9-3 Policies to Promote Growth

So far we have used the Solow model to uncover the theoretical relationships among the different sources of economic growth, and we have discussed some of the empirical work that describes actual growth experiences. We can now use the theory and evidence to help guide our thinking about economic policy.

Evaluating the Rate of Saving

According to the Solow growth model, how much a nation saves and invests is a key determinant of its citizens’ standard of living. So let’s begin our policy discussion with a natural question: Is the rate of saving in the U.S. economy too low, too high, or about right?

As we have seen, the saving rate determines the steady-state levels of capital and output. One particular saving rate produces the Golden Rule steady state, which maximizes consumption per worker and thus economic well-being. The Golden Rule provides the benchmark against which we can compare the U.S. economy.

To decide whether the U.S. economy is at, above, or below the Golden Rule steady state, we need to compare the marginal product of capital net of depreciation (MPK − δ) with the growth rate of total output (n + g). As we established in Section 9-1, at the Golden Rule steady state, MPK − δ = n + g. If the economy is operating with less capital than in the Golden Rule steady state, then diminishing marginal product tells us that MPK − δ > n + g. In this case, increasing the rate of saving will increase capital accumulation and economic growth and, eventually, lead to a steady state with higher consumption (although consumption will be lower for part of the transition to the new steady state). On the other hand, if the economy has more capital than in the Golden Rule steady state, then MPK − δ < n + g. In this case, capital accumulation is excessive: reducing the rate of saving will lead to higher consumption both immediately and in the long run.

252

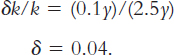

To make this comparison for a real economy, such as the U.S. economy, we need an estimate of the growth rate of output (n + g) and an estimate of the net marginal product of capital (MPK − δ). Real GDP in the United States grows an average of 3 percent per year, so n + g = 0.03. We can estimate the net marginal product of capital from the following three facts:

The capital stock is about 2.5 times one year’s GDP.

Depreciation of capital is about 10 percent of GDP.

Capital income is about 30 percent of GDP.

Using the notation of our model (and the result from Chapter 3 that capital owners earn income of MPK for each unit of capital), we can write these facts as

k = 2.5y.

δk = 0.1y.

MPK × k = 0.3y.

We solve for the rate of depreciation δ by dividing equation 2 by equation 1:

And we solve for the marginal product of capital MPK by dividing equation 3 by equation 1:

Thus, about 4 percent of the capital stock depreciates each year, and the marginal product of capital is about 12 percent per year. The net marginal product of capital, MPK − δ, is about 8 percent per year.

We can now see that the return to capital (MPK − δ = 8 percent per year) is well in excess of the economy’s average growth rate (n + g = 3 percent per year). This fact, together with our previous analysis, indicates that the capital stock in the U.S. economy is well below the Golden Rule level. In other words, if the United States saved and invested a higher fraction of its income, it would grow more rapidly and eventually reach a steady state with higher consumption.

This conclusion is not unique to the U.S. economy. When calculations similar to those above are done for other economies, the results are similar. The possibility of excessive saving and capital accumulation beyond the Golden Rule level is intriguing as a matter of theory, but it appears not to be a problem that actual economies face. In practice, economists are more often concerned with insufficient saving. It is this kind of calculation that provides the intellectual foundation for this concern.5

253

Changing the Rate of Saving

The preceding calculations show that to move the U.S. economy toward the Golden Rule steady state, policymakers should enact policies to encourage national saving. But how can they do that? We saw in Chapter 3 that, as a matter of simple accounting, higher national saving means higher public saving, higher private saving, or some combination of the two. Much of the debate over policies to increase growth centers on which of these options is likely to be most effective.

The most direct way in which the government affects national saving is through public saving—the difference between what the government receives in tax revenue and what it spends. When its spending exceeds its revenue, the government runs a budget deficit, which represents negative public saving. As we saw in Chapter 3, a budget deficit raises interest rates and crowds out investment; the resulting reduction in the capital stock is part of the burden of the national debt on future generations. Conversely, if it spends less than it raises in revenue, the government runs a budget surplus, which it can use to retire some of the national debt and stimulate investment.

