The Business Cycle and the Cyclically Adjusted Budget Balance

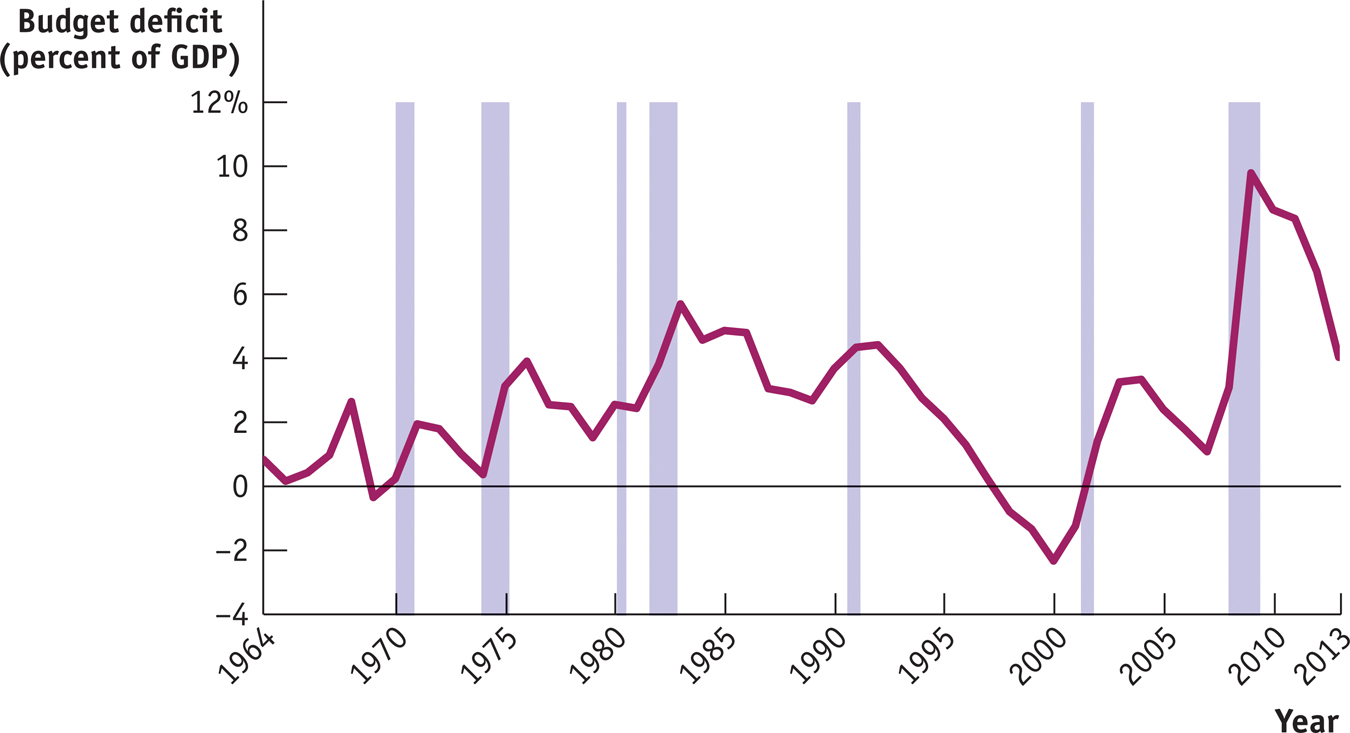

Historically there has been a strong relationship between the federal government’s budget balance and the business cycle. The budget tends to move into deficit when the economy experiences a recession, but deficits tend to get smaller or even turn into surpluses when the economy is expanding. Figure 13-8 shows the federal budget deficit as a percentage of GDP from 1964 to 2013. Shaded areas indicate recessions; unshaded areas indicate expansions. As you can see, the federal budget deficit increased around the time of each recession and usually declined during expansions. In fact, in the late stages of the long expansion from 1991 to 2000, the deficit actually became negative—

The relationship between the business cycle and the budget balance is even clearer if we compare the budget deficit as a percentage of GDP with the unemployment rate, as we do in Figure 13-9. The budget deficit almost always rises when the unemployment rate rises and falls when the unemployment rate falls.

Is this relationship between the business cycle and the budget balance evidence that policy makers engage in discretionary fiscal policy, using expansionary fiscal policy during recessions and contractionary fiscal policy during expansions? Not necessarily. To a large extent the relationship in Figure 13-9 reflects automatic stabilizers at work. As we saw earlier in the discussion of automatic stabilizers, government tax revenue tends to rise and some government transfers, like unemployment benefit payments, tend to fall when the economy expands. Conversely, government tax revenue tends to fall and some government transfers tend to rise when the economy contracts. So the budget tends to move toward surplus during expansions and toward deficit during recessions even without any deliberate action on the part of policy makers.

