Money and Inflation

In the summer of 2008, the African nation of Zimbabwe achieved the unenviable distinction of having the world’s highest inflation rate: 11 million percent a year. Although the United States has not experienced the inflation levels that some countries have seen, in the late 1970s and early 1980s, consumer prices were rising at an annual rate as high as 13%. The policies that the Federal Reserve instituted to reduce this high level led to the deepest recession since the Great Depression. As we’ll see later, moderate levels of inflation such as those experienced in the United States—

To understand what causes inflation, we need to revisit the effect of changes in the money supply on the overall price level. Then we’ll turn to the reasons why governments sometimes increase the money supply very rapidly.

The Classical Model of Money and Prices

We learned that in the short run an increase in the money supply increases real GDP by lowering the interest rate and stimulating investment spending and consumer spending. However, in the long run, as nominal wages and other sticky prices rise, real GDP falls back to its original level. So in the long run, an increase in the money supply does not change real GDP. Instead, other things equal, it leads to an equal percentage rise in the overall price level; that is, the prices of all goods and services in the economy, including nominal wages and the prices of intermediate goods, rise by the same percentage as the money supply. And when the overall price level rises, the aggregate price level—

To repeat, this is what happens in the long run. When analyzing large changes in the aggregate price level, however, macroeconomists often find it useful to ignore the distinction between the short run and the long run. Instead, they work with a simplified model in which the effect of a change in the money supply on the aggregate price level takes place instantaneously rather than over a long period of time. You might be concerned about this assumption given the emphasis we’ve placed on the difference between the short run and the long run. However, for reasons we’ll explain shortly, this is a reasonable assumption to make in the case of high inflation.

According to the classical model of the price level, the real quantity of money is always at its long-

AP® Exam Tip

In the Keynesian model, sticky prices and wages slow the economy’s process of self correction. Classical economists believe that prices and wages are flexible enough to allow the economy to correct itself quickly.

The simplified model in which the real quantity of money, M/P, is always at its long-

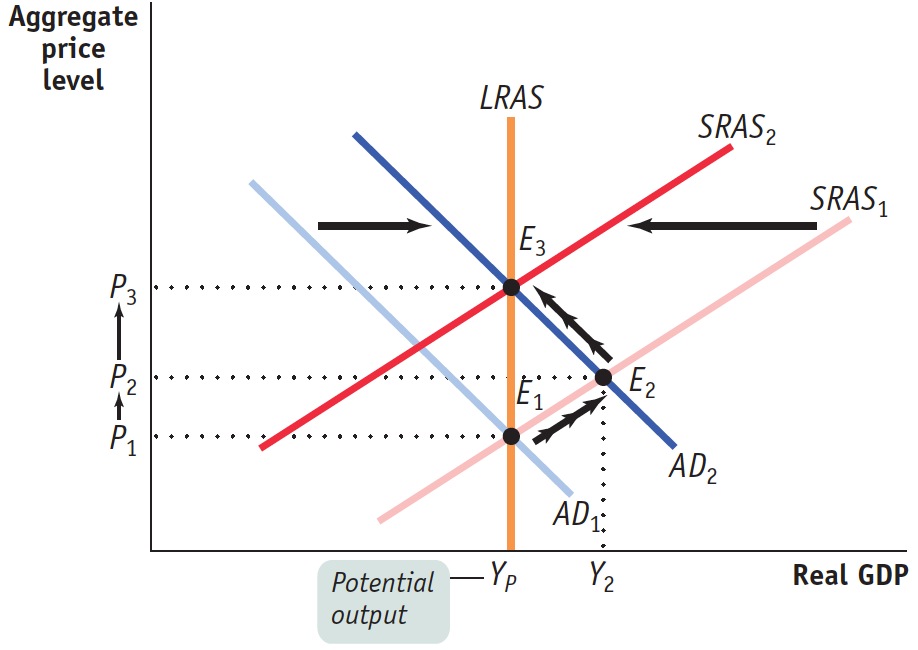

Figure 33.1 reviews the effects of an increase in the money supply according to the AD–

| Figure 33.1 | The Classical Model of the Price Level |

Now suppose there is an increase in the money supply. This is an expansionary monetary policy, which shifts the aggregate demand curve to the right, to AD2, and moves the economy to a new short-

The classical model of the price level ignores the short-

In reality, this is a poor assumption during periods of low inflation. With a low inflation rate, it may take a while for workers and firms to react to a monetary expansion by raising wages and prices. In this scenario, some nominal wages and the prices of some goods are sticky in the short run. As a result, under low inflation there is an upward-

But what about periods of high inflation? In the face of high inflation, economists have observed that the short-

