The Business Cycle

The Great Depression was by far the worst economic crisis in U.S. history. But although the economy managed to avoid catastrophe for the rest of the twentieth century, it has experienced many ups and downs.

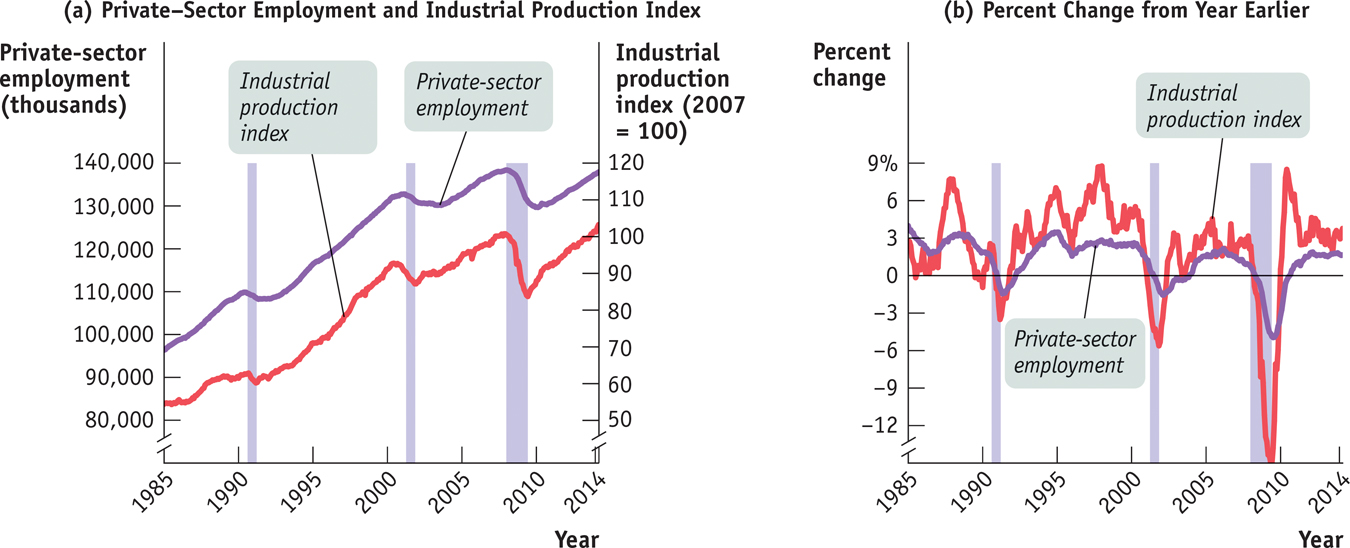

It’s true that the ups have consistently been bigger than the downs: a chart of any of the major numbers used to track the U.S. economy shows a strong upward trend over time. For example, panel (a) of Figure 21-2 shows total U.S. private-

But they didn’t rise steadily. As you can see from the figure, there were three periods—

The economy’s forward march, in other words, isn’t smooth. And the uneven pace of the economy’s progress, its ups and downs, is one of the main preoccupations of macroeconomics.

