An Overview of the Twenty-first Century American Banking System

Under normal circumstances, banking is a rather staid and unexciting business. Fortunately, bankers and their customers like it that way. However, there have been repeated episodes in which “sheer panic” would be the best description of banking conditions—

The creation of the Federal Reserve System in 1913 was largely a response to lessons learned in the Panic of 1907. In 2008, the United States found itself in the midst of a financial crisis that in many ways mirrored the Panic of 1907, which occurred almost exactly 100 years earlier.

Crisis in American Banking at the Turn of the Twentieth Century

The creation of the Federal Reserve System in 1913 marked the beginning of the modern era of American banking. From 1864 until 1913, American banking was dominated by a federally regulated system of national banks. They alone were allowed to issue currency, and the currency notes they issued were printed by the federal government with uniform size and design. How much currency a national bank could issue depended on its capital. Although this system was an improvement on the earlier period in which banks issued their own notes with no uniformity and virtually no regulation, the national banking regime still suffered numerous bank failures and major financial crises—

The main problem afflicting the system was that the money supply was not sufficiently responsive: it was difficult to shift currency around the country to respond quickly to local economic changes. In particular, there was often a tug-

However, the cause of the Panic of 1907 was different from those of previous crises; in fact, its cause was eerily similar to the roots of the 2008 crisis. Ground zero of the 1907 panic was New York City, but the consequences devastated the entire country, leading to a deep four-

Being less regulated than national banks, trusts were able to pay their depositors higher returns. Yet trusts took a free ride on national banks’ reputation for soundness, with depositors considering them equally safe. As a result, trusts grew rapidly: by 1907, the total assets of trusts in New York City were as large as those of national banks. Meanwhile, the trusts declined to join the New York Clearinghouse, a consortium of New York City national banks that guaranteed one another’s soundness; that would have required the trusts to hold higher cash reserves, reducing their profits.

