7.2 The Benefits and Costs of Taxation

When a government is considering whether to impose a tax or how to design a tax system, it has to weigh the benefits of a tax against its costs. We don’t usually think of a tax as something that provides benefits, but governments need money to provide things people want, such as building roads and providing health care. The benefit of a tax is the revenue it raises for the government to pay for these services. Unfortunately, this benefit comes at a cost—

The Revenue from an Excise Tax

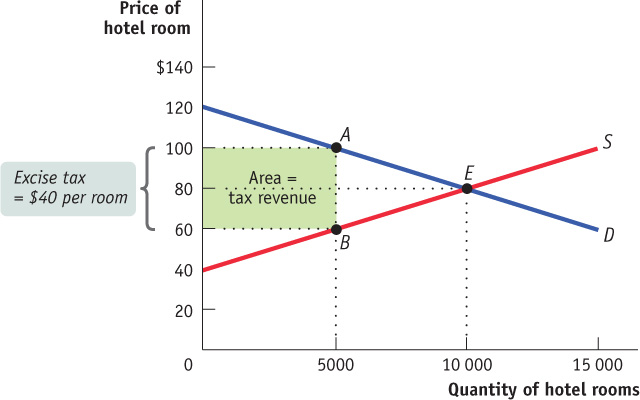

How much revenue does the government collect from an excise tax? In our hotel tax example, the revenue is equal to the area of the shaded rectangle in Figure 7-6.

To see why this area represents the revenue collected by a $40 tax on hotel rooms, notice that the height of the rectangle is $40, equal to the tax per room. It is also, as we’ve seen, the size of the wedge that the tax drives between the supply price (the price received by producers) and the demand price (the price paid by consumers). Meanwhile, the width of the rectangle is 5000 rooms, equal to the equilibrium quantity of rooms given the $40 tax. With that information, we can make the following calculations.

The tax revenue collected is:

Tax revenue = $40 per room × 5000 rooms = $200 000

The area of the shaded rectangle is:

Area = Height × Width = $40 per room × 5000 rooms = $200 000

or

Tax revenue = Area of shaded rectangle

This is a general principle: The revenue collected by an excise tax is equal to the area of the rectangle whose height is the tax wedge between the supply and demand curves and whose width is the quantity transacted under the tax.

Tax Rates and Revenue

A tax rate is the amount of tax people are required to pay per unit of whatever is being taxed.

In Figure 7-6, $40 per room is the tax rate on hotel rooms. A tax rate is the amount of tax levied per unit of whatever is being taxed. Sometimes tax rates are defined in terms of dollar amounts per unit of a good or service; for example, $6.75 per pack of cigarettes sold. In other cases, they are defined as a percentage of the price; for example, the payroll tax is 15.5% of a worker’s earnings up to $50 000.

There’s obviously a relationship between tax rates and revenue. That relationship is not, however, one-