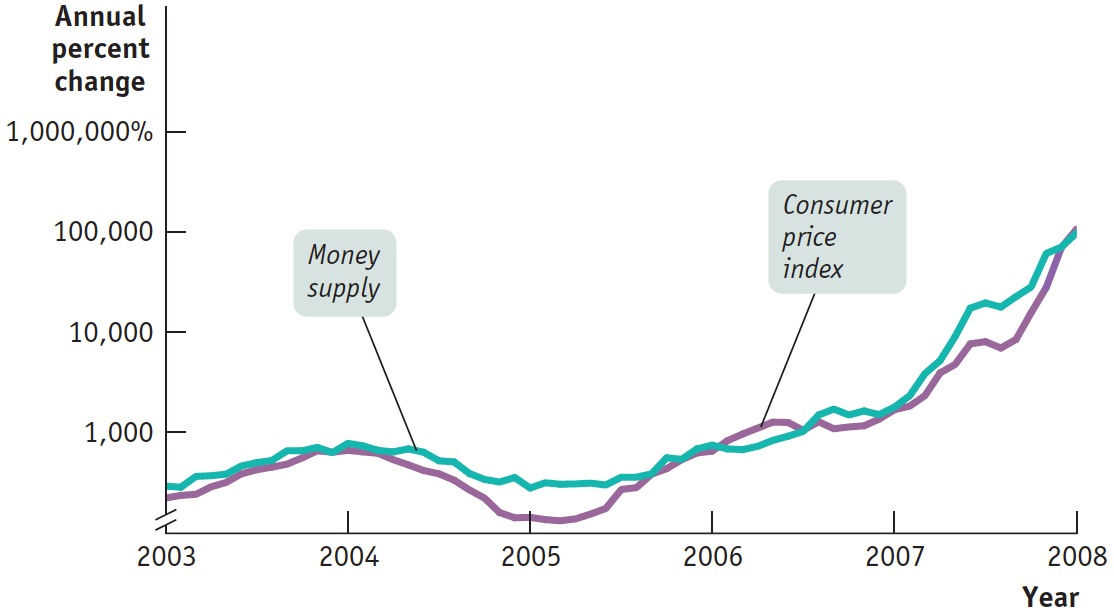

The consequence of this rapid adjustment of all prices in the economy is that in countries with persistently high inflation, changes in the money supply are quickly translated into changes in the inflation rate. Let’s look at Zimbabwe. Figure 33.2 shows the annual rate of growth in the money supply and the annual rate of change of consumer prices from 2003 through January 2008. As you can see, the surge in the growth rate of the money supply coincided closely with a roughly equal surge in the inflation rate. Note that to fit these very large percentage increases—

| Figure 33.2 | Money Supply Growth and Inflation in Zimbabwe |

In late 2008, Zimbabwe’s inflation rate reached 231 million percent. What leads a country to increase its money supply so much that the result is an inflation rate in the millions of percent?

The Inflation Tax

Modern economies use fiat money—

So what is to prevent a government from paying for some of its expenses not by raising taxes or borrowing but simply by printing money? Nothing. In fact, governments, including the U.S. government, do it all the time. How can the U.S. government do this, given that the Federal Reserve, not the U.S. Treasury, issues money? The answer is that the Treasury and the Federal Reserve work in concert. The Treasury issues debt to finance the government’s purchases of goods and services, and the Fed monetizes the debt by creating money and buying the debt back from the public through open-

For example, in February 2010, the U.S. monetary base—

An alternative way to look at this is to say that the right to print money is itself a source of revenue. Economists refer to the revenue generated by the government’s right to print money as seignorage, an archaic term that goes back to the Middle Ages. It refers to the right to stamp gold and silver into coins, and charge a fee for doing so, that medieval lords—

Seignorage accounts for only a tiny fraction (less than 1%) of the U.S. government’s budget. Furthermore, concerns about seignorage don’t have any influence on the Federal Reserve’s decisions about how much money to print; the Fed is worried about inflation and unemployment, not revenue. But this hasn’t always been true, even in the United States: both sides relied on seignorage to help cover budget deficits during the Civil War. And there have been many occasions in history when governments turned to their printing presses as a crucial source of revenue. According to the usual scenario, a government finds itself running a large budget deficit—

In such a situation, governments end up printing money to cover the budget deficit. But by printing money to pay its bills, a government increases the quantity of money in circulation. And as we’ve just seen, increases in the money supply translate into equally large increases in the aggregate price level. So printing money to cover a budget deficit leads to inflation.

An inflation tax is a reduction in the value of money held by the public caused by inflation.

Who ends up paying for the goods and services the government purchases with newly printed money? The people who currently hold money pay. They pay because inflation erodes the purchasing power of their money holdings. In other words, a government imposes an inflation tax, a reduction in the value of the money held by the public, by printing money to cover its budget deficit and creating inflation.

It’s helpful to think about what this tax represents. If the inflation rate is 5%, then a year from now $1 will buy goods and services worth only about $0.95 today. So a 5% inflation rate in effect imposes a tax rate of 5% on the value of all money held by the public.

