Inflation and Deflation

As we mentioned in the opening story, in early 2011 British officials were worried about two things: the unemployment rate was high and so was inflation. And there was a fierce debate about which concern should take priority.

Why is inflation something to worry about? Why do policy makers even now get anxious when they see the inflation rate moving upward? The answer is that inflation can impose costs on the economy—but not in the way most people think.

The Level of Prices Doesn’t Matter…

The most common complaint about inflation, an increase in the price level, is that it makes everyone poorer—after all, a given amount of money buys less. But inflation does not make everyone poorer. To see why, it’s helpful to imagine what would happen if the United States did something other countries have done from time to time—replacing the dollar with a new currency.

An example of this kind of currency conversion happened in 2002, when France, like a number of other European countries, replaced its national currency, the franc, with the new pan-European currency, the euro. People turned in their franc coins and notes, and received euro coins and notes in exchange, at a rate of precisely 6.55957 francs per euro. At the same time, all contracts were restated in euros at the same rate of exchange. For example, if a French citizen had a home mortgage debt of 500,000 francs, this became a debt of 500,000/6.55957 = 76,224.51 euros. If a worker’s contract specified that he or she should be paid 100 francs per hour, it became a contract specifying a wage of 100/6.55957 = 5.2449 euros per hour, and so on.

You could imagine doing the same thing here, replacing the dollar with a “new dollar” at a rate of exchange of, say, 7 to 1. If you owed $140,000 on your home, that would become a debt of 20,000 new dollars. If you had a wage rate of $14 an hour, it would become 2 new dollars an hour, and so on. This would bring the overall U.S. price level back to about what it was in 1962, when John F. Kennedy was president.

The real wage is the wage rate divided by the price level.

So would everyone be richer as a result because prices would be only one-seventh as high? Of course not. Prices would be lower, but so would wages and incomes in general. If you cut a worker’s wage to one-seventh of its previous value, but also cut all prices to one-seventh of their previous level, the worker’s real wage—the wage rate divided by the price level—hasn’t changed. In fact, bringing the overall price level back to what it was during the Kennedy administration would have no effect on overall purchasing power because doing so would reduce income exactly as much as it reduced prices.

Real income is income divided by the price level.

Conversely, the rise in prices that has actually taken place since the early 1960s hasn’t made America poorer because it has also raised incomes by the same amount: real incomes—incomes divided by the price level—haven’t been affected by the rise in overall prices.

The moral of this story is that the level of prices doesn’t matter: the United States would be no richer than it is now if the overall level of prices was still as low as it was in 1961; conversely, the rise in prices over the past 50 years hasn’t made us poorer.

…But the Rate of Change of Prices Does

The conclusion that the level of prices doesn’t matter might seem to imply that the inflation rate doesn’t matter either. But that’s not true.

To see why, it’s crucial to distinguish between the level of prices and the inflation rate: the percent increase in the overall level of prices per year. Recall from Chapter 11 that the inflation rate is defined as follows:

