Real GDP: A Measure of Aggregate Output

In this chapter’s opening story, we described how China passed Japan as the world’s second-

The moral of this story is that the commonly cited GDP number is an interesting and useful statistic, one that provides a good way to compare the size of different economies, but it’s not a good measure of the economy’s growth over time. GDP can grow because the economy grows, but it can also grow simply because of inflation. Even if an economy’s output doesn’t change, GDP will go up if the prices of the goods and services the economy produces have increased. Likewise, GDP can fall either because the economy is producing less or because prices have fallen.

Aggregate output is the economy’s total quantity of output of final goods and services.

In order to accurately measure the economy’s growth, we need a measure of aggregate output: the total quantity of final goods and services the economy produces. The measure that is used for this purpose is known as real GDP. By tracking real GDP over time, we avoid the problem of changes in prices distorting the value of changes in production of goods and services over time. Let’s look first at how real GDP is calculated, then at what it means.

Calculating Real GDP

To understand how real GDP is calculated, imagine an economy in which only two goods, apples and oranges, are produced and in which both goods are sold only to final consumers. The outputs and prices of the two fruits for two consecutive years are shown in Table 22-1.

|

|

Year 1 |

Year 2 |

|---|---|---|

|

Quantity of apples (billions) |

2,000 |

2,200 |

|

Price of apple |

$0.25 |

$0.30 |

|

Quantity of oranges (billions) |

1,000 |

1,200 |

|

Price of orange |

$0.50 |

$0.70 |

|

GDP (billions of dollars) |

$1,000 |

$1,500 |

|

Real GDP (billions of year 1 dollars) |

$1,000 |

$1,150 |

TABLE 7-

The first thing we can say about these data is that the value of sales increased from year 1 to year 2. In the first year, the total value of sales was (2,000 billion × $0.25) + (1,000 billion × $0.50) = $1,000 billion; in the second it was (2,200 billion × $0.30) + (1,200 billion × $0.70) = $1,500 billion, which is 50% larger. But it is also clear from the table that this increase in the dollar value of GDP overstates the real growth in the economy. Although the quantities of both apples and oranges increased, the prices of both apples and oranges also rose. So part of the 50% increase in the dollar value of GDP from year 1 to year 2 simply reflects higher prices, not higher production of output.

To estimate the true increase in aggregate output produced, we have to ask the following question: how much would GDP have gone up if prices had not changed? To answer this question, we need to find the value of output in year 2 expressed in year 1 prices. In year 1 the price of apples was $0.25 each and the price of oranges $0.50 each. So year 2 output at year 1 prices is (2,200 billion × $0.25) + (1,200 billion × $0.50) = $1,150 billion. And output in year 1 at year 1 prices was $1,000 billion. So in this example GDP measured in year 1 prices rose 15%—from $1,000 billion to $1,150 billion.

Real GDP is the total value of all final goods and services produced in the economy during a given year, calculated using the prices of a selected base year.

Now we can define real GDP: it is the total value of final goods and services produced in the economy during a year, calculated as if prices had stayed constant at the level of some given base year. A real GDP number always comes with information about what the base year is.

Nominal GDP is the value of all final goods and services produced in the economy during a given year, calculated using the prices current in the year in which the output is produced.

A GDP number that has not been adjusted for changes in prices is calculated using the prices in the year in which the output is produced. Economists call this measure nominal GDP, GDP at current prices. If we had used nominal GDP to measure the true change in output from year 1 to year 2 in our apples and oranges example, we would have overstated the true growth in output: we would have claimed it to be 50%, when in fact it was only 15%. By comparing output in the two years using a common set of prices—

Table 22-2 shows a real-

|

|

Nominal GDP (billions of current dollars) |

Real GDP (billions of 2009 dollars) |

|---|---|---|

|

2005 |

$13,094 |

$14,234 |

|

2009 |

14,419 |

14,419 |

|

2013 |

16,768 |

15,710 |

TABLE 7-

You might have noticed that there is an alternative way to calculate real GDP using the data in Table 22-1. Why not measure it using the prices of year 2 rather than year 1 as the base-

Chained dollars is the method of calculating changes in real GDP using the average between the growth rate calculated using an early base year and the growth rate calculated using a late base year.

In reality, the government economists who put together the U.S. national accounts have adopted a method to measure the change in real GDP known as chain-

What Real GDP Doesn’t Measure

GDP per capita is GDP divided by the size of the population; it is equivalent to the average GDP per person.

GDP, nominal or real, is a measure of a country’s aggregate output. Other things equal, a country with a larger population will have higher GDP simply because there are more people working. So if we want to compare GDP across countries but want to eliminate the effect of differences in population size, we use the measure GDP per capita—GDP divided by the size of the population, equivalent to the average GDP per person.

