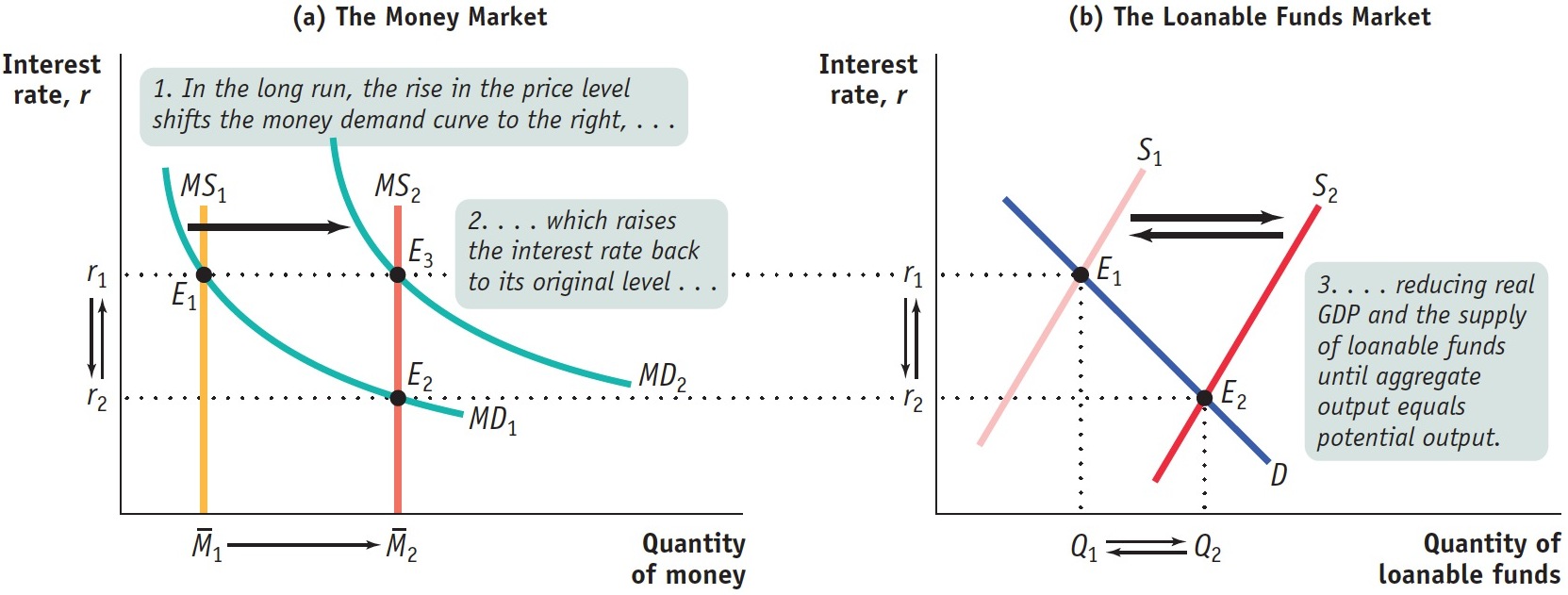

The Long- Run Determination of the Interest Rate Panel (a) shows the liquidity preference model long- run adjustment to an increase in the money supply from  1 to 2; panel (b) shows the corresponding lon

1 to 2; panel (b) shows the corresponding long- run adjustment in the loanable funds market. As we discussed in FIGURE 29.7, the increase in the money supply reduces the interest rate from r1 to r2, increases real GDP, and increases savings in the short run. This is shown in panel (a) and panel (b) as the movement from E1 to E2. In the long run, however, the increase in the money supply raises wages and other nominal prices; this shifts the money demand curve in panel (a) from MD1 to MD2, leading to an increase in the interest rate from r1 to r2 as the economy moves from E2 to E3. The rise in the interest rate causes a fall in real GDP and a fall in savings, shifting the loanable funds supply curve back to S1 from S2 and moving the loanable funds market from E2 back to E1. In the long run, the equilibrium interest rate is the rate that matches the supply and demand for loanable funds when real GDP equals potential output.

1 to 2; panel (b) shows the corresponding lon[Leave] [Close]