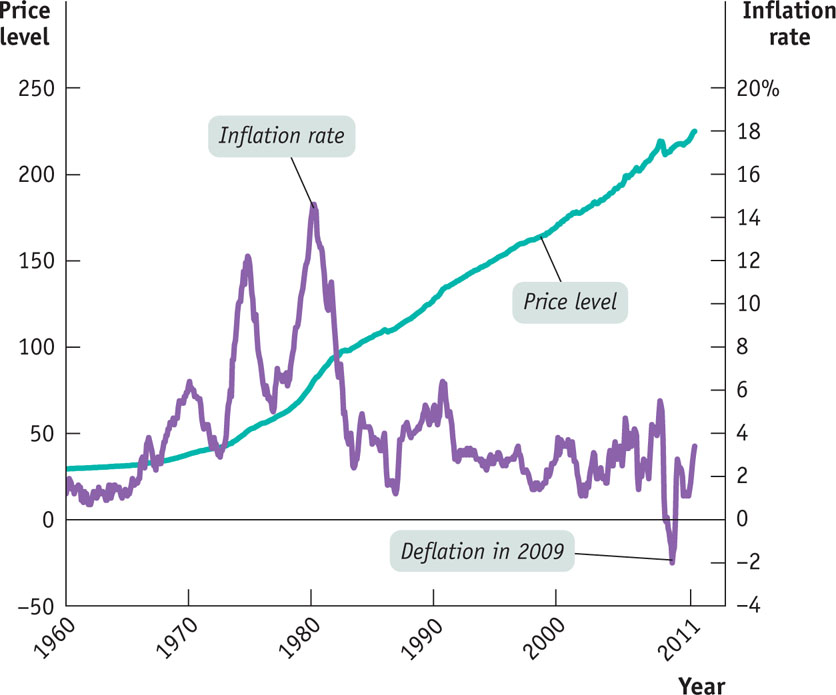

Figure 12-11 highlights the difference between the price level and the inflation rate in the United States over the last half-century, with the price level measured along the left vertical axis and the inflation rate measured along the right vertical axis. In the 2000s, the overall level of prices in America was much higher than it had been in 1960—but that, as we’ve learned, didn’t matter. The inflation rate in the 2000s, however, was much lower than in the 1970s—and that almost certainly made the economy richer than it would have been if high inflation had continued.

Economists believe that high rates of inflation impose significant economic costs. The most important of these costs are shoe-leather costs, menu costs, and unit-of-account costs. We’ll discuss each in turn.

Shoe-Leather Costs People hold money—cash in their wallets and bank deposits on which they can write checks—for convenience in making transactions. A high inflation rate, however, discourages people from holding money because the purchasing power of the cash in your wallet and the funds in your bank account steadily erodes as the overall level of prices rises. This leads people to search for ways to reduce the amount of money they hold, often at considerable economic cost.

The Economics in Action at the end of this section describes how Israelis spent a lot of time at the bank during the periods of high inflation rates that afflicted Israel in 1984–1985. During the most famous of all inflations, the German hyperinflation of 1921–1923, merchants employed runners to take their cash to the bank many times a day to convert it into something that would hold its value, such as a stable foreign currency. In each case, in an effort to avoid having the purchasing power of their money eroded, people used up valuable resources, such as time for Israeli citizens and the labor of those German runners that could have been used productively elsewhere. During the German hyperinflation, so many banking transactions were taking place that the number of employees at German banks nearly quadrupled—from around 100,000 in 1913 to 375,000 in 1923.

More recently, Brazil experienced hyperinflation during the early 1990s; during that episode, the Brazilian banking sector grew so large that it accounted for 15% of GDP, more than twice the size of the financial sector in the United States measured as a share of GDP. The large increase in the Brazilian banking sector needed to cope with the consequences of inflation represented a loss of real resources to its society.

Shoe-leather costs are the increased costs of transactions caused by inflation.

Increased costs of transactions caused by inflation are known as shoe-leather costs, an allusion to the wear and tear caused by the extra running around that takes place when people are trying to avoid holding money. Shoe-leather costs are substantial in economies with very high inflation, as anyone who has lived in such an economy—say, one suffering inflation of 100% or more per year—can attest. Most estimates suggest, however, that the shoe-leather costs of inflation at the rates seen in the United States—which in peacetime has never had inflation above 15%—are quite small.

The menu cost is the real cost of changing a listed price.

Menu Costs In a modern economy, most of the things we buy have a listed price. There’s a price listed under each item on a supermarket shelf, a price printed on the back of a book, a price listed for each dish on a restaurant’s menu. Changing a listed price has a real cost, called a menu cost. For example, to change prices in a supermarket requires sending clerks through the store to change the listed price under each item. In the face of inflation, of course, firms are forced to change prices more often than they would if the aggregate price level was more or less stable. This means higher costs for the economy as a whole.