Charting the Business Cycle

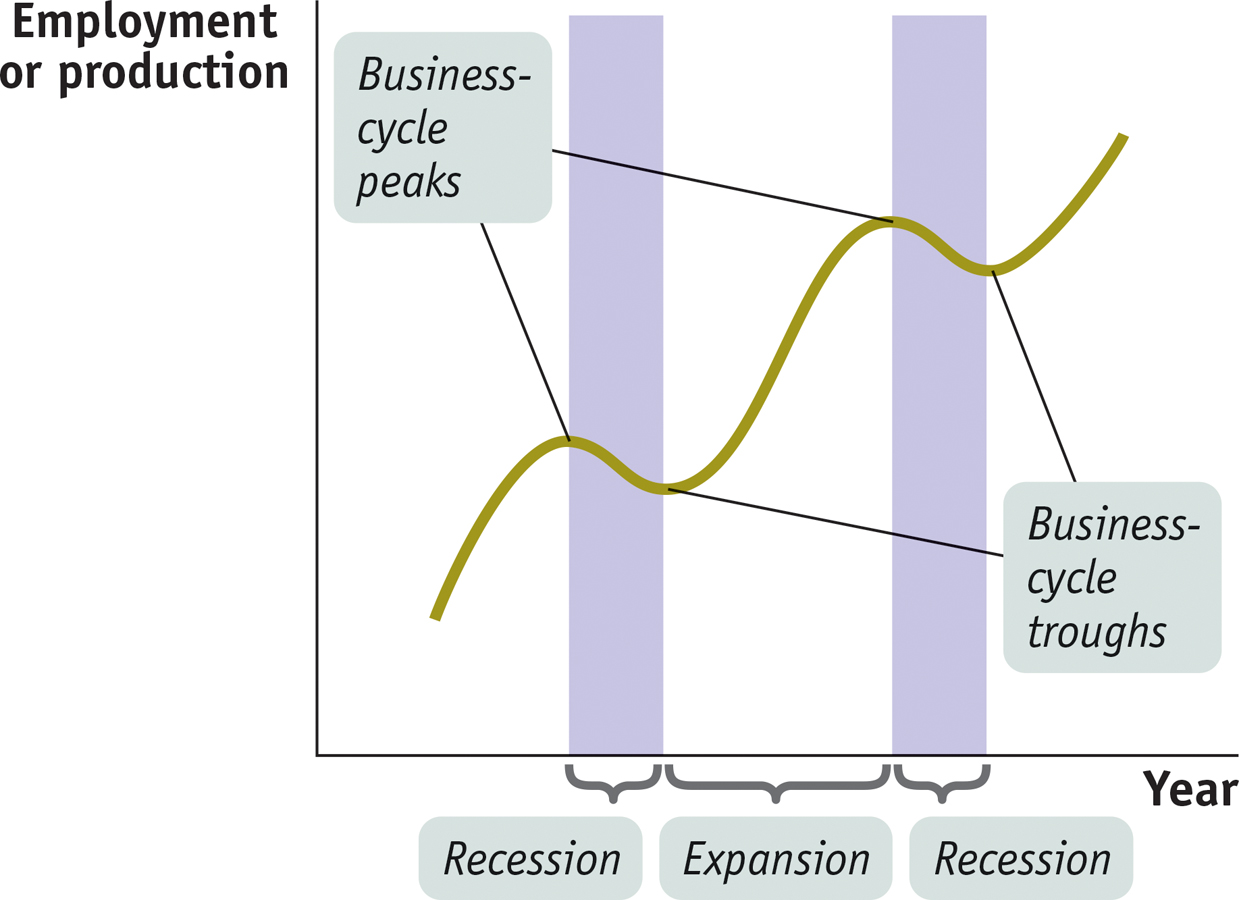

Figure 21-3 shows a stylized representation of the way the economy evolves over time. The vertical axis shows either employment or an indicator of how much the economy is producing, such as industrial production or real gross domestic product (real GDP), a measure of the economy’s overall output that we’ll learn about in the next chapter. As the data in Figure 21-2 suggest, these two measures tend to move together. Their common movement is the starting point for a major theme of macroeconomics: the economy’s alternation between short-

Recessions, or contractions, are periods of economic downturn when output and employment are falling.

Expansions, or recoveries, are periods of economic upturn when output and employment are rising.

