Chapter Introduction

CHAPTER 3

THE COFFEE MARKET’S HOT; WHY ARE BEAN PRICES NOT?

Insights into Supply and Demand

Under fifteenth-

SUPPLY, DEMAND, AND THE GREAT EXPLORERS

The story of supply and demand began long ago. Let’s pick it up with the great explorers of the fifteenth and sixteenth centuries. In 1492, Christopher Columbus sailed the ocean blue in search of a westward route to Asia and its gold. In 1519, Ferdinand Magellan proved that the earth is round on an expedition to the Spice Islands, where cinnamon, nutmeg, and cloves were abundant. The royalty of Spain paid generously for these trips because gold was precious and, at that time in Europe, some spices were worth more than their weight in gold. Why were these products so expensive? This chapter explains how the combination of high demand and limited supply leads to high prices. Thanks to the incentives that high prices provide, new trade routes were established, supply increased, and spices became affordable. In other words, Europeans came to America and you can have cinnamon in your latte thanks to the workings of supply and demand.

Because they explain so much, let’s explore the concepts of supply and demand. We’ll refer to them and their famous graph again in later chapters.

Supply

The supply curve exhibits the relationship between price and quantity supplied. According to the “law” of supply,1 as price increases, the quantity suppliers would be willing to supply increases, and as price decreases, the willingly supplied quantity decreases. This suggests, for example, that the Reno Philharmonic Orchestra2 would be willing to put on more performances per week if it could command an $80 ticket price than if it could command a $60 ticket price. This positive relationship between price and quantity is illustrated by the upward slope of the supply curve in the accompanying diagram.

1 Like other laws, the relationships that economists refer to as laws are sometimes broken.

2 See www.renophilharmonic.com/

It is likely that the law of supply describes your own behavior as well. Think about how many hours of burger flipping, lawn mowing, or babysitting you would supply per week at various prices. If you would supply more hours for $50 per hour than for $5 per hour, your supply curve resembles the one in the diagram. Let’s examine why you probably would, using the economic concept of opportunity cost.

The opportunity cost of a particular action is the value of the next-

It’s not only babysitting services that exhibit increasing opportunity costs. Consider items produced for sale, which economists refer to as goods, made with productive resources—

3 See www.millionsolarroofs.org/

4 For example, www.kysolar.org describes new solar installation training programs to handle the “shortage of trained, active installers.”

Increasing marginal costs cause suppliers to require higher prices in exchange for greater quantities. Thus, the supply curve, which shows the relationship between price and quantity supplied, is generally upward sloping. Marginal costs rise with production levels in many contexts and for many reasons. For example, it becomes increasingly expensive to obtain larger quantities of natural resources, such as fossil fuels and fish, as suppliers must tap more distant and less productive areas of the land and sea. And according to the “law” of diminishing marginal returns, if you add more and more of an input that is easily varied, for example fishers, to an input that is relatively fixed in quantity or size, such as a boat, the additional number of fish caught by each new fisher will eventually fall. Congestion decreases the contributions of new fishers, as do decreasing opportunities for specialization. A single fisher in a boat would have to navigate, tend the nets, and manage the catch. She or he might not become particularly good at any of these varied tasks. With three fishers, each could specialize in 1 of the 3 tasks and become particularly skilled and effective in that area. As more fishers are added, there are no new opportunities for specialization, redundancy sets in, and it becomes more costly to increase production levels. The classic example of diminishing marginal returns is about adding seeds to a flowerpot: If you keep adding seeds to a fixed amount of soil, the additional returns in terms of flowers will eventually decrease, and, at some point, there will be so many seeds in the pot that another seed will find no soil.

The market supply curve is simply the sum of individual firms’ supply curves, which is determined by adding up the quantities supplied by all the suppliers at each price. Suppose the fish market consists of 2 suppliers, Fred’s Fish and Fay’s Fish. If Fay would supply 10 fish for $1 each and 15 fish for $2 each, whereas Fred would supply 6 fish for $1 each and 12 fish for $2 each, then the market supply is 16 fish at $1 (10 from Fay plus 6 from Fred) and 27 fish at $2 (15 from Fay plus 12 from Fred). This information is summarized in the following table. The supply at any other price can be determined in the same way—

| PRICE | FAY’S SUPPLY | FRED’S SUPPLY | MARKET SUPPLY |

| $1 | 10 | 6 | 16 |

| $2 | 15 | 12 | 27 |

Because the supply curve reflects the marginal cost of production, the entire curve will shift downward and to the right, as from the solid supply curve to the dotted supply curve in the figure, when the cost of producing each additional unit decreases. For example, it would become cheaper to catch fish if there were an improvement in fishing technology, better weather, a reduction in fishing taxes, an increase in restocking subsidies, or higher catch limits. As the sum of all the fisher supply curves, the market supply curve will also shift downward and to the right when new fishers enter. The opposite of any of these changes will shift the supply curve upward and to the left, as from the dotted supply curve to the solid curve.