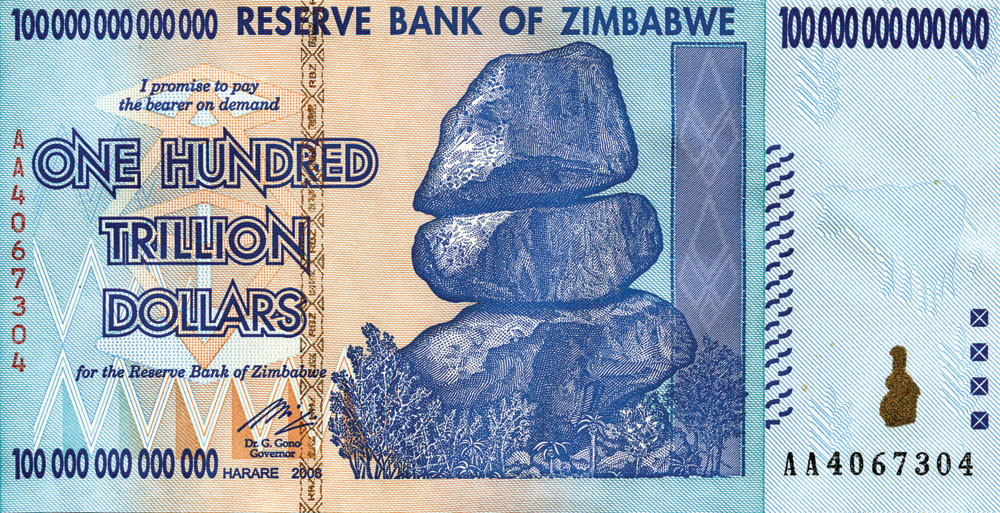

In times of very high inflation, menu costs can be substantial. During the Brazilian inflation of the early 1990s, for instance, supermarket workers reportedly spent half of their time replacing old price stickers with new ones. When inflation is high, merchants may decide to stop listing prices in terms of the local currency and use either an artificial unit—in effect, measuring prices relative to one another—or a more stable currency, such as the U.S. dollar. This is exactly what the Israeli real estate market began doing in the mid-1980s: prices were quoted in U.S. dollars, even though payment was made in Israeli shekels. And this is also what happened in Zimbabwe when, in May 2008, official estimates of the inflation rate reached 1,694,000%. By 2009, the government had suspended the Zimbabwean dollar, allowing Zimbabweans to buy and sell goods using foreign currencies.

Menu costs are also present in low-inflation economies, but they are not severe. In low-inflation economies, businesses might update their prices only sporadically—not daily or even more frequently, as is the case in high-inflation or hyperinflation economies. Also, with technological advances, menu costs are becoming less and less important, since prices can be changed electronically and fewer merchants attach price stickers to merchandise.

Unit-of-Account Costs In the Middle Ages, contracts were often specified “in kind”: a tenant might, for example, be obliged to provide his landlord with a certain number of cattle each year (the phrase in kind actually comes from an ancient word for cattle). This may have made sense at the time, but it would be an awkward way to conduct modern business. Instead, we state contracts in monetary terms: a renter owes a certain number of dollars per month, a company that issues a bond promises to pay the bondholder the dollar value of the bond when it comes due, and so on. We also tend to make our economic calculations in dollars: a family planning its budget, or a small business owner trying to figure out how well the business is doing, makes estimates of the amount of money coming in and going out.

Unit-of-account costs arise from the way inflation makes money a less reliable unit of measurement.

This role of the dollar as a basis for contracts and calculation is called the unit-of-account role of money. It’s an important aspect of the modern economy. Yet it’s a role that can be degraded by inflation, which causes the purchasing power of a dollar to change over time—a dollar next year is worth less than a dollar this year. The effect, many economists argue, is to reduce the quality of economic decisions: the economy as a whole makes less efficient use of its resources because of the uncertainty caused by changes in the unit of account, the dollar. The unit-of-account costs of inflation are the costs arising from the way inflation makes money a less reliable unit of measurement.

Unit-of-account costs may be particularly important in the tax system because inflation can distort the measures of income on which taxes are collected. Here’s an example: Assume that the inflation rate is 10%, so the overall level of prices rises 10% each year. Suppose that a business buys an asset, such as a piece of land, for $100,000, then resells it a year later for $110,000. In a fundamental sense, the business didn’t make a profit on the deal: in real terms, it got no more for the land than it paid for it. But U.S. tax law would say that the business made a capital gain of $10,000, and it would have to pay taxes on that phantom gain.

During the 1970s, when the United States had relatively high inflation, the distorting effects of inflation on the tax system were a serious problem. Some businesses were discouraged from productive investment spending because they found themselves paying taxes on phantom gains. Meanwhile, some unproductive investments became attractive because they led to phantom losses that reduced tax bills. When inflation fell in the 1980s—and tax rates were reduced—these problems became much less important.

