The Role of the Exchange Rate

We’ve just seen how differences in the supply of loanable funds from savings and the demand for loanable funds for investment spending lead to international capital flows. We’ve also learned that a country’s balance of payments on current account plus its balance of payments on financial account add to zero: a country that receives net capital inflows must run a matching current account deficit, and a country that generates net capital outflows must run a matching current account surplus.

The behavior of the financial account—

Not surprisingly, a price is what makes these two accounts balance. Specifically, that price is the exchange rate, which is determined in the foreign exchange market.

Understanding Exchange Rates

Currencies are traded in the foreign exchange market.

The prices at which currencies trade are known as exchange rates.

In general, goods, services, and assets produced in a country must be paid for in that country’s currency. American products must be paid for in dollars; European products must be paid for in euros; Japanese products must be paid for in yen. Occasionally, sellers will accept payment in foreign currency, but they will then exchange that currency for domestic money.

|

|

U.S. dollars |

Yen |

Euros |

|---|---|---|---|

|

One U.S. dollar exchanged for |

1 |

117.76 |

0.8072 |

|

One yen exchanged for |

0.0085 |

1 |

0.0069 |

|

One euro exchanged for |

1.2388 |

145.88 |

1 |

TABLE 19-

International transactions, then, require a market—

When a currency becomes more valuable in terms of other currencies, it appreciates.

When a currency becomes less valuable in terms of other currencies, it depreciates.

Table 34-3 shows exchange rates among the world’s three most important currencies as of 2 p.m., EDT, on Nov. 21, 2014. Each entry shows the price of the “row” currency in terms of the “column” currency. For example, at that time US$1 exchanged for €0.8072, so it took €0.8072 to buy US$1. Similarly, it took US$1.2388 to buy €1. These two numbers reflect the same rate of exchange between the euro and the U.S. dollar: 1/1.2388 = 0.8072.

PITFALLS: WHICH WAY IS UP?

WHICH WAY IS UP?

Suppose someone says, “The U.S. exchange rate is up.” What does that person mean?

It isn’t clear. Sometimes the exchange rate is measured as the price of a dollar in terms of foreign currency, sometimes as the price of foreign currency in terms of dollars. So the statement could mean either that the dollar appreciated or that it depreciated!

You have to be particularly careful when using published statistics. Most countries other than the United States state their exchange rates in terms of the price of a dollar in their domestic currency—

By the way, Americans generally follow other countries’ lead: we usually say that the exchange rate against Mexico is 10 pesos per dollar but that the exchange rate against Britain is 1.57 dollars per pound. But this rule isn’t reliable; exchange rates against the euro are often stated both ways.

So it’s always important to check before using exchange rate data: which way is the exchange rate being measured?

There are two ways to write any given exchange rate. In this case, there were €0.8072 to US$1 and US$1.2388 to €1. Which is the correct way to write it? The answer is that there is no fixed rule. In most countries, people tend to express the exchange rate as the price of a dollar in domestic currency. However, this rule isn’t universal, and the U.S. dollar–

When discussing movements in exchange rates, economists use specialized terms to avoid confusion. When a currency becomes more valuable in terms of other currencies, economists say that the currency appreciates. When a currency becomes less valuable in terms of other currencies, it depreciates. Suppose, for example, that the value of €1 went from $1 to $1.25, which means that the value of US$1 went from €1 to €0.80 (because 1/1.25 = 0.80). In this case, we would say that the euro appreciated and the U.S. dollar depreciated.

Movements in exchange rates, other things equal, affect the relative prices of goods, services, and assets in different countries. Suppose, for example, that the price of an American hotel room is US$100 and the price of a French hotel room is €100. If the exchange rate is €1 = US$1, these hotel rooms have the same price. If the exchange rate is €1.25 = US$1, the French hotel room is 20% cheaper than the American hotel room. If the exchange rate is €0.80 = US$1, the French hotel room is 25% more expensive than the American hotel room.

But what determines exchange rates? Supply and demand in the foreign exchange market.

The Equilibrium Exchange Rate

Imagine, for the sake of simplicity, that there are only two currencies in the world: U.S. dollars and euros. Europeans wanting to purchase American goods, services, and assets come to the foreign exchange market, wanting to exchange euros for U.S. dollars. That is, Europeans demand U.S. dollars from the foreign exchange market and, correspondingly, supply euros to that market. Americans wanting to buy European goods, services, and assets come to the foreign exchange market to exchange U.S. dollars for euros. That is, Americans supply U.S. dollars to the foreign exchange market and, correspondingly, demand euros from that market. (International transfers and payments of factor income also enter into the foreign exchange market, but to make things simple we’ll ignore these.)