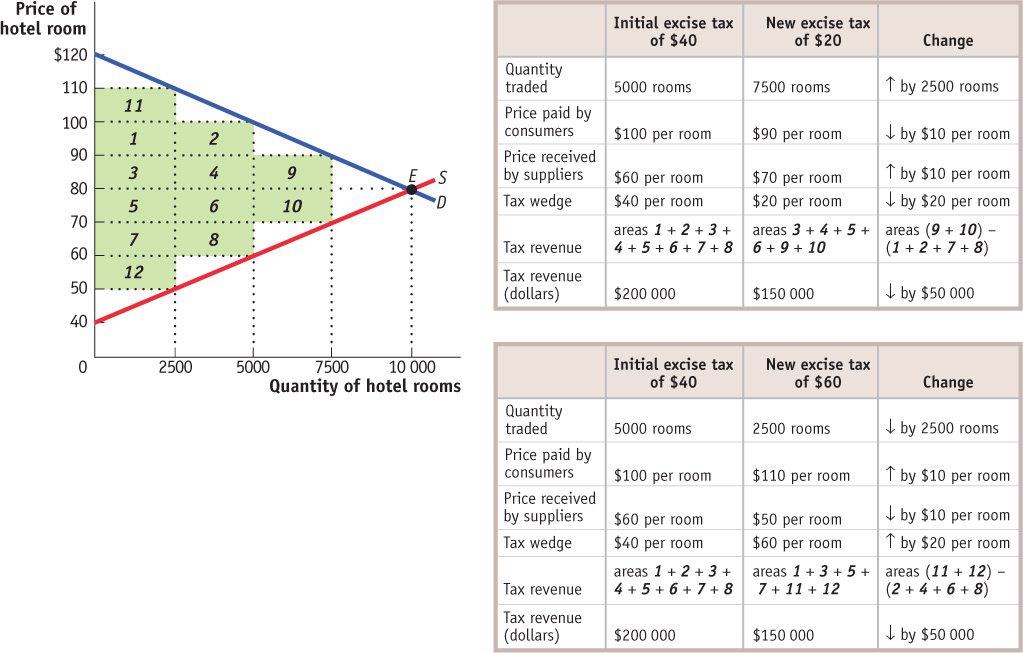

We can illustrate these points using our hotel room example. Figure 7-6 showed the revenue the government collects from a $40 tax on hotel rooms. Figure 7-7 shows the revenue the government would collect from two alternative tax rates—

Figure 7-7 shows the case of a $20 tax, equal to half the tax rate illustrated in Figure 7-6. At this lower tax rate, 7500 rooms are rented, generating tax revenue of:

Tax revenue = $20 per room × 7500 rooms = $150 000

Recall that the tax revenue collected from a $40 tax rate is $200 000. So the revenue collected from a $20 tax rate, $150 000, is only 75% of the amount collected when the tax rate is twice as high ($150 000/$200 000 × 100 = 75%). To put it another way, a 100% increase in the tax rate from $20 to $40 per room leads to only a one-

Figure 7-7 also depicts what happens if the tax rate is raised from $40 to $60 per room, leading to a fall in the number of rooms rented from 5000 to 2500. The revenue collected at a $60 per room tax rate is:

Tax revenue = $60 per room × 2500 rooms = $150 000

This is also less than the revenue collected by a $40 per room tax. So raising the tax rate from $40 to $60 actually reduces revenue. More precisely, in this case raising the tax rate by 50% (($60 − $40)/$40 × 100 = 50%) lowers the tax revenue by 25% (($150 000 − $200 000)/$200 000 × 100 = −25%). Why did this happen? It happened because the fall in tax revenue caused by the reduction in the number of rooms rented more than offset the increase in the tax revenue caused by the rise in the tax rate. In other words, setting a tax rate so high that it deters a significant number of transactions is likely to lead to a fall in tax revenue.

One way to think about the revenue effect of increasing an excise tax is that the tax increase affects tax revenue in two ways. On one side, the tax increase means that the government raises more revenue for each unit of the good sold, which other things equal would lead to a rise in tax revenue. On the other side, the tax increase reduces the quantity of sales, which other things equal would lead to a fall in tax revenue. The end result depends both on the price elasticities of supply and demand and on the initial level of the tax. If the price elasticities of both supply and demand are low, the tax increase won’t reduce the quantity of the good sold very much, so tax revenue will definitely rise. If the price elasticities are high, the result is less certain; if they are high enough, the tax reduces the quantity sold so much that tax revenue falls. Also, if the initial tax rate is low, the government doesn’t lose much revenue from the decline in the quantity of the good sold, so the tax increase will definitely increase tax revenue. If the initial tax rate is high, the result is again less certain. Tax revenue is likely to fall or rise very little from a tax increase only in cases where the price elasticities are high and there is already a high tax rate.

The possibility that a higher tax rate can reduce tax revenue, and the corresponding possibility that cutting taxes can increase tax revenue, is a basic principle of taxation that policy-

THE LAFFER CURVE

One afternoon in 1974, the economist Arthur Laffer got together in a cocktail lounge with Jude Wanniski, a writer for the Wall Street Journal, and Dick Cheney, who would later become vice president of the United States but at the time was the deputy White House chief of staff. During the course of their conversation, Laffer drew a diagram on a napkin that was intended to explain how tax cuts could sometimes lead to higher tax revenue. According to Laffer’s diagram, raising tax rates initially increases tax revenue, but beyond a certain level revenue falls instead as tax rates continue to rise. That is, at some point tax rates are so high and reduce the number of transactions so greatly that tax revenues fall.