Winners and Losers from Inflation

As we’ve just learned, a high inflation rate imposes overall costs on the economy. In addition, inflation can produce winners and losers within the economy. The main reason inflation sometimes helps some people while hurting others is that economic transactions often involve contracts that extend over a period of time, such as loans, and these contracts are normally specified in nominal—that is, in dollar—terms.

The interest rate on a loan is the price, calculated as a percentage of the amount borrowed, that a lender charges a borrower for the use of their savings for one year.

The nominal interest rate is the interest rate expressed in dollar terms.

The real interest rate is the nominal interest rate minus the rate of inflation.

In the case of a loan, the borrower receives a certain amount of funds at the beginning, and the loan contract specifies the interest rate on the loan and when it must be paid off. The interest rate is the return a lender receives for allowing borrowers the use of their savings for one year, calculated as a percentage of the amount borrowed.

But what that dollar is worth in real terms—that is, in terms of purchasing power—depends greatly on the rate of inflation over the intervening years of the loan. Economists summarize the effect of inflation on borrowers and lenders by distinguishing between the nominal interest rate and the real interest rate. The nominal interest rate is the interest rate in dollar terms—for example, the interest rate on a student loan. The real interest rate is the nominal interest rate minus the rate of inflation. For example, if a loan carries an interest rate of 8%, but there is 5% inflation, the real interest rate is 8% − 5% = 3%.

When a borrower and a lender enter into a loan contract, the contract is normally written in dollar terms—that is, the interest rate it specifies is a nominal interest rate. (And in later chapters, when we say the interest rate we will mean the nominal interest rate unless noted otherwise.) But each party to a loan contract has an expectation about the future rate of inflation and therefore an expectation about the real interest rate on the loan. If the actual inflation rate is higher than expected, borrowers gain at the expense of lenders: borrowers will repay their loans with funds that have a lower real value than had been expected. Conversely, if the inflation rate is lower than expected, lenders will gain at the expense of borrowers: borrowers must repay their loans with funds that have a higher real value than had been expected.

Historically, the fact that inflation creates winners and losers has sometimes been a major source of political controversy. In 1896 William Jennings Bryan electrified the Democratic presidential convention with a speech in which he declared, “You shall not crucify mankind on a cross of gold.” What he was actually demanding was an inflationary policy. At the time, the U.S. dollar had a fixed value in terms of gold. Bryan wanted to abandon that gold standard and have the U.S. government print more money, which would have raised the level of prices. The reason he wanted inflation was to help farmers, many of whom were deeply in debt.

In modern America, home mortgages are the most important source of gains and losses from inflation. Americans who took out mortgages in the early 1970s quickly found their real payments reduced by higher-than-expected inflation: by 1983, the purchasing power of a dollar was only 45% of what it had been in 1973. Those who took out mortgages in the early 1990s were not so lucky, because the inflation rate fell to lower-than-expected levels in the following years: in 2003 the purchasing power of a dollar was 78% of what it had been in 1993.

Because gains for some and losses for others result from inflation that is either higher or lower than expected, yet another problem arises: uncertainty about the future inflation rate discourages people from entering into any form of long-term contract. This is an additional cost of high inflation, because high rates of inflation are usually unpredictable. In countries with high and uncertain inflation, long-term loans are rare, which makes it difficult in many cases to make long-term investments.

One last point: unexpected deflation—a surprise fall in the price level—creates winners and losers, too. Between 1929 and 1933, as the U.S. economy plunged into the Great Depression, the consumer price index fell by 35%. This meant that debtors, including many farmers and homeowners, saw a sharp rise in the real value of their debts, which led to widespread bankruptcy and helped create a banking crisis, as lenders found their customers unable to pay back their loans. And as you can see in Figure 12-11, deflation occurred again in 2009, when the inflation rate fell to −2% at the trough of a deep recession. Like the Great Depression (but to a much lesser extent), the unexpected deflation of 2009 imposed heavy costs on debtors.

Inflation is Easy; Disinflation is Hard

Disinflation is the process of bringing the inflation rate down.