In assessing budget policy, it’s often useful to separate movements in the budget balance due to the business cycle from movements due to discretionary fiscal policy changes. The former are affected by automatic stabilizers and the latter by deliberate changes in government purchases, government transfers, or taxes. It’s important to realize that business-

In other words, do the government’s tax policies yield enough revenue to fund its spending in the long run? As we’ll learn shortly, this is a fundamentally more important question than whether the government runs a budget surplus or deficit in the current year.

The cyclically adjusted budget balance is an estimate of what the budget balance would be if real GDP were exactly equal to potential output.

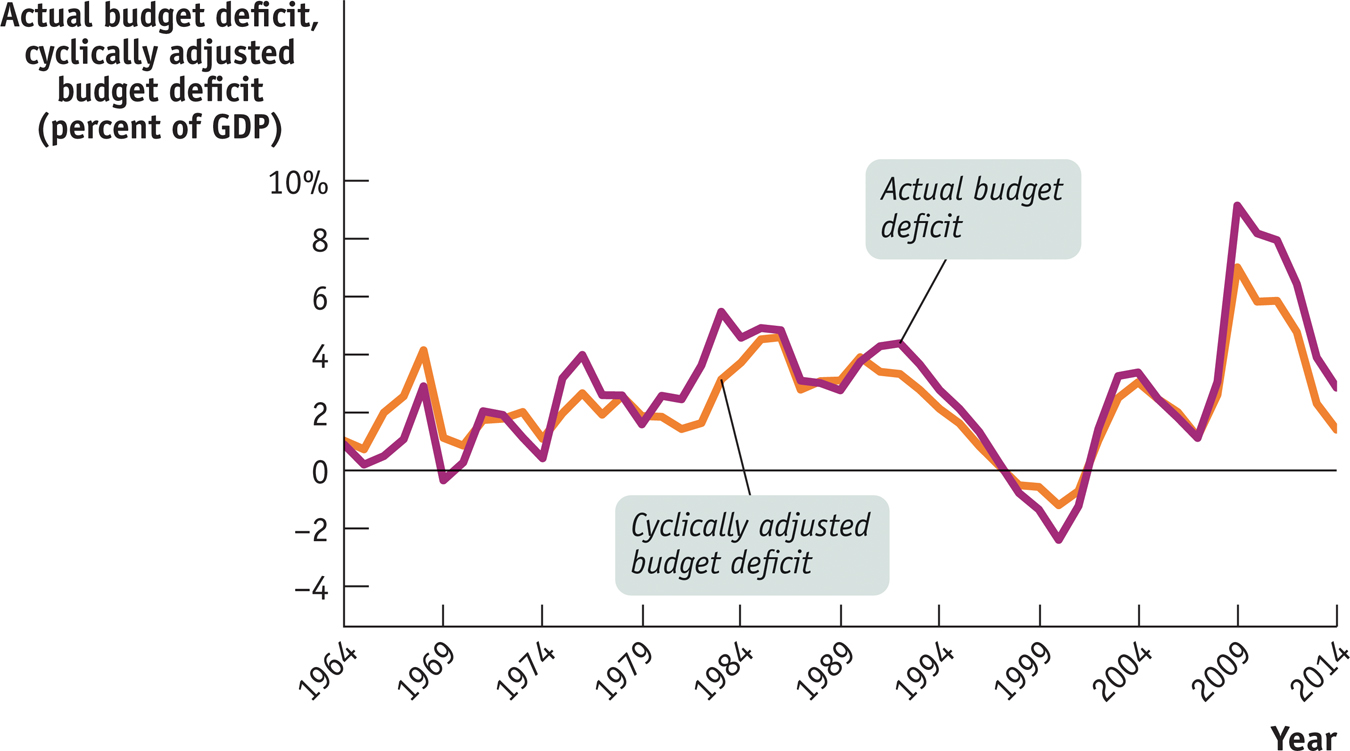

To separate the effect of the business cycle from the effects of other factors, many governments produce an estimate of what the budget balance would be if there were neither a recessionary nor an inflationary gap. The cyclically adjusted budget balance is an estimate of what the budget balance would be if real GDP were exactly equal to potential output. It takes into account the extra tax revenue the government would collect and the transfers it would save if a recessionary gap were eliminated—

Figure 13-10 shows the actual budget deficit and the Congressional Budget Office estimate of the cyclically adjusted budget deficit, both as a percentage of GDP, from 1964 to 2014. As you can see, the cyclically adjusted budget deficit doesn’t fluctuate as much as the actual budget deficit. In particular, large actual deficits, such as those of 1975, 1983, and 2009, are usually caused in part by a depressed economy.