There was nothing new about this idea, but in later years that napkin became the stuff of legend. The editors of the Wall Street Journal began promoting the “Laffer curve” as a justification for tax cuts. And when Ronald Reagan became president of the United States in 1981, he used the Laffer curve to argue that his proposed cuts in income tax rates would not reduce the federal government’s revenue.

So is there a Laffer curve? Yes—

The Costs of Taxation

What is the cost of a tax? You might be inclined to answer that it is the money taxpayers pay to the government. In other words, you might believe that the cost of a tax is the tax revenue collected. But suppose the government uses the tax revenue to provide services that taxpayers want. Or suppose that the government simply hands the tax revenue back to taxpayers. Would we say in those cases that the tax didn’t actually cost anything?

No—

So an excise tax imposes costs over and above the tax revenue collected in the form of inefficiency, which occurs because the tax discourages mutually beneficial transactions. As we learned in Chapter 5, the cost to society of this kind of inefficiency—

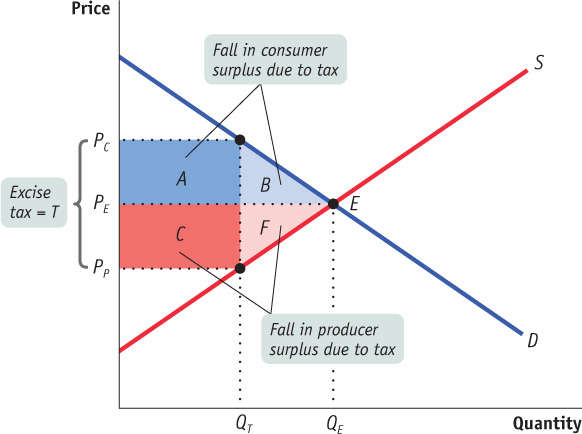

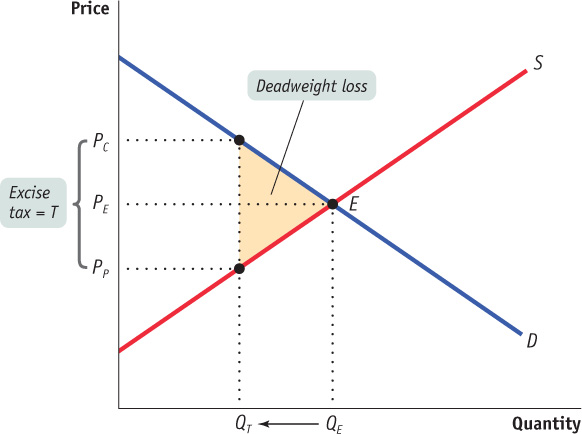

To measure the deadweight loss from a tax, we turn to the concepts of producer and consumer surplus. Figure 7-8 shows the effects of an excise tax on consumer and producer surplus. In the absence of the tax, the equilibrium is at E and the equilibrium price and quantity are PE and QE, respectively. An excise tax drives a wedge equal to the amount of the tax between the price received by producers and the price paid by consumers, reducing the quantity sold. In this case, where the tax is T dollars per unit, the quantity sold falls to QT. The price paid by consumers rises to PC, the demand price of the reduced quantity, QT, and the price received by producers falls to PP, the supply price of that quantity. The difference between these prices, PC − PP, is equal to the excise tax, T.

Using the concepts of producer and consumer surplus, we can show exactly how much surplus producers and consumers lose as a result of the tax. From Figure 4-5 we learned that, other things equal, a fall in the price of a good generates a gain in consumer surplus that is equal to the sum of the areas of a rectangle and a triangle. Similarly, other things equal, a price increase causes a loss to consumers that is represented by the sum of the areas of a rectangle and a triangle. So it’s not surprising that in the case of an excise tax, the rise in the price paid by consumers causes a loss equal to the sum of the areas of a rectangle and a triangle: the area of the dark blue rectangle labelled A and the area of the light blue triangle labelled B in Figure 7-8.