The business cycle is the short-

The point at which the economy turns from expansion to recession is a business-

The point at which the economy turns from recession to expansion is a business-

A broad-

|

Business- |

Business- |

|---|---|

|

no prior data available June 185 7October 1860 April 1865 June 1869 October 1873 |

December 1854 December 1858 June 1861 December 1867 December 1870 March 1879 |

|

March 1882 March 1887 July 1890 January 1893 December 1895 |

May 1885 April 1888 May 1891 June 1894 June 1897 |

|

June 1899 September 1902 May 1907 January 1910 January 1913 |

December 1900 August 1904 June 1908 January 1912 December 1914 |

|

August 1918 January 1920 May 1923 October 1926 August 1929 |

March 1919 July 1921 July 1924 November 1927 March 1933 |

|

May 1937 February 1945 November 1948 July 1953 August 1957 |

June 1938 October 1945 October 1949 May 1954 April 1958 |

|

April 1960 December 1969 November 1973 January 1980 July 1981 |

February 1961 November 1970 March 1975 July 1980 November 1982 |

|

July 1990 March 2001 December 2007 |

March 1991 November 2001 June 2009 |

|

Source: National Bureau of Economic Research. |

|

TABLE 6-

The alternation between recessions and expansions is known as the business cycle. The point in time at which the economy shifts from expansion to recession is known as a business-

The business cycle is an enduring feature of the economy. Table 21-2 shows the official list of business-

The Pain of Recession

Not many people complain about the business cycle when the economy is expanding. Recessions, however, create a great deal of pain.

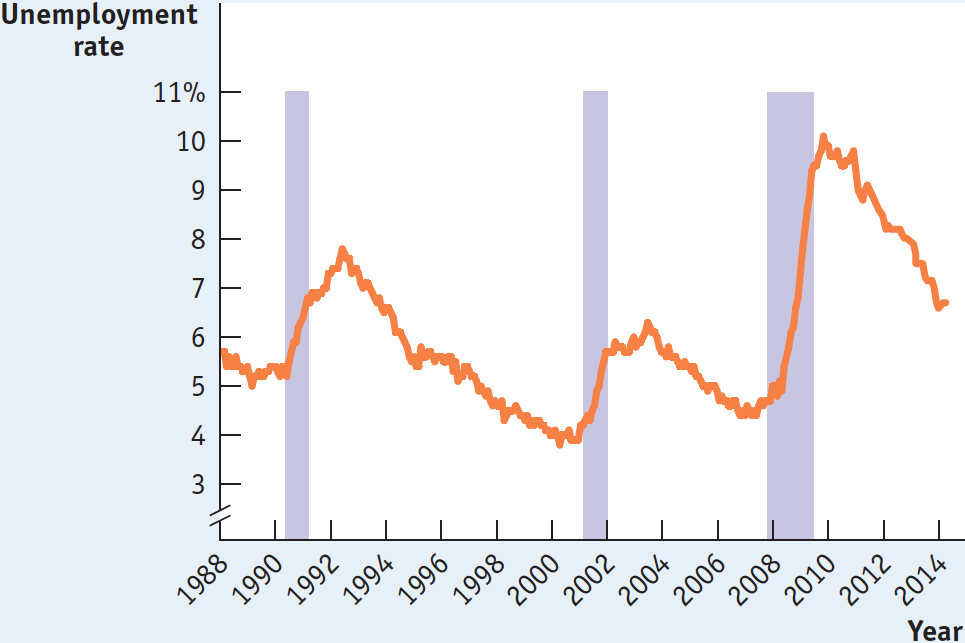

The most important effect of a recession is its effect on the ability of workers to find and hold jobs. The most widely used indicator of conditions in the labor market is the unemployment rate. We’ll explain how that rate is calculated in Chapter 23, but for now it’s enough to say that a high unemployment rate tells us that jobs are scarce and a low unemployment rate tells us that jobs are easy to find.

Figure 21-4 shows the unemployment rate from 1988 to 2014. As you can see, the U.S. unemployment rate surged during and after each recession but eventually fell during periods of expansion. The rising unemployment rate in 2008 was a sign that a new recession might be under way, which was later confirmed by the NBER to have begun in December 2007.

