19-2 Problems in Measurement

The government budget deficit equals government spending minus government revenue, which in turn equals the amount of new debt the government needs to issue to finance its operations. This definition may sound simple enough, but in fact debates over fiscal policy sometimes arise over how the budget deficit should be measured. Some economists believe that the deficit as currently measured is not a good indicator of the stance of fiscal policy. That is, they believe that the budget deficit does not accurately gauge either the impact of fiscal policy on today’s economy or the burden being placed on future generations of taxpayers. In this section we discuss four problems with the usual measure of the budget deficit.

561

Measurement Problem 1: Inflation

The least controversial of the measurement issues is the correction for inflation. Almost all economists agree that the government’s indebtedness should be measured in real terms, not in nominal terms. The measured deficit should equal the change in the government’s real debt, not the change in its nominal debt.

The budget deficit as commonly measured, however, does not correct for inflation. To see how large an error this induces, consider the following example. Suppose that the real government debt is not changing; in other words, in real terms, the budget is balanced. In this case, the nominal debt must be rising at the rate of inflation. That is,

ΔD/D = π,

where π is the inflation rate and D is the stock of government debt. This implies

ΔD = πD.

The government would look at the change in the nominal debt ΔD and would report a budget deficit of πD. Hence, most economists believe that the reported budget deficit is overstated by the amount πD.

We can make the same argument in another way. The deficit is government expenditure minus government revenue. Part of expenditure is the interest paid on the government debt. Expenditure should include only the real interest paid on the debt rD, not the nominal interest paid iD. Because the difference between the nominal interest rate i and the real interest rate r is the inflation rate π, the budget deficit is overstated by πD.

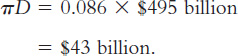

This correction for inflation can be large, especially when inflation is high, and it can often change our evaluation of fiscal policy. For example, in 1979, the federal government reported a budget deficit of $28 billion. Inflation was 8.6 percent, and the government debt held at the beginning of the year by the public (excluding the Federal Reserve) was $495 billion. The deficit was therefore overstated by

Corrected for inflation, the reported budget deficit of $28 billion turns into a budget surplus of $15 billion! In other words, even though nominal government debt was rising, real government debt was falling. This correction has been less important in recent years, because inflation has been low.

Measurement Problem 2: Capital Assets

Many economists believe that an accurate assessment of the government’s budget deficit requires taking into account the government’s assets as well as its liabilities. In particular, when measuring the government’s overall indebtedness, we should subtract government assets from government debt. Therefore, the budget deficit should be measured as the change in debt minus the change in assets.

562

Certainly, individuals and firms treat assets and liabilities symmetrically. When a person borrows to buy a house, we do not say that she is running a budget deficit. Instead, we offset the increase in assets (the house) against the increase in debt (the mortgage) and record no change in net wealth. Perhaps we should treat the government’s finances the same way.

A budget procedure that accounts for assets as well as liabilities is called capital budgeting because it takes into account changes in capital. For example, suppose that the government sells one of its office buildings or some of its land and uses the proceeds to reduce the government debt. Under current budget procedures, the reported deficit would be lower. Under capital budgeting, the revenue received from the sale would not lower the deficit because the reduction in debt would be offset by a reduction in assets. Similarly, under capital budgeting, government borrowing to finance the purchase of a capital good would not raise the deficit.

The major difficulty with capital budgeting is that it is hard to decide which government expenditures should count as capital expenditures. For example, should the interstate highway system be counted as an asset of the government? If so, what is its value? What about the stockpile of nuclear weapons? Should spending on education be treated as expenditure on human capital? These difficult questions must be answered if the government is to adopt a capital budget.

Reasonable people disagree about whether the federal government should use capital budgeting. (Many state governments already use it.) Opponents of capital budgeting argue that, although the system is superior in principle to the current system, it is too difficult to implement in practice. Proponents of capital budgeting argue that even an imperfect treatment of capital assets would be better than ignoring them altogether.

Measurement Problem 3: Uncounted Liabilities

Some economists argue that the measured budget deficit is misleading because it excludes some important government liabilities. For example, consider the pensions of government workers. These workers provide labor services to the government today, but part of their compensation is deferred to the future. In essence, these workers are providing a loan to the government. Their future pension benefits are a government liability not very different from government debt. Yet this liability is not included as part of the government debt, and the accumulation of this liability is not included as part of the budget deficit. According to some estimates, this implicit liability is almost as large as the official government debt.

Similarly, consider the Social Security system. In some ways, the system is like a pension plan. People pay some of their income into the system when young and expect to receive benefits when old. Perhaps accumulated future Social Security benefits should be included in the government’s liabilities. Estimates suggest that the government’s future Social Security liabilities (less future Social Security taxes) are more than three times the government debt as officially measured.

563

One might argue that Social Security liabilities are different from government debt because the government can change the laws determining Social Security benefits. Yet, in principle, the government could always choose not to repay all of its debt: the government honors its debt only because it chooses to do so. Promises to pay the holders of government debt may not be fundamentally different from promises to pay the future recipients of Social Security.

A particularly difficult form of government liability to measure is the contingent liability—the liability that is due only if a specified event occurs. For example, the government guarantees many forms of private credit, such as student loans, mortgages for low- and moderate-income families, and deposits in banks and savings-and-loan institutions. If the borrower repays the loan, the government pays nothing; if the borrower defaults, the government makes the repayment. When the government provides this guarantee, it undertakes a liability contingent on the borrower’s default. Yet this contingent liability is not reflected in the budget deficit, in part because it is not clear what dollar value to attach to it.

Measurement Problem 4: The Business Cycle

Many changes in the government’s budget deficit occur automatically in response to a fluctuating economy. When the economy goes into a recession, incomes fall, so people pay less in personal income taxes. Profits fall, so corporations pay less in corporate income taxes. Fewer people are employed, so payroll tax revenue declines. More people become eligible for government assistance, such as welfare and unemployment insurance, so government spending rises. Even without any change in the laws governing taxation and spending, the budget deficit increases.

These automatic changes in the deficit are not errors in measurement because the government truly borrows more when a recession depresses tax revenue and boosts government spending. But these changes do make it more difficult to use the deficit to monitor changes in fiscal policy. That is, the deficit can rise or fall either because the government has changed policy or because the economy has changed direction. For some purposes, it would be good to know which is occurring.

To solve this problem, the government calculates a cyclically adjusted budget deficit (sometimes called the full-employment budget deficit). The cyclically adjusted deficit is based on estimates of what government spending and tax revenue would be if the economy were operating at its natural level of output and employment. The cyclically adjusted deficit is a useful measure because it reflects policy changes but not the current stage of the business cycle.

Summing Up

Economists differ in the importance they place on these measurement problems. Some believe that the problems are so severe that the budget deficit as normally measured is almost meaningless. Most take these measurement problems seriously but still view the measured budget deficit as a useful indicator of fiscal policy.

564

The undisputed lesson is that to fully evaluate what fiscal policy is doing, economists and policymakers must look at more than just the measured budget deficit. And, in fact, they do. The budget documents prepared annually by the Office of Management and Budget contain much detailed information about the government’s finances, including data on capital expenditures and credit programs.

No economic statistic is perfect. Whenever we see a number reported in the media, we need to know what it is measuring and what it is leaving out. This is especially true for data on government debt and budget deficits.