The government also affects national saving by influencing private saving—the saving done by households and firms. In particular, how much people decide to save depends on the incentives they face, and these incentives are altered by a variety of public policies. Many economists argue that high tax rates on capital—including the corporate income tax, the federal income tax, the estate tax, and many state income and estate taxes—discourage private saving by reducing the rate of return that savers earn. On the other hand, tax-exempt retirement accounts, such as IRAs, are designed to encourage private saving by giving preferential treatment to income saved in these accounts. Some economists have proposed increasing the incentive to save by replacing the current system of income taxation with a system of consumption taxation.

Many disagreements over public policy are rooted in different views about how much private saving responds to incentives. For example, suppose that the government increased the amount that people can put into tax-exempt retirement accounts. Would people respond to this incentive by saving more? Or, instead, would people merely transfer saving already done in taxable savings accounts into these tax-advantaged accounts, reducing tax revenue and thus public saving without any stimulus to private saving? The desirability of the policy depends on the answers to these questions. Unfortunately, despite much research on this issue, no consensus has emerged.

Allocating the Economy’s Investment

The Solow model makes the simplifying assumption that there is only one type of capital. In the world, of course, there are many types. Private businesses invest in traditional types of capital, such as bulldozers and steel plants, and newer types of capital, such as computers and robots. The government invests in various forms of public capital, called infrastructure, such as roads, bridges, and sewer systems.

254

In addition, there is human capital—the knowledge and skills that workers acquire through education, from early-childhood programs such as Head Start to on-the-job training for adults in the labor force. Although the capital variable in the Solow model is usually interpreted as including only physical capital, in many ways human capital is analogous to physical capital. Like physical capital, human capital increases our ability to produce goods and services. Raising the level of human capital requires investment in the form of teachers, libraries, and student time. Research on economic growth has emphasized that human capital is at least as important as physical capital in explaining international differences in standards of living. One way of modeling this fact is to give the variable we call “capital” a broader definition that includes both human and physical capital.6

Policymakers trying to promote economic growth must confront the issue of what kinds of capital the economy needs most. In other words, what kinds of capital yield the highest marginal products? To a large extent, policymakers can rely on the marketplace to allocate the pool of saving to alternative types of investment. Those industries with the highest marginal products of capital will naturally be most willing to borrow at market interest rates to finance new investment. Many economists advocate that the government should merely create a “level playing field” for different types of capital—for example, by ensuring that the tax system treats all forms of capital equally. The government can then rely on the market to allocate capital efficiently.

Other economists have suggested that the government should actively encourage particular forms of capital. Suppose, for instance, that technological advance occurs as a by-product of certain economic activities. This would happen if new and improved production processes are devised during the process of building capital (a phenomenon called learning by doing) and if these ideas become part of society’s pool of knowledge. Such a by-product is called a technological externality (or a knowledge spillover). In the presence of such externalities, the social returns to capital exceed the private returns, and the benefits of increased capital accumulation to society are greater than the Solow model suggests.7 Moreover, some types of capital accumulation may yield greater externalities than others. If, for example, installing robots yields greater technological externalities than building a new steel mill, then perhaps the government should use the tax laws to encourage investment in robots. The success of such an industrial policy, as it is sometimes called, requires that the government be able to accurately measure the externalities of different economic activities so it can give the correct incentive to each activity.

255

Most economists are skeptical about industrial policies for two reasons. First, measuring the externalities from different sectors is virtually impossible. If policy is based on poor measurements, its effects might be close to random and, thus, worse than no policy at all. Second, the political process is far from perfect. Once the government gets into the business of rewarding specific industries with subsidies and tax breaks, the rewards are as likely to be based on political clout as on the magnitude of externalities.

One type of capital that necessarily involves the government is public capital. Local, state, and federal governments are always deciding if and when they should borrow to finance new roads, bridges, and transit systems. In 2009, one of President Barack Obama’s first economic proposals was to increase spending on such infrastructure. This policy was motivated by a desire partly to increase short-run aggregate demand (a goal we will examine later in this book) and partly to provide public capital and enhance long-run economic growth. Among economists, this policy had both defenders and critics. Yet all of them agree that measuring the marginal product of public capital is difficult. Private capital generates an easily measured rate of profit for the firm owning the capital, whereas the benefits of public capital are more diffuse. Furthermore, while private capital investment is made by investors spending their own money, the allocation of resources for public capital involves the political process and taxpayer funding. It is all too common to see “bridges to nowhere” being built simply because the local senator or congressman has the political muscle to get funds approved.