Because recessions cause many people to lose their jobs and also make it hard to find new ones, recessions hurt the standard of living of many families. Recessions are usually associated with a rise in the number of people living below the poverty line, an increase in the number of people who lose their houses because they can’t afford the mortgage payments, and a fall in the percentage of Americans with health insurance coverage.

You should not think, however, that workers are the only group that suffers during a recession. Recessions are also bad for firms: like employment and wages, profits suffer during recessions, with many small businesses failing.

All in all, then, recessions are bad for almost everyone. Can anything be done to reduce their frequency and severity?

!worldview! FOR INQUIRING MINDS: Defining Recessions and Expansions

Some readers may be wondering exactly how recessions and expansions are defined. The answer is that there is no exact definition!

In many countries, economists adopt the rule that a recession is a period of at least two consecutive quarters (a quarter is three months) during which the total output of the economy shrinks. The two-

Sometimes, however, this definition seems too strict. For example, an economy that has three months of sharply declining output, then three months of slightly positive growth, then another three months of rapid decline, should surely be considered to have endured a nine-

In the United States, we try to avoid such misclassifications by assigning the task of determining when a recession begins and ends to an independent panel of experts at the National Bureau of Economic Research (NBER). This panel looks at a variety of economic indicators, with the main focus on employment and production. But, ultimately, the panel makes a judgment call.

Sometimes this judgment is controversial. In fact, there is lingering controversy over the 2001 recession. According to the NBER, that recession began in March 2001 and ended in November 2001 when output began rising. Some critics argue, however, that the recession really began several months earlier, when industrial production began falling. Other critics argue that the recession didn’t really end in 2001 because employment continued to fall and the job market remained weak for another year and a half.

Taming the Business Cycle

Modern macroeconomics largely came into being as a response to the worst recession in history—

As we explained earlier in this chapter, the work of John Maynard Keynes, published during the Great Depression, suggested that monetary and fiscal policies could be used to mitigate the effects of recessions, and to this day governments turn to Keynesian policies when recession strikes. Later work, notably that of another great macroeconomist, Milton Friedman, led to a consensus that it’s important to rein in booms as well as to fight slumps. So modern policy makers try to “smooth out” the business cycle. They haven’t been completely successful, as a look back at Figure 21-2 makes clear. It’s widely believed, however, that policy guided by macroeconomic analysis has helped make the economy more stable.

Although the business cycle is one of the main concerns of macroeconomics and historically played a crucial role in fostering the development of the field, macroeconomists are also concerned with other issues. We turn next to the question of long-