Real GDP per capita can be a useful measure in some circumstances, such as in a comparison of labor productivity between countries. However, despite the fact that it is a rough measure of the average real output per person, real GDP per capita has well-

Let’s take a moment to be clear about why a country’s real GDP per capita is not a sufficient measure of human welfare in that country and why growth in real GDP per capita is not an appropriate policy goal in itself.

GDP and the Meaning of Life

“I’ve been rich and I’ve been poor,” the actress Mae West famously declared. “Believe me, rich is better.” But is the same true for countries?

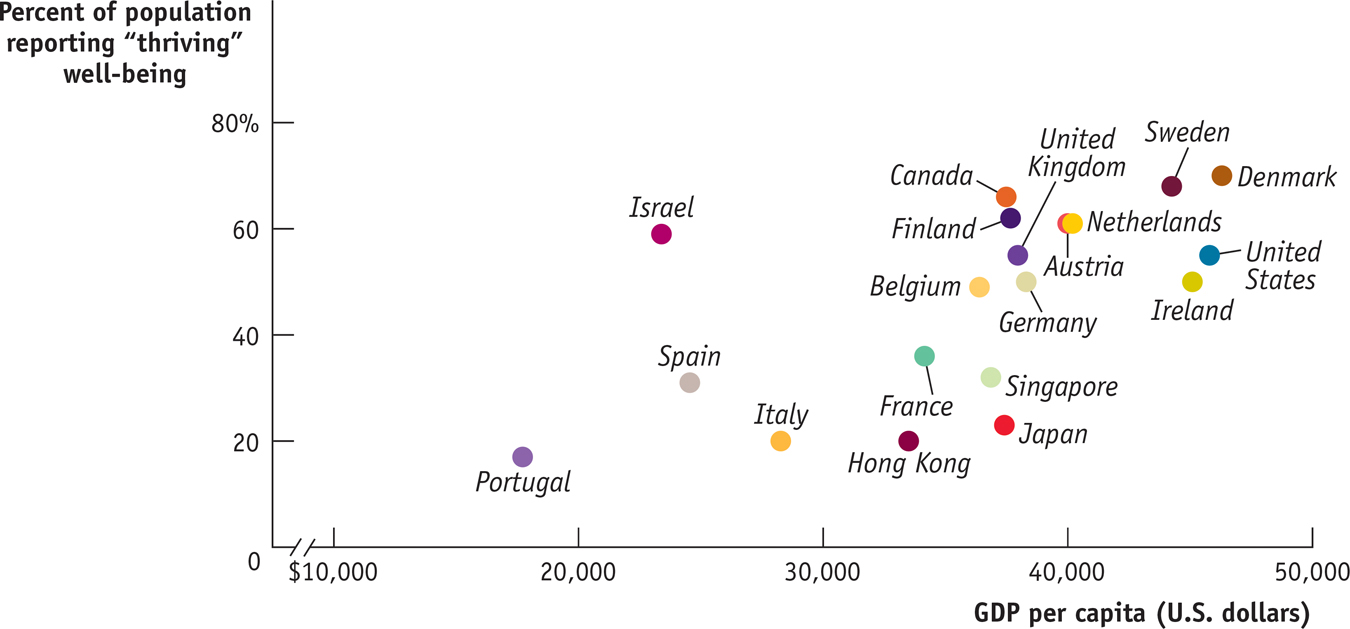

This figure shows two pieces of information for a number of countries: how rich they are, as measured by GDP per capita, and how people assess their well-

Rich is better. Richer countries on average have higher well-

being than poor countries. Money matters less as you grow richer. As GDP rises, the average gain in life satisfaction gets smaller and smaller. For example, the rise in GDP per capita from lower-

income Italy to middle- income Belgium is about the same as from middle- income Belgium to the high- income United States. But the increase in life satisfaction is much greater going from Italy to Belgium compared to going from Belgium to the United States. Money isn’t everything. Israelis, though rich by world standards, are poorer than Americans—

but they seem more satisfied with their lives. Japan is richer than most other nations, but by and large quite miserable.

These results are consistent with the observation that high GDP per capita makes it easier to achieve a good life but that countries aren’t equally successful in taking advantage of that possibility.

Source: Gallup; World Bank.

One way to think about this issue is to say that an increase in real GDP means an expansion in the economy’s production possibility frontier. Because the economy has increased its productive capacity, society can achieve more things. But whether society actually makes good use of that increased potential to improve living standards is another matter. To put it in a slightly different way, your income may be higher this year than last year, but whether you use that higher income to improve your quality of life is your choice.