CASE STUDY

Industrial Policy in Practice

Policymakers and economists have long debated whether the government should promote certain industries and firms because they are strategically important for the economy. In the United States, the debate goes back over two centuries. Alexander Hamilton, the first U.S. Secretary of the Treasury, favored tariffs on certain imports to encourage the development of domestic manufacturing. The Tariff of 1789 was the second act passed by the new federal government. The tariff helped manufacturers, but it hurt farmers, who had to pay more for foreign-made products. Because the North was home to most of the manufacturers, while the South had more farmers, the tariff was one source of the regional tensions that eventually led to the Civil War.

Advocates of a significant government role in promoting technology can point to some recent successes. For example, the precursor of the modern Internet is a system called Arpanet, which was established by an arm of the U.S. Department of Defense as a way for information to flow among military installations. There is little doubt that the Internet has been associated with large advances in productivity and that the government had a hand in its creation. According to proponents of industrial policy, this example illustrates how the government can help jump-start an emerging technology.

256

Yet governments can also make mistakes when they try to supplant private business decisions. Japan’s Ministry of International Trade and Industry (MITI) is sometimes viewed as a successful practitioner of industrial policy, but it once tried to stop Honda from expanding its business from motorcycles to automobiles. MITI thought that the nation already had enough car manufacturers. Fortunately, the government lost this battle, and Honda turned into one of the world’s largest and most profitable car companies. Soichiro Honda, the company’s founder, once said, “Probably I would have been even more successful had we not had MITI.”

More recently, government policy has aimed to promote “green technologies.” In particular, the U.S. federal government has subsidized the production of energy in ways that yield lower carbon emissions, which are thought to contribute to global climate change. It is too early to judge the long-run success of this policy, but there have been some short-run embarrassments. In 2011, a manufacturer of solar panels called Solyndra declared bankruptcy just two years after the federal government granted it a $535 million loan guarantee.

The debate over industrial policy will surely continue in the years to come. The final judgment about this kind of government intervention in the market requires evaluating both the efficiency of unfettered markets and the ability of governmental institutions to identify technologies worthy of support.

Establishing the Right Institutions

As we discussed earlier, economists who study international differences in the standard of living attribute some of these differences to the inputs of physical and human capital and some to the productivity with which these inputs are used. One reason nations may have different levels of production efficiency is that they have different institutions guiding the allocation of scarce resources. Creating the right institutions is important for ensuring that resources are allocated to their best use.