But why would any government push the inflation tax to rates of hundreds or thousands of percent? We turn next to the process by which high inflation turns into explosive hyperinflation.

The Logic of Hyperinflation

Inflation imposes a tax on individuals who hold money. And, like most taxes, it will lead people to change their behavior. In particular, when inflation is high, people have a strong incentive to either spend money quickly or acquire interest-

We are now prepared to understand how countries can get themselves into situations of extreme inflation. Suppose the government prints enough money to pay for a given quantity of goods and services each month. The increase in the money supply causes the inflation rate to rise, which means the government must print more money each month to buy the same quantity of goods and services. If the desire to reduce money holdings causes people to spend money faster than the government prints money, prices increase faster than the money supply. As a result, the government must accelerate the rate of growth of the money supply, which leads to an even higher rate of inflation. As this process becomes self-

Here’s an analogy: imagine a city government that tries to raise a lot of money with a special fee on taxi rides. The fee will raise the cost of taxi rides, and this will cause people to turn to substitutes, such as walking or taking the bus. As taxi use declines, the government finds that its tax revenue declines and it must impose a higher fee to raise the same amount of revenue as before. You can imagine the ensuing vicious circle: the government imposes fees on taxi rides, which leads to less taxi use, which causes the government to raise the fee on taxi rides, which leads to even less taxi use, and so on.

Substitute the real money supply for taxi rides and the inflation rate for the increase in the fee on taxi rides, and you have the story of hyperinflation. A race develops between the government printing presses and the public: the presses churn out money at a faster and faster rate to try to compensate for the fact that the public is reducing its real money holdings. At some point the inflation rate explodes into hyperinflation, and people are unwilling to hold any money at all (and resort to trading in eggs and lumps of coal). The government is then forced to abandon its use of the inflation tax and shut down the printing presses.

Zimbabwe’s Inflation

Zimbabwe’s Inflation

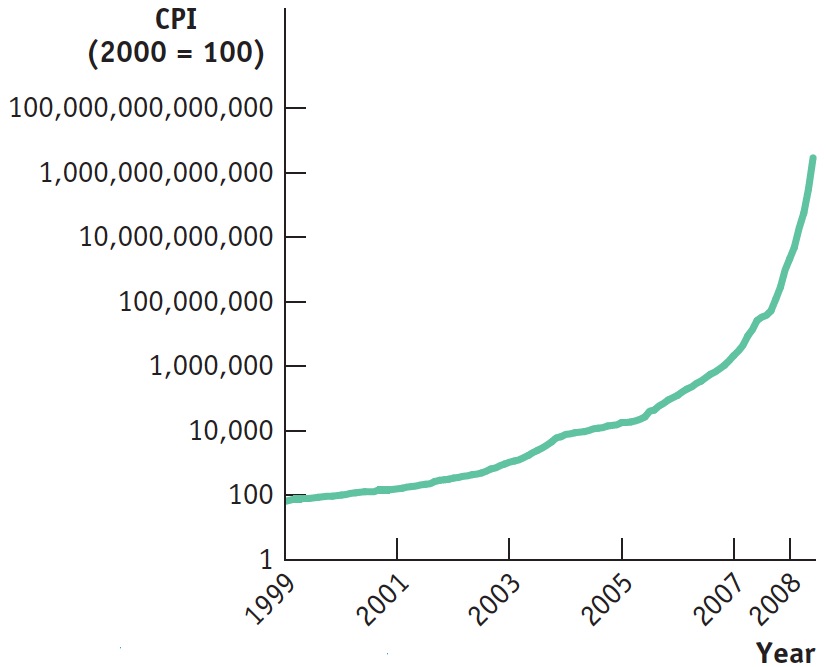

Zimbabwe offers a recent example of a country experiencing very high inflation. Figure 33.2 showed that surges in Zimbabwe’s money supply growth were matched by almost simultaneous surges in its inflation rate. But looking at rates of change doesn’t give a true feel for just how much prices went up.

The figure here shows Zimbabwe’s consumer price index from 1999 to June 2008, with the 2000 level set equal to 100. As in Figure 33.2, we use a logarithmic scale, which lets us draw equal-

Why did Zimbabwe’s government pursue policies that led to runaway inflation? The reason boils down to political instability, which in turn had its roots in Zimbabwe’s history. Until the 1970s, Zimbabwe had been ruled by its small white minority; even after the shift to majority rule, many of the country’s farms remained in the hands of whites. Eventually Robert Mugabe, Zimbabwe’s president, tried to solidify his position by seizing these farms and turning them over to his political supporters. But because this seizure disrupted production, the result was to undermine the country’s economy and its tax base. It became impossible for the country’s government to balance its budget either by raising taxes or by cutting spending. At the same time, the regime’s instability left Zimbabwe unable to borrow money in world markets. Like many others before it, Zimbabwe’s government turned to the printing press to cover the gap—