So let’s say it again: real GDP per capita is a measure of an economy’s average aggregate output per person—

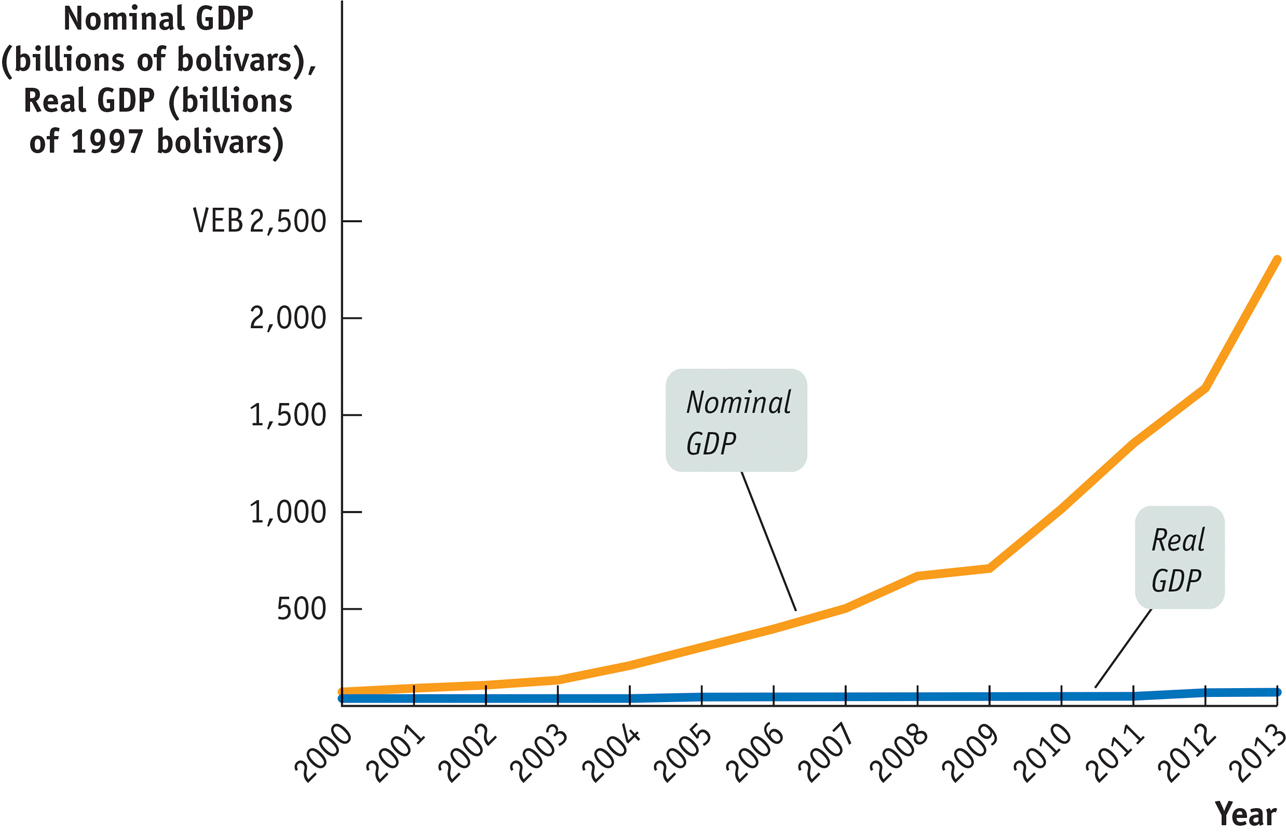

!worldview! ECONOMICS in Action: Miracle in Venezuela?

Miracle in Venezuela?

The South American nation of Venezuela has a distinction that may surprise you: in recent years, it has had one of the world’s fastest-

So is Venezuela experiencing an economic miracle? No, it’s just suffering from unusually high inflation. Figure 22-4 shows Venezuela’s nominal and real GDP from 2000 to 2013, with real GDP measured in 1997 prices. Real GDP did grow over the period, but at an annual rate of only 3.2%. That’s about twice the U.S. growth rate over the same period, but it is far short of China’s 10% growth.

Quick Review

To determine the actual growth in aggregate output, we calculate real GDP using prices from some given base year. In contrast, nominal GDP is the value of aggregate output calculated with current prices. U.S. statistics on real GDP are always expressed in chained dollars.

Real GDP per capita is a measure of the average aggregate output per person. But it is not a sufficient measure of human welfare, nor is it an appropriate goal in itself, because it does not reflect important aspects of living standards within an economy.

22-2

Question 7.4

Assume there are only two goods in the economy, french fries and onion rings. In 2013, 1,000,000 servings of french fries were sold at $0.40 each and 800,000 servings of onion rings at $0.60 each. From 2013 to 2014, the price of french fries rose by 25% and the servings sold fell by 10%; the price of onion rings fell by 15% and the servings sold rose by 5%.

Calculate nominal GDP in 2013 and 2014. Calculate real GDP in 2014 using 2013 prices.

Why would an assessment of growth using nominal GDP be misguided?

Question 7.5

From 2005 to 2010, the price of electronic equipment fell dramatically and the price of housing rose dramatically. What are the implications of this in deciding whether to use 2005 or 2010 as the base year in calculating 2013 real GDP?

Solutions appear at back of book.