Chapter Introduction

313

314

After studying this chapter you should be able to:

- Explain the goals of monetary policy and how the Fed uses expansionary and contractionary policies to achieve them.

- Describe how monetary policy affects interest rates and aggregate demand, and subsequently prices and output.

- Describe the equation of exchange and its implications for monetary policy in the long run.

- Contrast classical long-run monetary theory concerning the effectiveness of monetary policy in the short run with the explanations of the Keynesians and monetarists.

- Describe why the Fed targets price stability in the long run and inflation rates and output in the short run.

- Determine the effectiveness of monetary policy when demand or supply shocks occur.

- Describe the controversy over whether the Fed should have discretion or be governed by simple monetary rules.

- Describe the federal funds target, the Taylor rule, and how they are used in modern monetary policymaking.

- Explain why some policymakers have questioned the role of the Fed after it used extraordinary powers in response to the financial crisis of 2008.

- Discuss the monetary policy challenges faced by the Fed and the European Central Bank following the last recession and the Eurozone crisis.

Information received since the Federal Open Market Committee met in January suggests a return to moderate economic growth following a pause late last year. Labor market conditions have shown signs of improvement in recent months but the unemployment rate remains elevated…. To support continued progress towards maximum employment and price stability, the Committee expects that a highly accommodative stance of monetary policy will remain appropriate for a considerable time….

—Excerpt from the FOMC Statement of March 20, 2013

At 2:00 p.m. on an ordinary weekday afternoon, the Federal Reserve (Fed) concludes its meeting of the Federal Open Market Committee, and just 15 minutes later, at 2:15 p.m. a meeting statement is released. To the twelve voting members of this committee, which meets about every six weeks, it’s just another day on the job. But this is not your ordinary everyday job.

On Wall Street, millions of investors, physically present at a stock exchange or virtually present via their online brokerage accounts, anxiously await this Fed statement. Corporate executives, just coming back from lunch, immediately search their news app for the latest statement release.

Government policymakers in Ecuador and El Salvador tune in to the news to hear the Fed statement because it affects their countries’ interest rates and their currency, which in fact is the U.S. dollar. And markets in the rest of the world await the Fed statement to determine how their own economies will be affected.

Indeed, in a matter of minutes after the release of the Fed statement, the twelve members of the Federal Open Market Committee will have affected the lives of hundreds of millions of people. How do such ordinary people carry such tremendous power?

The Federal Open Market Committee is the body within the Federal Reserve that controls U.S. monetary policy. Their economic policy decisions affect not only the U.S. economy but the entire world economy.

Although not every Fed meeting statement produces a dramatic flurry of reactions, the ability of the Fed to exert powerful policy action in times of economic fluctuation makes its meeting statement the most dissected piece of economic news in the world. Even the most slightly nuanced wording of the statement can generate mass market activity as people attempt to predict how the Fed will act not only today, but in months and years ahead.

This chapter studies the remarkable influence the Fed has to alter the macroeconomy using the tools that form the basis of monetary policy. The Federal Reserve Act mandates that the Fed implement monetary policies that will promote economic growth accompanied by high employment, stable prices, and moderate long-term interest rates. In the previous chapter, we saw how the Federal Reserve System is organized and described the three monetary policy tools the Fed uses, which are setting reserve requirements, setting the discount rate, and conducting open market operations. In this chapter, we look at what monetary policy aims to achieve and how the Fed undertakes monetary policy to deal with economic fluctuations.