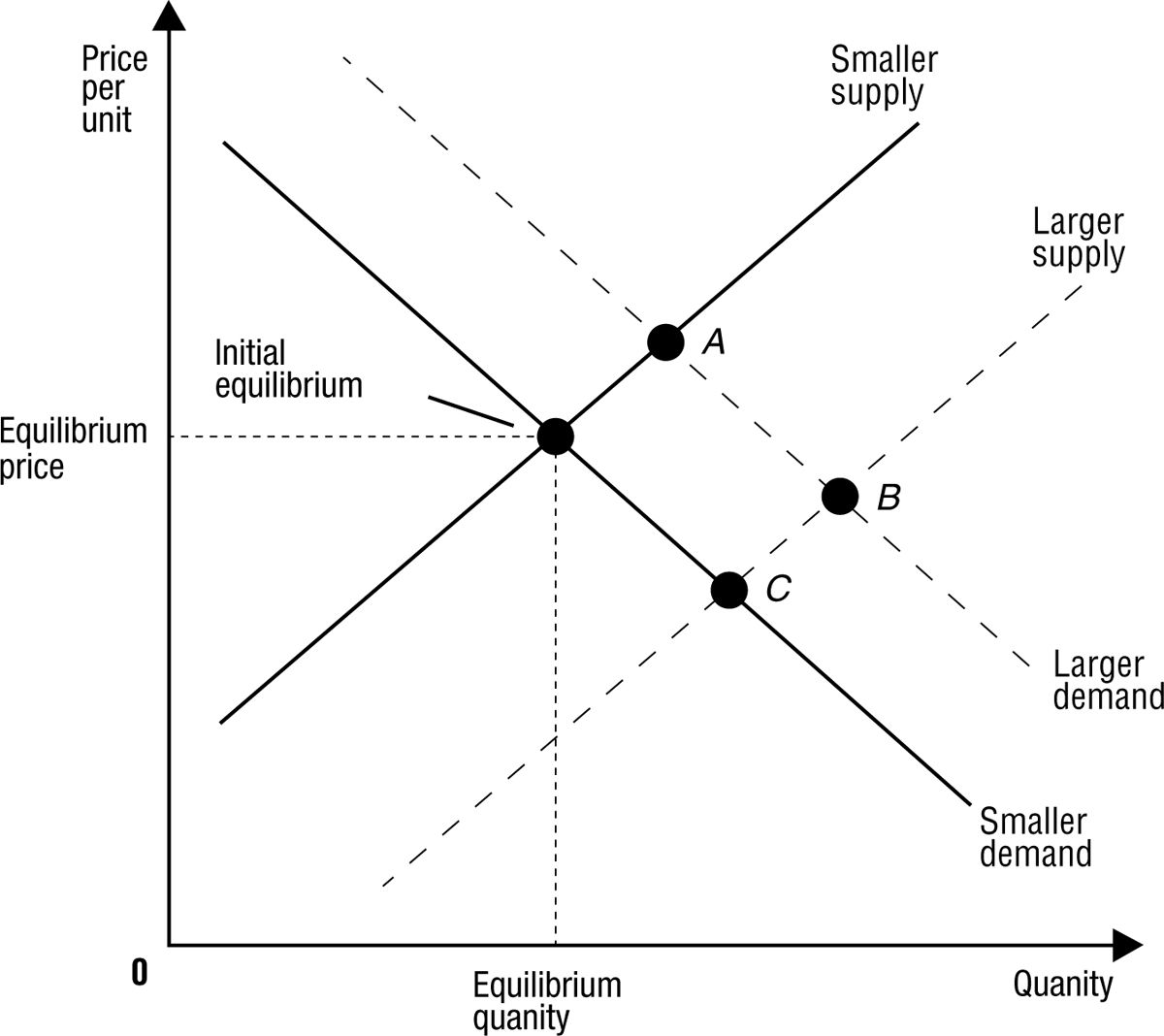

Note that a change in the price of fish does not change the marginal cost of catching fish and will, therefore, not shift the supply curve. Rather, it will cause a movement to a new point along the existing supply curve, as from the point labeled “Initial equilibrium” to point A in the figure. To distinguish between these two types of changes, we call a movement along a stationary supply curve a change in the quantity supplied and a shift in the supply curve itself, as from the solid supply curve to the dotted supply curve, a change in supply.