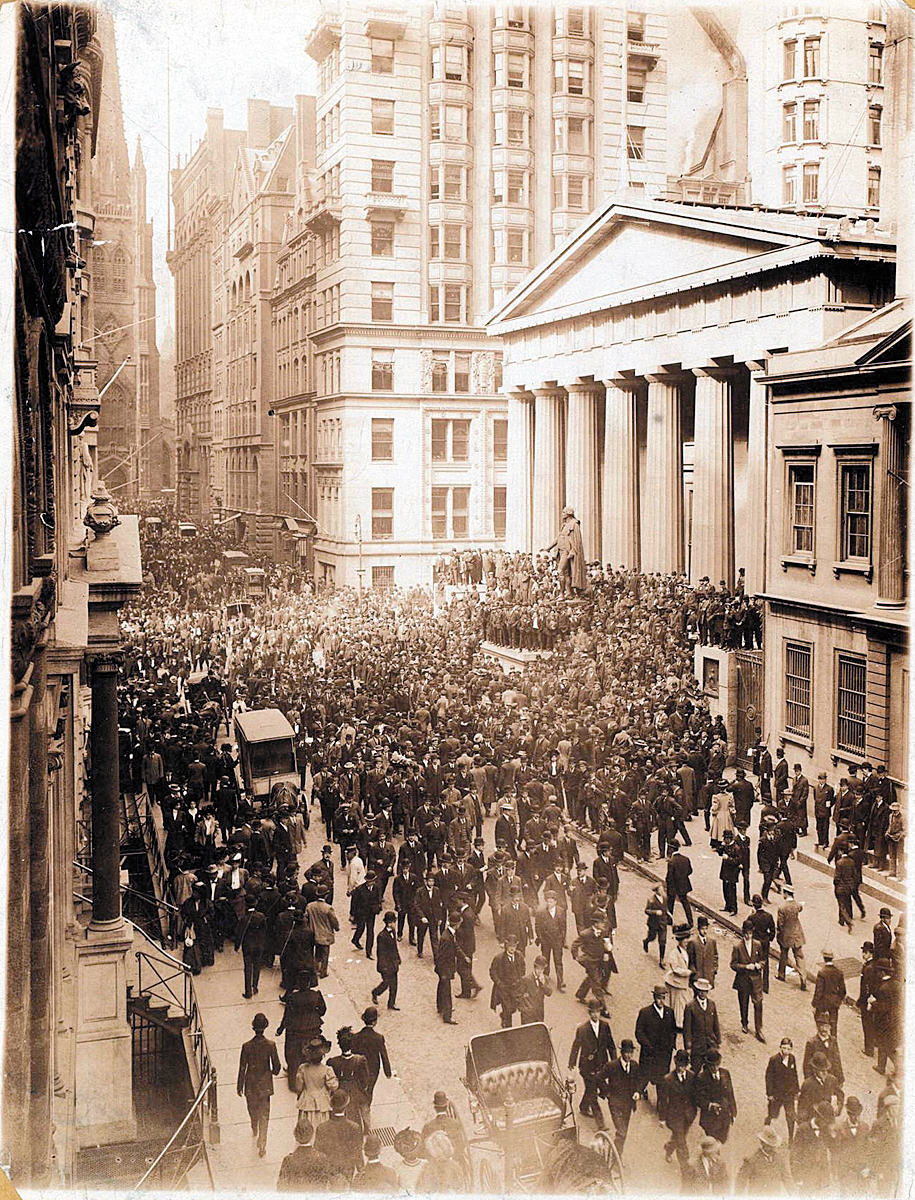

The Panic of 1907 began with the failure of the Knickerbocker Trust, a large New York City trust that failed when it suffered massive losses in unsuccessful stock market speculation. Quickly, other New York trusts came under pressure, and frightened depositors began queuing in long lines to withdraw their funds. The New York Clearinghouse declined to step in and lend to the trusts, and even healthy trusts came under serious assault. Within two days, a dozen major trusts had gone under. Credit markets froze, and the stock market fell dramatically as stock traders were unable to get credit to finance their trades and business confidence evaporated.

Fortunately, one of New York City’s wealthiest men, the banker J. P. Morgan, quickly stepped in to stop the panic. Understanding that the crisis was spreading and would soon engulf healthy institutions, trusts and banks alike, he worked with other bankers, wealthy men such as John D. Rockefeller, and the U.S. Secretary of the Treasury to shore up the reserves of banks and trusts so they could withstand the onslaught of withdrawals. Once people were assured that they could withdraw their money, the panic ceased. Although the panic itself lasted little more than a week, it and the stock market collapse decimated the economy. A four-

Responding to Banking Crises:The Creation of the Federal Reserve

Concerns over the frequency of banking crises and the unprecedented role of J. P. Morgan in saving the financial system prompted the federal government to initiate banking reform. In 1913 the national banking system was eliminated and the Federal Reserve System was created as a way to compel all deposit-

The Structure of the Fed

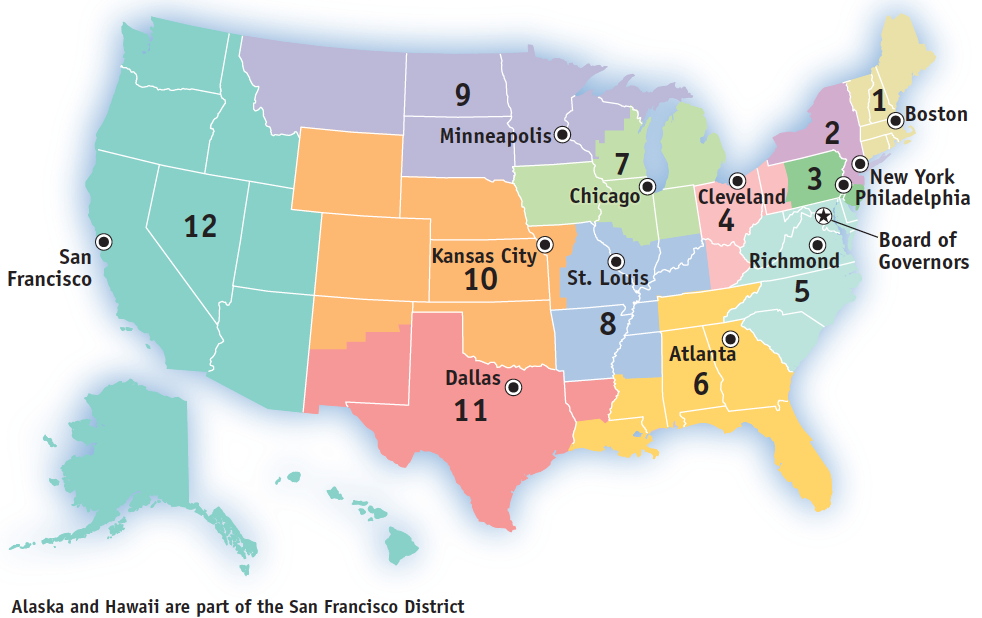

The legal status of the Fed is unusual: it is not exactly part of the U.S. government, but it is not really a private institution either. Strictly speaking, the Federal Reserve System consists of two parts: the Board of Governors and the 12 regional Federal Reserve Banks.