315

Monetary Policy In Action

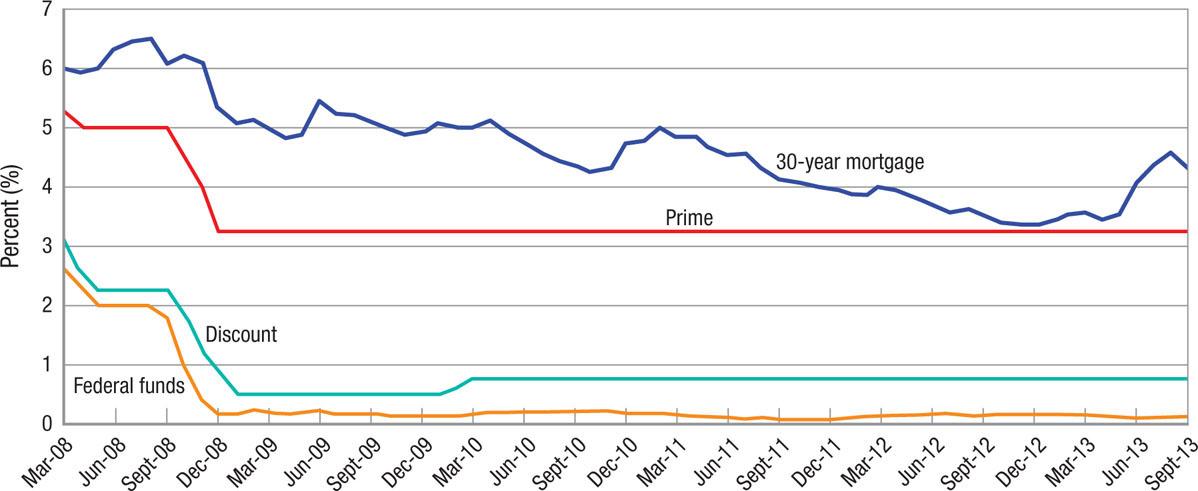

Among the tools used by the Federal Reserve to conduct monetary policy are setting the discount rate and conducting open market operations targeting the federal funds rate. The interest rates targeted by the Fed have a profound impact on the entire economy.

The Fed’s decisions on the discount and federal funds rate influence other interest rates of concern to consumers and firms. Notice how the average 30-year mortgage rate and the prime rate track the Fed’s discount and federal funds rate.

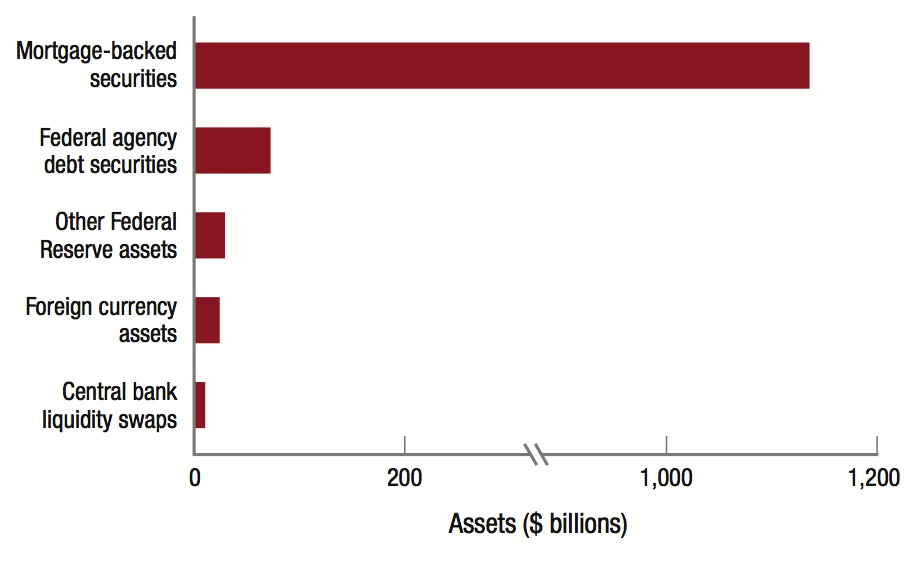

With the federal funds rate near 0%, the Fed used other mechanisms to provide relief to the economy, especially the purchase of mortgage-backed assets from banks and other financial institutions. As of April 2013, the Fed held over $1.2 trillion in nontreasury assets, of which mortgage-backed securities represented almost 90% of this amount.

