Inflation Targeting

Inflation targeting occurs when the central bank sets an explicit target for the inflation rate and sets monetary policy in order to hit that target.

Until January 2012, the Fed did not explicitly commit itself to achieving a particular inflation rate. However, in January 2012, the Fed announced that it would set its policy to maintain an approximately 2% inflation rate per year. With that statement, the Fed joined a number of other central banks that have explicit inflation targets. So rather than using a Taylor rule to set monetary policy, they instead announce the inflation rate that they want to achieve—

Inflation Targets

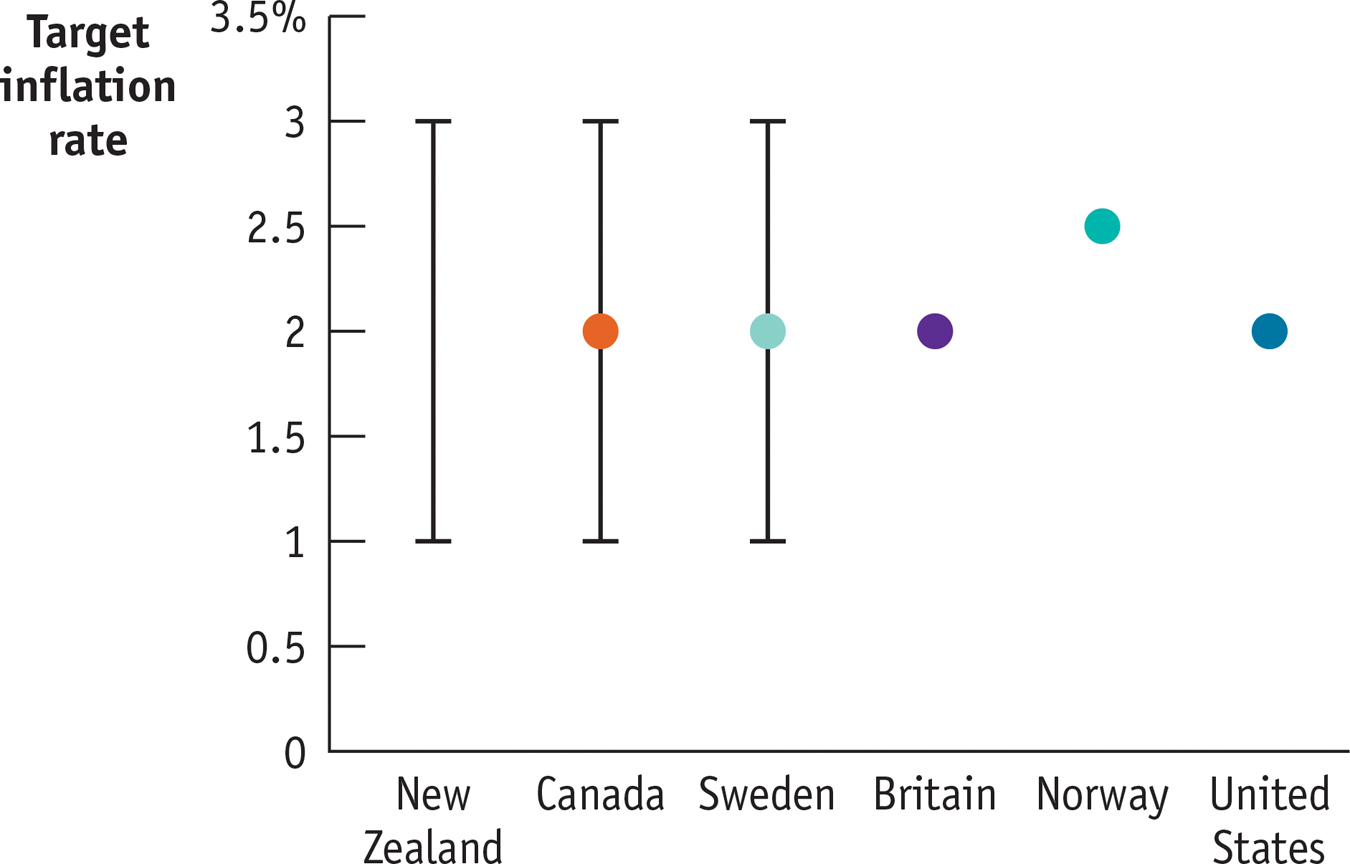

This figure shows the target inflation rates of six central banks that have adopted inflation targeting. The central bank of New Zealand introduced inflation targeting in 1990. Today it has an inflation target range of from 1% to 3%. The central banks of Canada and Sweden have the same target range but also specify 2% as the precise target. The central banks of Britain and Norway have specific targets for inflation, 2% and 2.5%, respectively. Neither states by how much they’re prepared to miss those targets. Since 2012, the U.S. Federal Reserve also targets inflation at 2%.

In practice, these differences in detail don’t seem to lead to any significant difference in results. New Zealand aims for the middle of its range, at 2% inflation; Britain, Norway, and the United States allow themselves considerable wiggle room around their target inflation rates.

Other central banks commit themselves to achieving a specific number. For example, the Bank of England has committed to keeping inflation at 2%. In practice, there doesn’t seem to be much difference between these versions: central banks with a target range for inflation seem to aim for the middle of that range, and central banks with a fixed target tend to give themselves considerable wiggle room.

One major difference between inflation targeting and the Taylor rule method is that inflation targeting is forward-

Advocates of inflation targeting argue that it has two key advantages over a Taylor rule: transparency and accountability. First, economic uncertainty is reduced because the central bank’s plan is transparent: the public knows the objective of an inflation-

Critics of inflation targeting argue that it’s too restrictive because there are times when other concerns—

Many American macroeconomists have had positive things to say about inflation targeting—