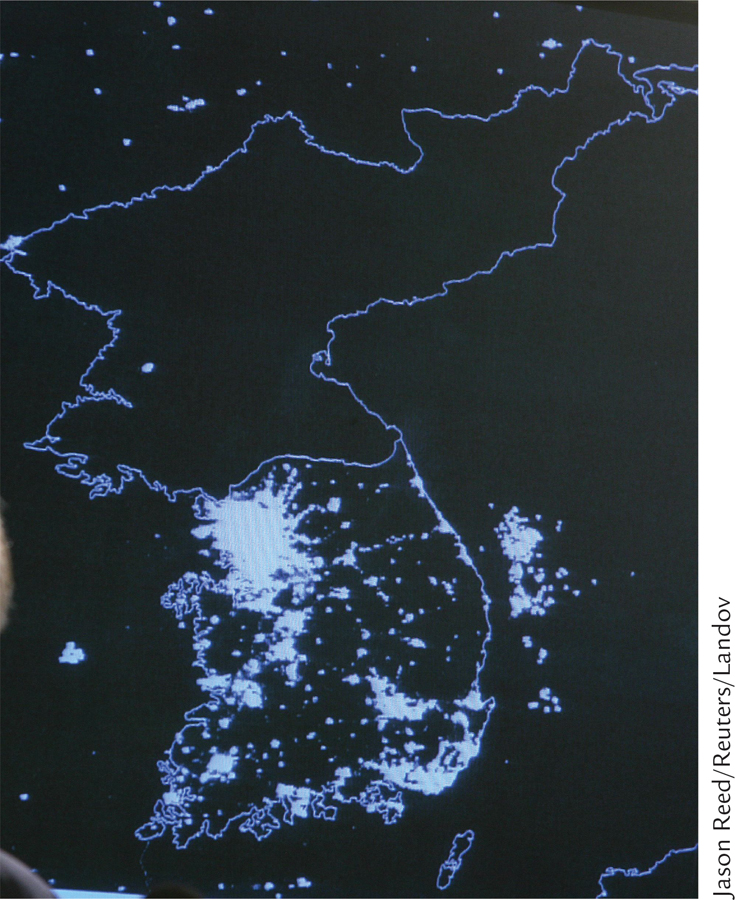

Perhaps the clearest current example of the importance of institutions is the comparison between North and South Korea. For many centuries, these two nations were combined with a common government, heritage, culture, and economy. Yet in the aftermath of World War II, an agreement between the United States and the Soviet Union split Korea in two. Above the thirty-eighth parallel, North Korea established institutions based on the Soviet model of authoritarian communism. Below the thirty-eighth parallel, South Korea established institutions based on the American model of democratic capitalism. Today, the difference in economic development could not be more stark. GDP per person in North Korea is less than one-tenth what it is in South Korea. This difference is visible in satellite photos taken at night. South Korea is well lit—its widespread use of electricity a sign of advanced economic development. North Korea, in contrast, is shrouded in darkness.

257

Among democratic capitalist nations, there are important but more subtle institutional differences. One example is a nation’s legal tradition. Some countries, such as the United States, Australia, India, and Singapore, are former colonies of the United Kingdom and, therefore, have English-style common-law systems. Other nations, such as Italy, Spain, and most of those in Latin America, have legal traditions that evolved from the French Napoleonic Code. Studies have found that legal protections for shareholders and creditors are stronger in English-style than French-style legal systems. As a result, the English-style countries have better-developed capital markets. Nations with better-developed capital markets, in turn, experience more rapid growth because it is easier for small and start-up companies to finance investment projects, leading to a more efficient allocation of the nation’s capital.8

Another important institutional difference across countries is the quality of government and honesty of government officials. Ideally, governments should provide a “helping hand” to the market system by protecting property rights, enforcing contracts, promoting competition, prosecuting fraud, and so on. Yet governments sometimes diverge from this ideal and act more like a “grabbing hand” by using the authority of the state to enrich a few powerful individuals at the expense of the broader community. Empirical studies have shown that the extent of corruption in a nation is indeed a significant determinant of economic growth.9

Adam Smith, the great eighteenth-century economist, was well aware of the role of institutions in economic growth. He once wrote, “Little else is requisite to carry a state to the highest degree of opulence from the lowest barbarism but peace, easy taxes, and a tolerable administration of justice: all the rest being brought about by the natural course of things.” Sadly, many nations do not enjoy these three simple advantages.

CASE STUDY

The Colonial Origins of Modern Institutions

International data show a remarkable correlation between latitude and economic prosperity: nations closer to the equator typically have lower levels of income per person than nations farther from the equator. This fact is true in both the northern and southern hemispheres.

What explains the correlation? Some economists have suggested that the tropical climates near the equator have a direct negative impact on productivity. In the heat of the tropics, agriculture is more difficult, and disease is more prevalent. This makes the production of goods and services more difficult.

258

Although the direct impact of geography is one reason tropical nations tend to be poor, it is not the whole story. Research by Daron Acemoglu, Simon Johnson, and James Robinson has suggested an indirect mechanism—the impact of geography on institutions. Here is their explanation, presented in several steps:

In the seventeenth, eighteenth, and nineteenth centuries, tropical climates presented European settlers with an increased risk of disease, especially malaria and yellow fever. As a result, when Europeans were colonizing much of the rest of the world, they avoided settling in tropical areas, such as most of Africa and Central America. The European settlers preferred areas with more moderate climates and better health conditions, such as the regions that are now the United States, Canada, and New Zealand.

In those areas where Europeans settled in large numbers, the settlers established European-style institutions that protected individual property rights and limited the power of government. By contrast, in tropical climates, the colonial powers often set up “extractive” institutions, including authoritarian governments, so they could take advantage of the area’s natural resources. These institutions enriched the colonizers, but they did little to foster economic growth.

Although the era of colonial rule is now long over, the early institutions that the European colonizers established are strongly correlated with the modern institutions in the former colonies. In tropical nations, where the colonial powers set up extractive institutions, there is typically less protection of property rights even today. When the colonizers left, the extractive institutions remained and were simply taken over by new ruling elites.

The quality of institutions is a key determinant of economic performance. Where property rights are well protected, people have more incentive to make the investments that lead to economic growth. Where property rights are less respected, as is typically the case in tropical nations, investment and growth tend to lag behind.

