| Figure 60.4 | The Effect of an Increase in Demand in the Short Run and the Long Run in an Increasin |

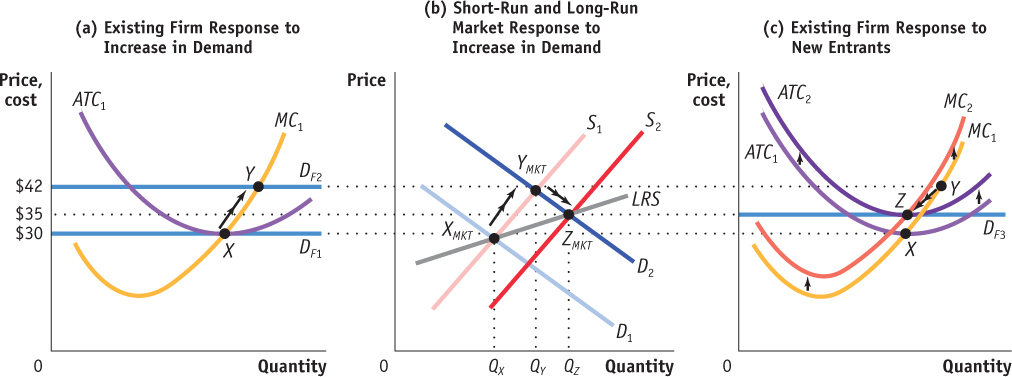

The Effect of an Increase in Demand in the Short Run and the Long Run in an Increasing- Cost Industry In an increasing- cost industry, an increase in demand leads to a higher price both in the short run and in the long run. Suppose demand increases from D1 to D2 as shown in panel (b). This raises the market price to $42. Existing firms increase their output, and industry output expands along the short- run industry supply curve, S1, to a short- run equilibrium at YMKT. The increase in output from QX to QY is the result of existing firms increasing their output as shown for a representative firm by the move from point X to point Y in panel (a). Because the new price is above the minimum of average total cost, economic profit attracts new entrants in the long run, shifting the short- run industry supply curve rightward and lowering the market price. Meanwhile, industry expansion drives up the cost of inputs and shifts the firms’ cost curves upward as shown in panel (c). This continues until the falling equilibrium price meets the rising minimum of average total cost. As shown in panel (b), that occurs at equilibrium point ZMKT with a price of $35 and an industry output of QZ. Assuming that the higher input prices raise the cost of making each unit by the same amount, the firms’ cost curves shift straight up. In the long run, an existing firm moves from Y to Z in panel (c), returning to its initial output level and earning zero economic profit. The upward- sloping line passing through XMKT and ZMKT, labeled LRS, is the long- run industry supply curve.

[Leave] [Close]