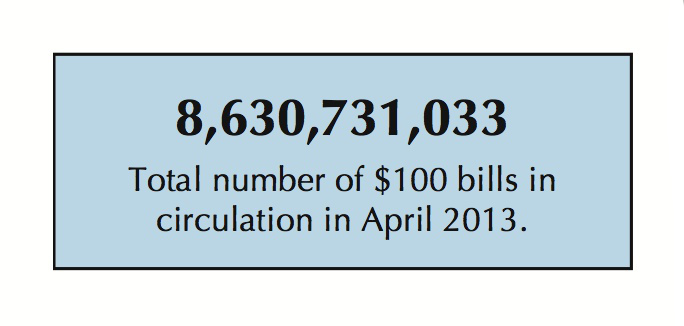

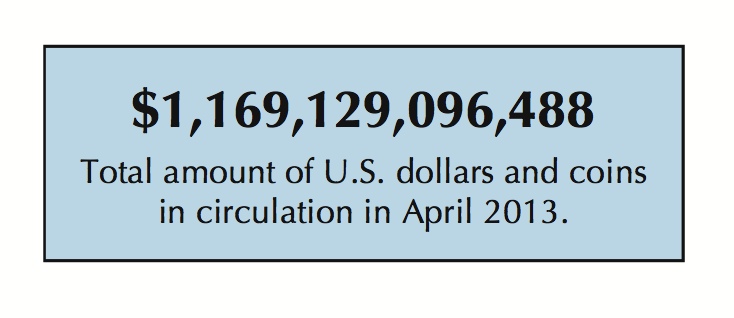

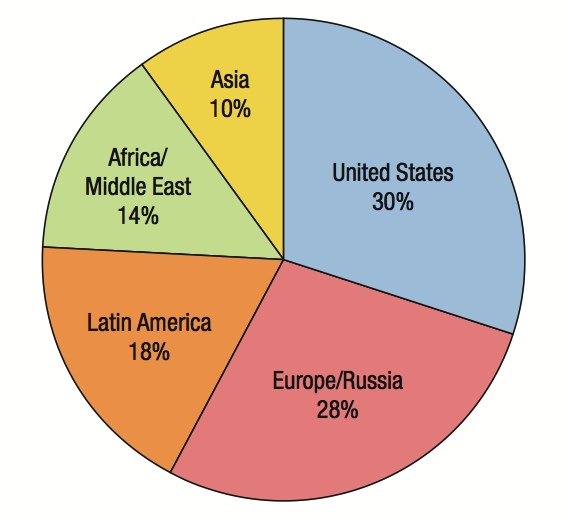

As the Fed increased the money supply, other countries have increased their holdings of U.S. dollars, mainly as reserves. Part of this is held in actual banknotes, mostly $100 bills. Where are all these $100 bills?

As the Fed increased the money supply, other countries have increased their holdings of U.S. dollars, mainly as reserves. Part of this is held in actual banknotes, mostly $100 bills. Where are all these $100 bills?

316

The first part of this chapter describes the monetary policy process. We show how expansionary monetary policy is utilized during economic downturns and contractionary monetary policy during economic booms. We then consider the question: How do changes in the money supply affect the economy? We will see that money has no effect on the economy’s real growth in the long run but can have sizeable effects in the short run. We examine the impact of monetary policy on controlling demand and supply shocks and how the Fed actually tries to manage the economy. We will see that the Fed’s control over the economy is indirect and that good monetary policymaking is both art and science.

This chapter goes on to examine modern monetary policy in the context of financial crises and political wrangling. What can the Fed do to deal with problems in the financial system? And how have the Fed’s aggressive actions during the recent financial crisis changed the perceptions of policymakers and the public about the role of government? The chapter concludes by looking at monetary policy challenges faced by the Fed and the European Central Bank, both of which have recently dealt with financial crises not seen in generations.