This research suggests that much of the international variation in living standards that we observe today is a result of the long reach of history.10

Encouraging Technological Progress

The Solow model shows that sustained growth in income per worker must come from technological progress. The Solow model, however, takes technological progress as exogenous; it does not explain it. Unfortunately, the determinants of technological progress are not well understood.

Despite this limited understanding, many public policies are designed to stimulate technological progress. Most of these policies encourage the private sector to devote resources to technological innovation. For example, the patent system gives a temporary monopoly to inventors of new products; the tax code offers tax breaks for firms engaging in research and development; and government agencies, such as the National Science Foundation, directly subsidize basic research in universities. In addition, as discussed above, proponents of industrial policy argue that the government should take a more active role in promoting specific industries that are key to rapid technological advance.

259

In recent years, the encouragement of technological progress has taken on an international dimension. Many of the companies that engage in research to advance technology are located in the United States and other developed nations. Developing nations such as China have an incentive to “free ride” on this research by not strictly enforcing intellectual property rights. That is, Chinese companies often use ideas developed abroad without compensating the patent holders. The United States has strenuously objected to this practice, and China has promised to step up enforcement. If intellectual property rights were better enforced around the world, firms would have more incentive to engage in research, and this would promote worldwide technological progress.

CASE STUDY

Is Free Trade Good for Economic Growth?

At least since Adam Smith, economists have advocated free trade as a policy that promotes national prosperity. Here is how Smith put the argument in his 1776 classic, The Wealth of Nations:

It is a maxim of every prudent master of a family, never to attempt to make at home what it will cost him more to make than to buy. The tailor does not attempt to make his own shoes, but buys them of the shoemaker. The shoemaker does not attempt to make his own clothes but employs a tailor….

What is prudence in the conduct of every private family can scarce be folly in that of a great kingdom. If a foreign country can supply us with a commodity cheaper than we ourselves can make it, better buy it of them with some part of the produce of our own industry employed in a way in which we have some advantage.

Today, economists make the case with greater rigor, relying on David Ricardo’s theory of comparative advantage as well as more modern theories of international trade. According to these theories, a nation open to trade can achieve greater production efficiency and a higher standard of living by specializing in those goods for which it has a comparative advantage.

A skeptic might point out that this is just a theory. What about the evidence? Do nations that permit free trade in fact enjoy greater prosperity? A large body of literature addresses precisely this question.

One approach is to look at international data to see if countries that are open to trade typically enjoy greater prosperity. The evidence shows that they do. Economists Andrew Warner and Jeffrey Sachs studied this question for the period from 1970 to 1989. They report that among developed nations, the open economies grew at 2.3 percent per year, while the closed economies grew at 0.7 percent per year. Among developing nations, the open economies grew at 4.5 percent per year, while the closed economies again grew at 0.7 percent per year. These findings are consistent with Smith’s view that trade enhances prosperity, but they are not conclusive. Correlation does not prove causation. Perhaps being closed to trade is correlated with various other restrictive government policies, and it is those other policies that retard growth.

260

A second approach is to look at what happens when closed economies remove their trade restrictions. Once again, Smith’s hypothesis fares well. Throughout history, when nations open themselves up to the world economy, the typical result is a subsequent increase in economic growth. This occurred in Japan in the 1850s, South Korea in the 1960s, and Vietnam in the 1990s. But once again, correlation does not prove causation. Trade liberalization is often accompanied by other reforms aimed to promote growth, and it is hard to disentangle the effects of trade from the effects of the other reforms.

A third approach to measuring the impact of trade on growth, proposed by economists Jeffrey Frankel and David Romer, is to look at the impact of geography. Some countries trade less simply because they are geographically disadvantaged. For example, New Zealand is disadvantaged compared to Belgium because it is farther from other populous countries. Similarly, landlocked countries are disadvantaged compared to countries with their own seaports. Because these geographical characteristics are correlated with trade, but arguably uncorrelated with other determinants of economic prosperity, they can be used to identify the causal impact of trade on income. (The statistical technique, which you may have studied in an econometrics course, is called instrumental variables.) After analyzing the data, Frankel and Romer conclude that “a rise of one percentage point in the ratio of trade to GDP increases income per person by at least one-half percentage point. Trade appears to raise income by spurring the accumulation of human and physical capital and by increasing output for given levels of capital.”

The overwhelming weight of the evidence from this body of research is that Adam Smith was right. Openness to international trade is good for economic growth.11