Meanwhile, the fall in the price received by producers leads to a fall in producer surplus. This, too, is equal to the sum of the areas of a rectangle and a triangle. The loss in producer surplus is the sum of the areas of the dark red rectangle labelled C and the light red triangle labelled F in Figure 7-8.

Of course, although consumers and producers are hurt by the tax, the government gains revenue. The revenue the government collects is equal to the tax per unit sold, T, multiplied by the quantity sold, QT. This revenue is equal to the area of a rectangle QT wide and T high. And we already have that rectangle in the figure: it is the sum of rectangles A and C. So the government gains part of what consumers and producers lose from an excise tax.

But a portion of the loss to producers and consumers from the tax is not offset by a gain to the government—

Figure 7-9 is a version of Figure 7-8 that leaves out rectangles A (the surplus shifted from consumers to the government) and C (the surplus shifted from producers to the government) and shows only the deadweight loss, drawn here as a shaded triangle. The base of that triangle is equal to the tax wedge, T; the height of the triangle is equal to the reduction in the quantity transacted due to the tax, QE − QT. Clearly, the larger the tax wedge and the larger the reduction in the quantity transacted, the greater the inefficiency from the tax. But also note an important, contrasting point: if the excise tax somehow didn’t reduce the quantity bought and sold in this market—

Using a triangle to measure deadweight loss is a technique used in many economic applications. For example, triangles are used to measure the deadweight loss produced by types of taxes other than excise taxes. They are also used to measure the deadweight loss produced by monopoly, another kind of market distortion. And deadweight-

The administrative costs of a tax are the resources used by government to collect the tax, and by taxpayers to pay it, over and above the amount of the tax, as well as to evade it.

In considering the total amount of inefficiency caused by a tax, we must also take into account something not shown in Figure 7-9: the resources actually used by the government to collect the tax, and by taxpayers to pay it, over and above the amount of the tax. These lost resources are called the administrative costs of the tax. The most familiar administrative cost of the Canadian tax system is the time individuals spend filling out their income tax forms or the money they spend on accountants to prepare their tax forms for them. (The latter is considered an inefficiency from the point of view of society because accountants could instead be performing other, non-

So the total inefficiency caused by a tax is the sum of its deadweight loss and its administrative costs. The general rule for economic policy is that, other things equal, a tax system should be designed to minimize the total inefficiency it imposes on society. In practice, other considerations also apply (as the federal government learned in 1990), but this principle nonetheless gives valuable guidance. Administrative costs are usually well known, and are more or less determined by the current technology of collecting taxes (for example, filing paper returns versus filing electronically). But how can we predict the size of the deadweight loss associated with a given tax? Not surprisingly, as in our analysis of the incidence of a tax, the price elasticities of supply and demand play crucial roles in making such a prediction.

Elasticities and the Deadweight Loss of a Tax

We know that the deadweight loss from an excise tax arises because it prevents some mutually beneficial transactions from occurring. In particular, the producer and consumer surplus that is forgone because of these missing transactions is equal to the size of the deadweight loss itself. This means that the larger the number of transactions that are prevented by the tax, the larger the deadweight loss.