The Board of Governors, which oversees the entire system from its offices in Washington, D.C., is constituted like a government agency: its seven members are appointed by the president and must be approved by the Senate. However, they are appointed for 14-

The 12 Federal Reserve Banks each serve a region of the country, known as a Federal Reserve district, providing various banking and supervisory services. One of their jobs, for example, is to audit the books of private-

| Figure 26.1 | The Federal Reserve System |

Decisions about monetary policy are made by the Federal Open Market Committee, which consists of the Board of Governors plus five of the regional bank presidents. The president of the Federal Reserve Bank of New York is always on the committee, and the other four seats rotate among the 11 other regional bank presidents. The chair of the Board of Governors normally also serves as the chair of the Federal Open Market Committee.

The effect of this complex structure is to create an institution that is ultimately accountable to the voting public because the Board of Governors is chosen by the president and confirmed by the Senate, all of whom are themselves elected officials. But the long terms served by board members, as well as the indirectness of their appointment process, largely insulate them from short-

The Effectiveness of the Federal Reserve System

Although the Federal Reserve System standardized and centralized the holding of bank reserves, it did not eliminate the potential for bank runs because banks’ reserves were still less than the total value of their deposits. The potential for more bank runs became a reality during the Great Depression. Plunging commodity prices hit American farmers particularly hard, precipitating a series of bank runs in 1930, 1931, and 1933, each of which started at midwestern banks and then spread throughout the country. After the failure of a particularly large bank in 1930, federal officials realized that the economy-

In the midst of the catastrophic bank run of 1933, the new U.S. president, Franklin Delano Roosevelt, was inaugurated. He immediately declared a “bank holiday,” closing all banks until regulators could get a handle on the problem. In March 1933, emergency measures were adopted that gave the RFC extraordinary powers to stabilize and restructure the banking industry by providing capital to banks either by loans or by outright purchases of bank shares. With the new regulations, regulators closed nonviable banks and recapitalized viable ones by allowing the RFC to buy preferred shares in banks (shares that gave the U.S. government more rights than regular shareholders) and by greatly expanding banks’ ability to borrow from the Federal Reserve. By 1933, the RFC had invested over $17 billion (2013 dollars) in bank capital—

A commercial bank accepts deposits and is covered by deposit insurance.

An investment bank trades in financial assets and is not covered by deposit insurance.

Although the powerful actions of the RFC stabilized the banking industry, new legislation was needed to prevent future banking crises. The Glass-

These measures were clearly successful, and the United States enjoyed a long period of financial and banking stability. As memories of the bad old days dimmed, Depression-

The Savings and Loan Crisis of the 1980s

A savings and loan (thrift) is another type of deposit-

Along with banks, the banking industry also included savings and loans (also called S&Ls or thrifts), institutions established to accept savings and turn them into long-

In order to improve S&Ls’ competitive position versus banks, Congress eased regulations to allow S&Ls to undertake much more risky investments in addition to long-

Not surprisingly, during the real estate boom of the 1970s and 1980s, S&Ls engaged in overly risky real estate lending. Also, corruption occurred as some S&L executives used their institutions as private piggy banks. By the early 1980s, a large number of S&Ls had failed. Because accounts were covered by federal deposit insurance, the liabilities of a failed S&L were now liabilities of the federal government. From 1986 through 1995, the federal government closed over 1,000 failed S&Ls, costing U.S. taxpayers over $124 billion.

In a classic case of shutting the barn door after the horse has escaped, in 1989 Congress put in place comprehensive oversight of S&L activities. It also empowered Fannie Mae and Freddie Mac to take over much of the home mortgage lending previously done by S&Ls. Fannie Mae and Freddie Mac are quasi-

Back to the Future: The Financial Crisis of 2008

The financial crisis of 2008 shared features of previous crises. Like the Panic of 1907 and the S&L crisis, it involved institutions that were not as strictly regulated as deposit-

Beginning in mid-

By the fall of 2010, the financial system was relatively stable, and major institutions had repaid much of the money the federal government had injected during the crisis. It was generally expected that taxpayers would end up losing little if any money. However, the recovery of the banks was not matched by a successful turnaround for the overall economy: although the recession that began in December 2007 officially ended in June 2009, unemployment remained stubbornly high.

Like earlier crises, the crisis of 2008 led to changes in banking regulation, most notably the Dodd-

Regulation After the 2008 Crisis

Regulation After the 2008 Crisis

In July 2010, President Obama signed the Wall Street Reform and Consumer Protection Act—

For the most part, it left regulation of traditional deposit-

The major changes came in the regulation of financial institutions other than banks—

Beyond this, the law established new rules on the trading of derivatives, those complex financial instruments that played an important role in the 2008 crisis: most derivatives would henceforth have to be bought and sold on exchanges, where everyone could observe their prices and the volume of transactions. The idea was to make the risks taken by financial institutions more transparent.

Overall, Dodd-