EXAMPLE 13.25 Fitting and Forecasting Amazon Sales

amazon

CASE 13.1 Example 13.19 (page 678) showed us that the trend-and-season model given in Example 13.18 (pages 675–676) fails to capture the autocorrelation effect between successive observations. One strategy is to add a lag variable to the trend-and-seasonal model. In other words, we need to consider a model for logged sales that combines all the effects:

log(yt)=β0+β1t+β2Q1+β3Q2+β4Q3+β5log(yt−1)+εt

From software, we find the estimated model to be

^log(yt)=1.67+0.0131t−0.6996Q1−0.55212Q2−0.4277Q3+0.8045log(yt−1)

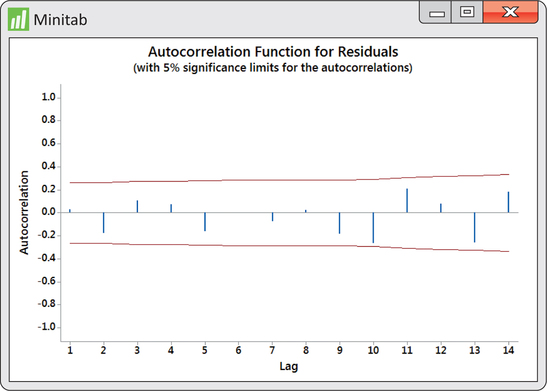

Figure 13.44 shows the ACF for the residuals from the above fit. Compare this ACF with the trend-and-seasonal residuals ACF of Figure 13.34 (page 678). We can see that the lag effects have been captured and thus result in a better fitting model. In terms of forecasting, the series ends with second-quarter 2014 sales of $19,340 (in millions). The ending quarter is the 58th period in the series, so our notation is y58=19,340.

First, use the model to forecast the logarithm of third-quarter 2014 sales:

^log(y59)=1.67+0.0131(59)−0.6996(0)−0.55212(0)−0.4277(1)+0.8045log(y58)=2.0152+0.8045log(19340)=2.0152+(0.8045)(9.86993)=9.95556

We can now untransform the log predicted value:

e9.95556=21069.04

Recall from the discussion of Example 13.18 (pages 675–676) that the preceding fitted value provides a prediction of median sales. If we want a prediction of mean sales, we need to obtain the regression standard error from our log fit. From the regression output for the fitting of logged sales, we find s=0.0410473. The predicted mean sales is then

^SALES59=21069.04es2/2=21069.04e0.04104732/2=21069.49(1.0008)=21085.90