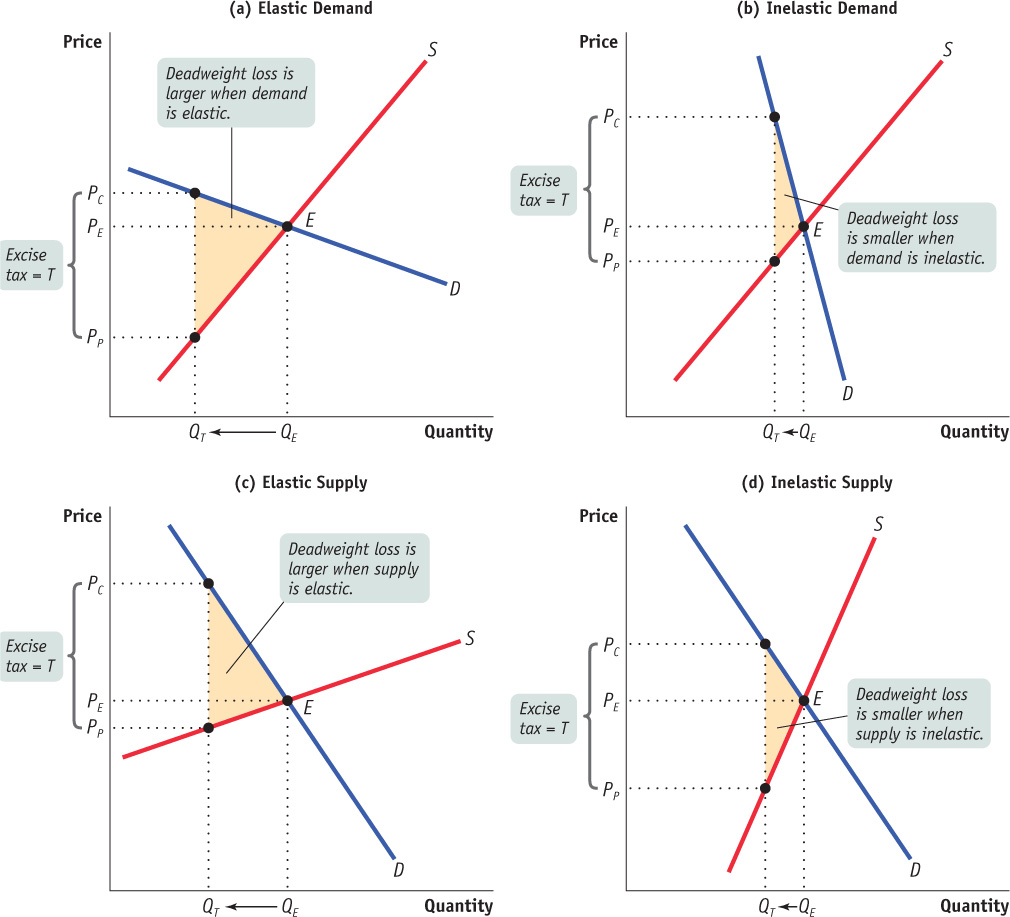

This fact gives us an important clue in understanding the relationship between elasticity and the size of the deadweight loss from a tax. Recall that when demand or supply is elastic, the quantity demanded or the quantity supplied is relatively responsive to changes in the price. So a tax imposed on a good for which either demand or supply, or both, is elastic will cause a relatively large decrease in the quantity transacted and a relatively large deadweight loss. And when we say that demand or supply is inelastic, we mean that the quantity demanded or the quantity supplied is relatively unresponsive to changes in the price. As a result, a tax imposed when demand or supply, or both, is inelastic will cause a relatively small decrease in the quantity transacted and a relatively small deadweight loss.

The four panels of Figure 7-10 illustrate the positive relationship between a good’s price elasticity of either demand or supply and the deadweight loss from taxing that good. Each panel represents the same amount of tax imposed but on a different good; the size of the deadweight loss is given by the area of the shaded triangle. In panel (a), the deadweight-loss triangle is large because demand for this good is relatively elastic—a large number of transactions fail to occur because of the tax. In panel (b), the same supply curve is drawn as in panel (a), but demand for this good is relatively inelastic; as a result, the triangle is small because only a small number of transactions are forgone. Likewise, panels (c) and (d) contain the same demand curve but different supply curves. In panel (c), an elastic supply curve gives rise to a large deadweight-loss triangle, but in panel (d) an inelastic supply curve gives rise to a small deadweight-loss triangle.

The implication of this result is clear: if you want to minimize the efficiency costs of taxation, you should choose to tax only those goods for which demand or supply, or both, is relatively inelastic. For such goods, a tax has little effect on behaviour because behaviour is relatively unresponsive to changes in the price. In the extreme case in which demand is perfectly inelastic (a vertical demand curve), the quantity demanded is unchanged by the imposition of the tax. As a result, the tax imposes no deadweight loss. Similarly, if supply is perfectly inelastic (a vertical supply curve), the quantity supplied is unchanged by the tax and there is also no deadweight loss. So if the goal in choosing whom to tax is to minimize deadweight loss, then taxes should be imposed on goods and services that have the most inelastic response—that is, goods and services for which consumers or producers will change their behaviour the least in response to the tax. (Unless they have a tendency to revolt, of course.) And this lesson carries a flip side: using a tax to purposely decrease the amount of a harmful activity, such as underage drinking, will have the most impact when that activity is elastically demanded or supplied.