Demand

The demand curve shows the relationship between the price of a good or service and the quantity demanded. The demand for a good or service depends on the benefits it conveys. Whether it is fish, clothing, coffee, or almost anything else, the marginal benefit—the benefit gained from 1 more—

5 This concept, called diminishing marginal utility, is explained in greater detail in Chapter 4.

Consider your demand for cans of tuna fish. Your 1st can in a week provides the important benefits of protein, minerals, omega-

6 Of course, you are unlikely to need to pay $5 for a can of tuna, but the demand curve describes the most you would pay if you had to, not what you must or do pay.

| PRICE | YOUR DEMAND | MY DEMAND | MARKET DEMAND |

| $6 | 0 | 0 | 0 |

| $5 | 1 | 0 | 1 |

| $4 | 1 | 0 | 1 |

| $3 | 1 | 1 | 2 |

| $2 | 1 | 1 | 2 |

| $1 | 2 | 2 | 4 |

| $0.30 | 3 | 2 | 5 |

| $0 | 3 | 2 | 5 |

As explained in Chapter 1, economists assume that people behave rationally. It is rational for you to buy cans of tuna fish until the benefit you receive from 1 more can is no longer worth at least as much as the price you must pay for it. If the price were $6, you wouldn’t buy any tuna fish because even the first can is only worth $5 to you. If the price were $4, you would buy 1 can because it’s rational to pay $4 for something that’s worth $5. At a price of $1 or less, you would buy the second can, which is worth $1 to you, and if the price were 30 cents or less, you would buy 3 cans but no more.

The market demand curve is found by adding up the quantities demanded by all individuals in the market at each price. Suppose I would be willing to pay up to $3 for my first can of tuna fish, $1 for a second, and nothing for a third, and that you and I are the only consumers in the tuna fish market. The table on page 21 illustrates the demand schedules for you, me, and the market. The quantity demanded in the market would be 1 can at a price of $5 because at that price you would demand your first can. At $3 the market demand would increase to a quantity of 2 because I would buy my first can at that price. The quantity demanded would increase to 4 at a price of $1 because each of us would buy our second can if the price fell to $1. At a price of 30 cents the market demand would increase to 5. After that point, neither of us would purchase another can of tuna fish at any price. Thus, the market demand curve falls to a height of 0 after the quantity of 5.

Because the demand curve reflects consumers’ willingness to pay for each additional unit of a good or service, the curve will shift upward and to the right, as from the solid demand curve to the dotted demand curve in the figure, when the willingness to pay increases. This could result from

a change in income

a successful advertising campaign

expectations of an upcoming increase in prices

an increase in the price of substitutes, such as peanut butter and jelly

a decrease in the price of complementary goods, such as bread

an increase in the number of tuna fish consumers

The opposite of these changes would cause the demand curve to shift downward and to the left. The effect of a change in income depends on the type of good in question. A normal good is one that consumers buy more of when their incomes increase, and an inferior good is one that consumers buy less of when incomes increase. Whether a good is normal or inferior depends on individual preferences. For some people, tuna fish might be a normal good. Other people might buy more steak and less tuna fish when their incomes increase, so for them steak would be normal and tuna fish would be inferior. Other examples of goods that are inferior for some people include secondhand clothing, rides on public buses, store-

The Marriage of Supply and Demand

Referring to the figure, note that the supply and demand curves reside on the same graph, with the price per unit measured on the vertical axis and the quantity of a particular good measured on the horizontal axis. Supply and demand meet at the equilibrium point, which is so named because it represents a balance between the quantity demanded and the quantity supplied. The price directly to the left of the equilibrium point is the equilibrium price, and the quantity directly below the equilibrium point is the equilibrium quantity. If the price is initially set above the equilibrium price, the quantity supplied will exceed the quantity demanded, and the resulting surplus will lead suppliers to lower their price. If the price begins below the equilibrium price, the quantity demanded will exceed the quantity supplied, and the resulting shortage will motivate an increase in the price. Thus, we expect the price to reach the equilibrium level and stay there until there is a shift in either the supply curve or the demand curve. With knowledge of a shift in one of the curves, we can learn how price and quantity are affected by drawing the shift and comparing the new and old equilibrium points.