There is not much evidence that a rise in the inflation rate from, say, 2% to 5% would do a great deal of harm to the economy. Still, policy makers generally move forcefully to bring inflation back down when it creeps above 2% or 3%. Why? Because experience shows that bringing the inflation rate down—a process called disinflation—is very difficult and costly once a higher rate of inflation has become well established in the economy.

Figure 12-12 shows what happened during two major episodes of disinflation in the United States, in the mid-1970s and in the early 1980s. The horizontal axis shows the unemployment rate. The vertical axis shows “core” inflation over the previous year, a measure that excludes volatile food and energy prices and is widely considered a better measure of underlying inflation than overall consumer prices. Each marker represents the inflation rate and the unemployment rate for one month. In each episode, unemployment and inflation followed a sort of clockwise spiral, with high inflation gradually falling in the face of an extended period of very high unemployment.

FIGURE 12-12 The Cost of Disinflation

According to many economists, these periods of high unemployment that temporarily depressed the economy were necessary to reduce inflation that had become deeply embedded in the economy. The best way to avoid having to put the economy through a wringer to reduce inflation, however, is to avoid having a serious inflation problem in the first place. So policy makers respond forcefully to signs that inflation may be accelerating as a form of preventive medicine for the economy.

Israel’s Experience with Inflation

It’s often hard to see the costs of inflation clearly because serious inflation problems are often associated with other problems that disrupt economic life, notably war or political instability (or both). In the mid-1980s, however, Israel experienced a “clean” inflation: there was no war, the government was stable, and there was order in the streets. Yet a series of policy errors led to very high inflation, with prices often rising more than 10% a month.

As it happens, one of the authors spent a month visiting at Tel Aviv University at the height of the inflation, so we can give a first-hand account of the effects.

First, the shoe-leather costs of inflation were substantial. At the time, Israelis spent a lot of time in lines at the bank, moving money in and out of accounts that provided high enough interest rates to offset inflation. People walked around with very little cash in their wallets; they had to go to the bank whenever they needed to make even a moderately large cash payment. Banks responded by opening a lot of branches, a costly business expense.

Second, although menu costs weren’t that visible to a visitor, what you could see were the efforts businesses made to minimize them. For example, restaurant menus often didn’t list prices. Instead, they listed numbers that you had to multiply by another number, written on a chalkboard and changed every day, to figure out the price of a dish.

Finally, it was hard to make decisions because prices changed so much and so often. It was a common experience to walk out of a store because prices were 25% higher than at one’s usual shopping destination, only to discover that prices had just been increased 25% there, too.

Quick Review

- The real wage and real income are unaffected by the level of prices.

- Inflation, like unemployment, is a major concern of policy makers—so much so that in the past they have accepted high unemployment as the price of reducing inflation.

- While the overall level of prices is irrelevant, high rates of inflation impose real costs on the economy: shoe-leather costs, menu costs, and unit-of-account costs.

- The interest rate is the return a lender receives for use of his or her funds for a year. The real interest rate is equal to the nominal interest rate minus the inflation rate. As a result, unexpectedly high inflation helps borrowers and hurts lenders. With high and uncertain inflation, people will often avoid long-term investments.

- Disinflation is very costly, so policy makers try to avoid getting into situations of high inflation in the first place.

Check Your Understanding 12-3

Question

The widespread use of technology has revolutionized the banking industry, making it much easier for customers to access and manage their assets. Does this mean that the shoe-leather costs of inflation are higher or lower than they used to be?

A. B. Shoeleather costs as a result of inflation will be lower because it is now less costly for individuals to manage their assets in order to economize on their money holdings. This reduction in the costs associated with converting non-money assets into money translates into lower shoe-leather costs.Question

Most people in the United States have grown accustomed to a modest inflation rate of around 2% to 3%. Who would gain and who would lose if inflation came to a complete stop over the next 15 or 20 years?

A. B. C. If inflation came to a complete stop over the next 15 or 20 years, the inflation rate would be zero, which of course is less than the expected inflation rate of 2 to 3%. Because the real interest rate is the nominal interest rate minus the inflation rate, the real interest rate on a loan would be higher than expected, and lenders would gain at the expense of borrowers. Borrowers would have to repay their loans with funds that have a higher real value than had been expected.

Solutions appear at back of book.