TAXING SMOKES

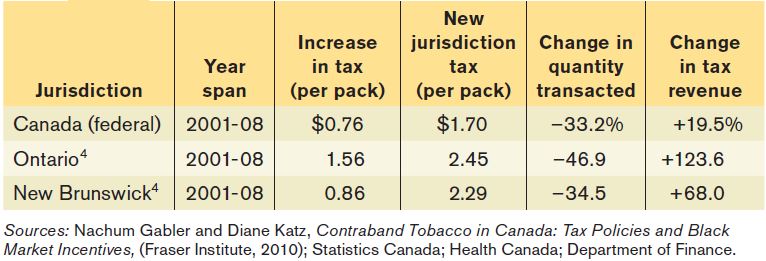

One of the most important excise taxes in Canada is the tax on cigarettes. The federal government imposes a tax of $1.70 a pack; provincial and territorial governments impose taxes that range from $2.47 a pack in Ontario to $5.80 a pack in Manitoba; and throughout the country the GST/HST applies on top of these excise taxes (in Manitoba and Saskatchewan, the PST also applies on top of the excise tax). The combined tax on a pack of cigarettes varies from $4.65 per pack in Quebec to $8.79 a pack in Manitoba. In general, tax rates on cigarettes have increased over time, because more and more governments have seen them not just as a source of revenue but as a way to discourage smoking. But the rise in cigarette taxes has not been gradual. Once a government decides to raise cigarette taxes, it usually raises them a lot—which provides economists with useful data on what happens when there is a big tax increase.

The time span for the data was chosen to reflect the significant tax increases that followed the 2001 introduction of the Federal Tobacco Control Strategy that, among other things, sought to protect Canadians from the harms of tobacco consumption via higher federal taxes. The federal government raised the excise tax per pack of cigarettes from $0.94 in 2000 to $1.70 by 2008—an 80.7% increase. Many of the provinces followed the federal lead. The largest provincial increase occurred in Ontario, where the excise tax per pack rose from $0.89 in 2000 to $2.45 by 2008—a 175.1% increase. The smallest provincial increase was in New Brunswick, where the excise tax per pack rose from $1.43 in 2000 to $2.29 by 2008—a 59.7% increase.

Table 7-1 shows the results of big increases in cigarette taxes. In each case, sales fell, just as our analysis predicts. Although it’s theoretically possible for tax revenue to fall after such a large tax increase, in reality, tax revenue rose in each case. That’s because cigarettes have a low price elasticity of demand.

Quick Review

An excise tax generates tax revenue equal to the tax rate times the number of units of the good or service transacted but reduces consumer and producer surplus.

The government tax revenue collected is less than the loss in total surplus because the tax creates inefficiency by discouraging some mutually beneficial transactions.

The difference between the tax revenue from an excise tax and the reduction in total surplus is the deadweight loss from the tax. The total amount of inefficiency resulting from a tax is equal to the deadweight loss plus the administrative costs of the tax.

The larger the number of trans-actions prevented by a tax, the larger the deadweight loss. As a result, taxes on goods with a greater price elasticity of supply or demand, or both, generate higher deadweight losses. There is no deadweight loss when the number of transactions is unchanged by the tax.

Check Your Understanding 7-2

CHECK YOUR UNDERSTANDING 7-2

Question 7.6

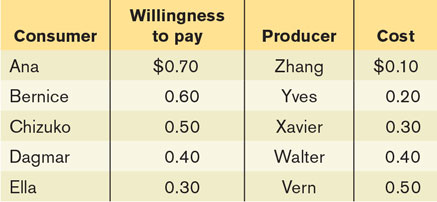

The accompanying table shows five consumers’ willingness to pay for one can of diet cola each as well as five producers’ costs of selling one can of diet cola each. Each consumer buys at most one can of cola; each producer sells at most one can of cola. The government asks your advice about the effects of an excise tax of $0.40 per can of diet cola. Assume that there are no administrative costs from the tax.