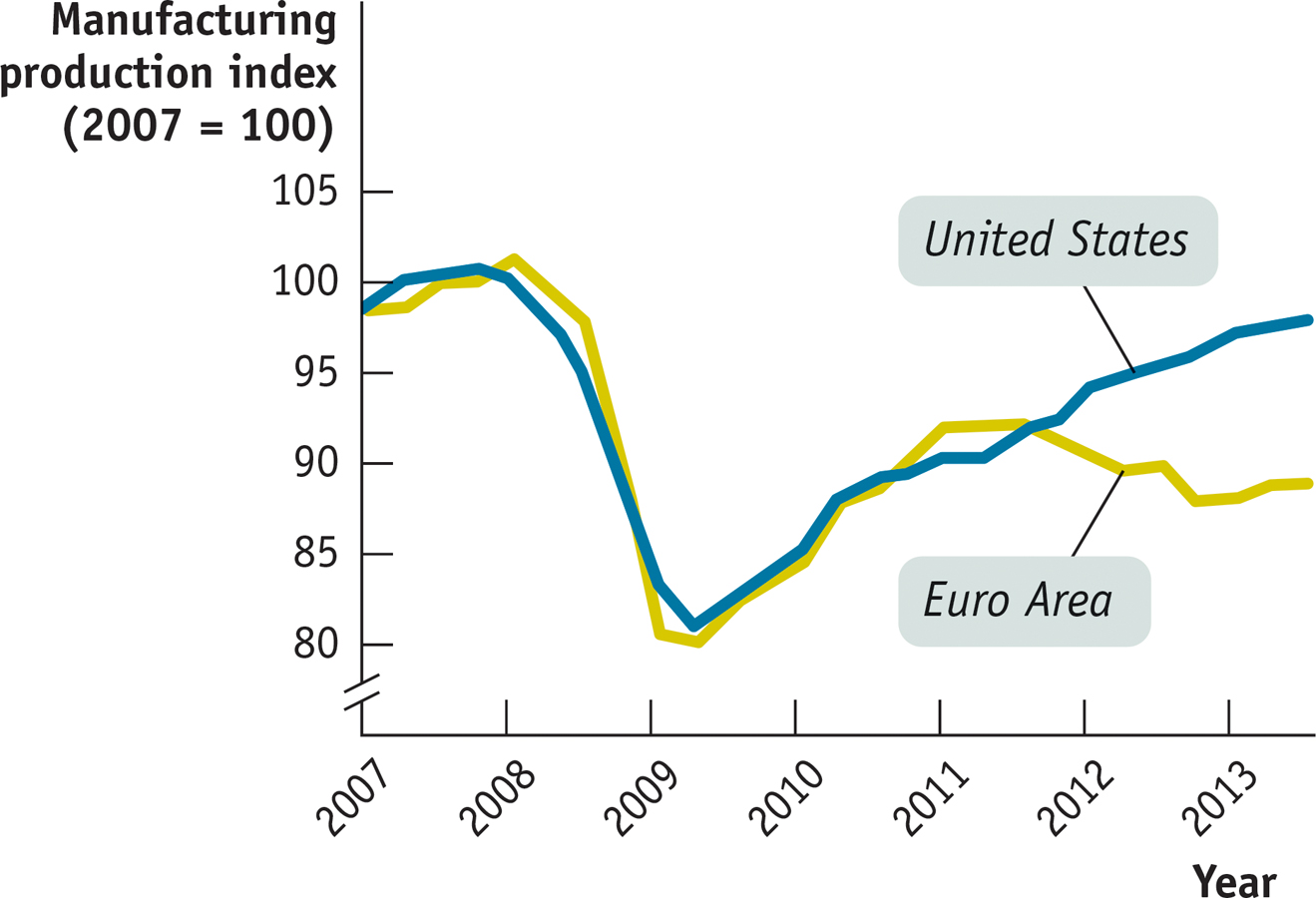

Slumps Across the Atlantic

This figure shows manufacturing production from 2007 to 2013 in two of the world’s biggest economies: the United States and the Euro Area, the group of European countries that share a common currency, the euro. As you can see, both economies suffered a severe downturn in 2008–

More or less simultaneous recessions in different countries are, in fact, quite common. But that doesn’t mean that economies always or even usually move in lockstep. As you can see from the figure, both the Euro Area and the United States began to recover in mid-

What we learn from recent experience, then, is that the business cycle is to some extent an international phenomenon. But individual countries can diverge from each other for a variety of reasons, including policy differences and differences in the underlying structure of their economies.

Source: Federal Reserve Bank of St. Louis.

