Pacific Investment Management Company, generally known as PIMCO, is one of the world’s largest investment companies. Among other things, it runs PIMCO Total Return, the world’s second-largest mutual fund. The head of PIMCO, Bill Gross, is legendary for his ability to predict trends in financial markets, especially bond markets, where PIMCO does much of its investing.

In the fall of 2009, Gross decided to put more of PIMCO’s assets into long-term U.S. government bonds. This amounted to a bet that long-term interest rates would fall. This bet was especially interesting because it was the opposite of the bet many other investors were making. For example, in November 2009 the investment bank Morgan Stanley told its clients to expect a sharp rise in long-term interest rates.

Stephen VanHorn/Shutterstock

What lay behind PIMCO’s bet? Gross explained the firm’s thinking in his September 2009 commentary. He suggested that unemployment was likely to stay high and inflation low. “Global policy rates,” he asserted—meaning the federal funds rate and its equivalents in Europe and elsewhere—“will remain low for extended periods of time.”

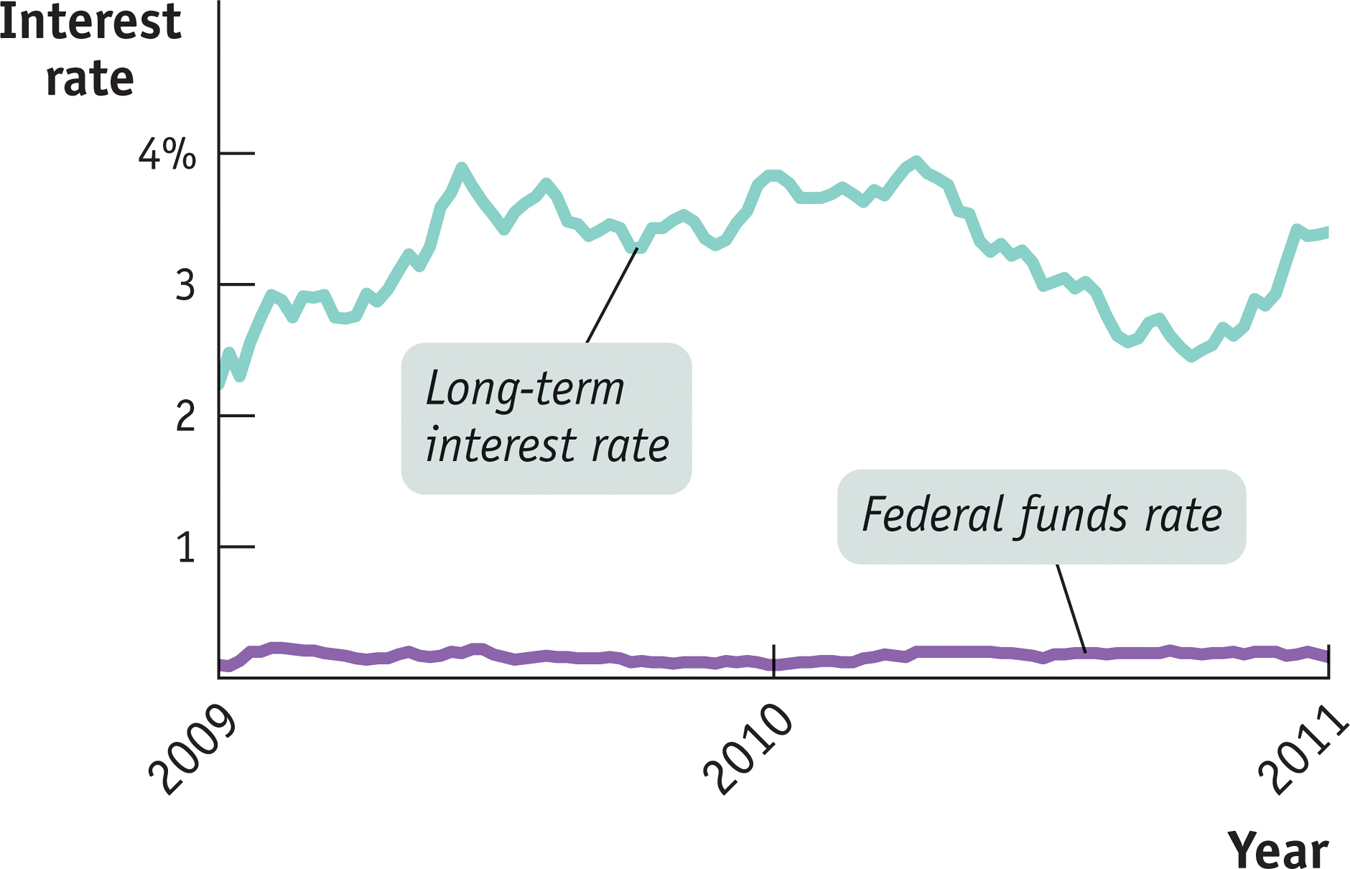

The Federal Funds Rate and Long-Term Interest Rates, 2009–2011

Source: Federal Reserve Bank of St. Louis.

PIMCO’s view was in sharp contrast to those of other investors: Morgan Stanley expected long-term rates to rise in part because it expected the Fed to raise the federal funds rate in 2010.

Who was right? PIMCO, mostly. As the accompanying figure shows, the federal funds rate stayed near zero, and long-term interest rates fell through much of 2010, although they rose somewhat very late in the year as investors became somewhat more optimistic about economic recovery.

Morgan Stanley, which had bet on rising rates, actually apologized to investors for getting it so wrong.

Bill Gross’s foresight, however, was a lot less accurate in 2011. Anticipating a significantly stronger U.S. economy by mid-2011 that would result in inflation, Gross bet heavily against U.S. government bonds early that year. But this time he was wrong, as weak growth continued. By late summer 2011, Gross realized his mistake as U.S. bonds rose in value and the value of his funds sank. He admitted to the Wall Street Journal that he had “lost sleep” over his bet, and called it a “mistake.”

Questions for Thought

Question

1.Why did PIMCO’s view that unemployment would stay high and inflation low lead to a forecast that policy interest rates would remain low for an extended period?

Why did PIMCO’s view that unemployment would stay high and inflation low lead to a forecast that policy interest rates would remain low for an extended period?

Question

2.Why would low policy rates suggest low long-term interest rates?

Why would low policy rates suggest low long-term interest rates?

Question

3.What might have caused long-term interest rates to rise in late 2010, even though the federal funds rate was still zero?

What might have caused long-term interest rates to rise in late 2010, even though the federal funds rate was still zero?