Without the excise tax, what is the equilibrium price and the equilibrium quantity of cola transacted?

The excise tax raises the price paid by consumers post-tax to $0.60 and lowers the price received by producers post-tax to $0.20. With the excise tax, what is the quantity of cola transacted?

Without the excise tax, how much individual consumer surplus does each of the consumers gain? How much with the tax? How much total consumer surplus is lost as a result of the tax?

Without the excise tax, how much individual producer surplus does each of the producers gain? How much with the tax? How much total producer surplus is lost as a result of the tax?

How much government revenue does the excise tax create?

What is the deadweight loss from the imposition of this excise tax?

Without the excise tax, Zhang, Yves, Xavier, and Walter sell, and Ana, Bernice, Chizuko, and Dagmar buy one can of cola each, at $0.40 per can. So the quantity bought and sold is 4.

With the excise tax, Zhang and Yves sell, and Ana and Bernice buy one can of cola each. So the quantity bought and sold is 2.

Without the excise tax, Ana’s individual consumer surplus is $0.70 − $0.40 = $0.30, Bernice’s is $0.60 − $0.40 = $0.20, Chizuko’s is $0.50 − $0.40 = $0.10, and Dagmar’s is $0.40 − $0.40 = $0.00. Total consumer surplus is $0.30 + $0.20 + $0.10 + $0.00 = $0.60. With the tax, Ana’s individual consumer surplus is $0.70 − $0.60 = $0.10 and Bernice’s is $0.60 − $0.60 = $0.00. Total consumer surplus post-tax is $0.10 + $0.00 = $0.10. So the total consumer surplus lost because of the tax is $0.60 − $0.10 = $0.50.

Without the excise tax, Zhang’s individual producer surplus is $0.40 − $0.10 = $0.30, Yves’s is $0.40 − $0.20 = $0.20, Xavier’s is $0.40 − $0.30 = $0.10, and Walter’s is $0.40 − $0.40 = $0.00. Total producer surplus is $0.30 + $0.20 + $0.10 + $0.00 = $0.60. With the tax, Zhang’s individual producer surplus is $0.20 − $0.10 = $0.10 and Yves’s is $0.20 − $0.20 = $0.00. Total producer surplus post-tax is $0.10 + $0.00 = $0.10. So the total producer surplus lost because of the tax is $0.60 − $0.10 = $0.50.

With the tax, two cans of cola are sold, so the government tax revenue from this excise tax is 2 × $0.40 = $0.80.

Total surplus without the tax is $0.60 + $0.60 = $1.20. With the tax, total surplus is $0.10 + $0.10 = $0.20, and government tax revenue is $0.80. So deadweight loss from this excise tax is $1.20 − ($0.20 + $0.80) = $0.20.

Question 7.7

In each of the following cases, focus on the price elasticity of demand and use a diagram to illustrate the likely size—small or large—of the deadweight loss resulting from a tax. Explain your reasoning.

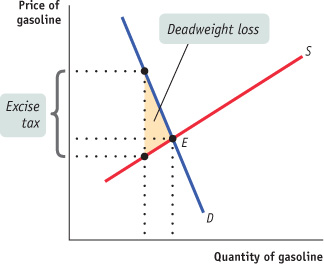

Gasoline

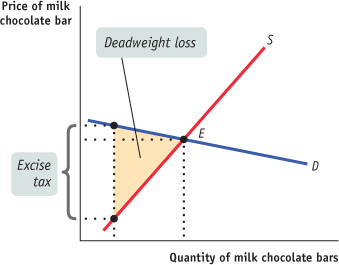

Milk chocolate bars

The demand for gasoline is inelastic because there is no close substitute for gasoline itself and it is difficult for drivers to arrange substitutes for driving, such as taking public transportation. As a result, the deadweight loss from a tax on gasoline would be relatively small, as shown in the accompanying diagram.

The demand for milk chocolate bars is elastic because there are close substitutes: dark chocolate bars, milk chocolate kisses, and so on. As a result, the deadweight loss from a tax on milk chocolate bars would be relatively large, as shown in the accompanying diagram.