Now we are equipped to explain the happenings in the spice and coffee markets of the past and present. In the sixteenth century, the supply of cinnamon in Europe was very small. Because quantities are measured on the horizontal axis and the smallest quantities are farthest to the left, we represent a relatively small supply with the solid “smaller supply” curve on the left side of the graph. Suppose demand is represented by the solid “smaller demand” curve. To discover the influence of supply fluctuations on price, we compare the price level (height) at the initial equilibrium of the solid supply and demand curves and at equilibrium point C at the intersection of the dotted “larger supply” curve and the solid demand curve. With limited supply, the price is higher, which helps to explain the high equilibrium price fetched by cinnamon and other spices imported by Europeans 500 years ago. The supply of spices to Europe and America increased dramatically after Columbus, Magellan, and other explorers established faster and safer trade routes to Asia. As more and more ships brought spices to Western shores, the supply curve shifted from left to right and the equilibrium price fell.

THE COFFEE CRISIS

In the spice example, we left the demand curve unchanged, but to examine recent activity in the coffee market, we must consider the effect on prices of changes in demand. Starting again at the equilibrium of the solid demand and supply curves in the figure, an increase in the popularity of coffee shifts the demand curve to the right. This demand shift indicates that people are willing to buy more coffee at any given price. What happens to the equilibrium price as a result of this increase in demand? It rises to the level of equilibrium point A, and higher prices entice an increase in the quantity of coffee supplied. Note that the change in demand has not affected the cost of producing coffee, which depends on input costs rather than demand, so the supply curve does not shift. Point A is on the same supply curve that we started with, but the price has risen because the demand curve shifted outward.

Today, U.S. consumers demand roughly $1.3 trillion worth of imported goods annually. The United States is the largest importer of coffee, which, after oil, is the most traded commodity in the world. More than 400 billion cups of coffee are consumed worldwide each year. But as increasing demand led Starbucks, Inc., to open 5,700 new retail outlets during the past 5 years, the price of coffee beans declined by half. Let’s examine the paradox of coffee prices in the context of supply and demand.

In the 1980s, coffee sold for about $1.20 per pound on the world market. This price provided healthy profits for coffee growers and led to a rapid expansion in the allocation of land to coffee farming in countries such as Vietnam and Brazil. The fruits of these plantings became available in the 1990s. Although coffee demand was robust during that period, supply increased by even more than demand. The dotted curves in the figure represent the larger demand and the much larger supply of coffee experienced in the 1990s. An increase in demand lifts prices, but an increase in supply lowers them, and the downward effect on prices was dominant. Despite the large demand, prices were depressed by the overarching supply glut.

In the early 2000s, coffee prices languished at about 50 cents a pound, a 100-

CONCLUSION

Supply is determined by the marginal cost of production, which generally increases with quantity. Demand is determined by marginal benefit, which tends to fall as quantity increases. The price-

8 The Strategic Petroleum Reserve is a collection of more than 700 million barrels of oil for use primarily in emergencies. After Hurricane Katrina knocked out many oil-

DISCUSSION STARTERS

In Chapter 2, I explained that in 2005 Toyota doubled the supply of Priuses, and yet people were paying higher prices than ever for those cars. Using a supply-

and- demand graph, explain how an increase in price can accompany an increase in supply. As your income increases, what do you think will happen to your demand curve for Folgers coffee? What will happen to your demand curve for Starbucks coffee? Are these goods, therefore, normal or inferior?

How do you think Magellan’s discoveries affected the market demand curve for spices? What do you think is the main reason for any change in the market demand curve for cinnamon during the past 500 years?

An organization called TransFair certifies a “fair trade” designation for coffee beans purchased at a wholesale price of $1.26 or more per pound. What do you think would happen to the quantity of coffee beans supplied and demanded if the government mandated a minimum wholesale price of $1.26 for all coffee bean purchases?