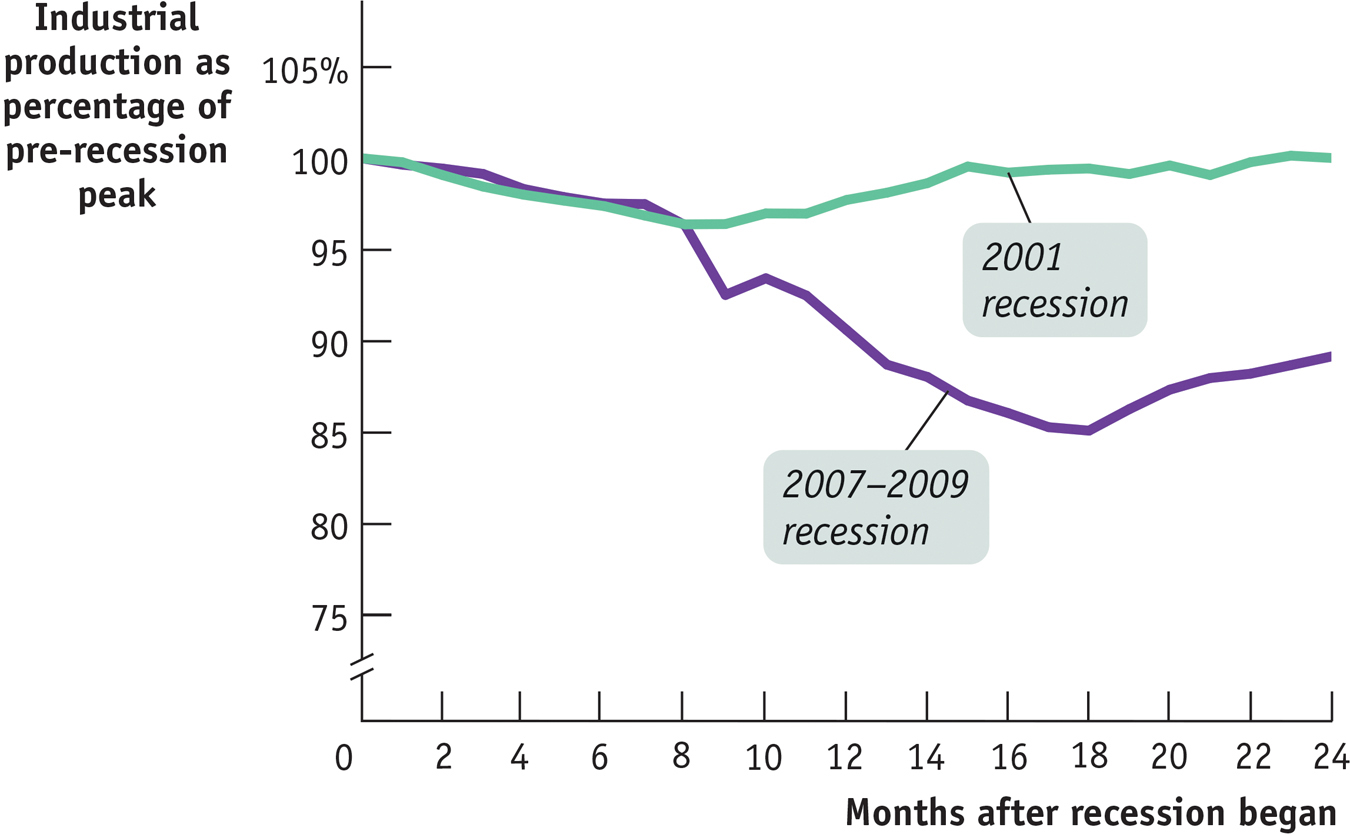

ECONOMICS in Action: Comparing Recessions

Comparing Recessions

The alternation of recessions and expansions seems to be an enduring feature of economic life. However, not all business cycles are created equal. In particular, some recessions have been much worse than others.

Let’s compare the two most recent U.S. recessions: the 2001 recession and the Great Recession of 2007–

In Figure 21-5 we compare the depth of the recessions by looking at what happened to industrial production over the months after the recession began. In each case, production is measured as a percentage of its level at the recession’s start. Thus the line for the 2007–

Clearly, the 2007–

Of course, this was no consolation to the millions of American workers who lost their jobs, even in that mild recession.

Quick Review

The business cycle, the short-

run alternation between recessions and expansions, is a major concern of modern macroeconomics. The point at which expansion shifts to recession is a business-

cycle peak. The point at which recession shifts to expansion is a business- cycle trough.

21-2

Question 6.3

Why do we talk about business cycles for the economy as a whole, rather than just talking about the ups and downs of particular industries?

Question 6.4

Describe who gets hurt in a recession, and how.

Solutions appear at back of book.