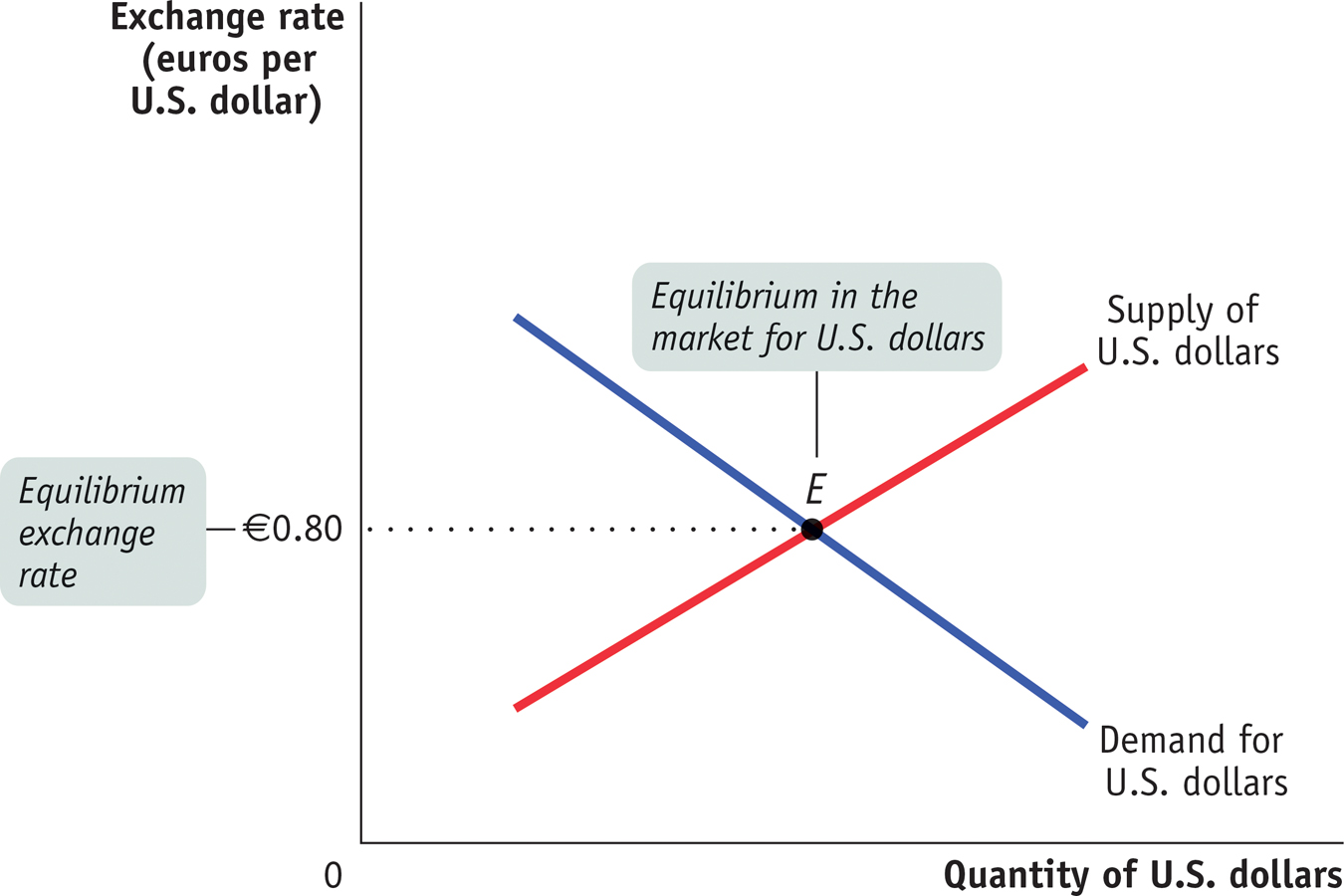

Figure 34-5 shows how the foreign exchange market works. The quantity of dollars demanded and supplied at any given euro–

The figure shows two curves, the demand curve for U.S. dollars and the supply curve for U.S. dollars. The key to understanding the slopes of these curves is that the level of the exchange rate affects exports and imports. When a country’s currency appreciates (becomes more valuable), exports fall and imports rise. When a country’s currency depreciates (becomes less valuable), exports rise and imports fall.

To understand why the demand curve for U.S. dollars slopes downward, recall that the exchange rate, other things equal, determines the prices of American goods, services, and assets relative to those of European goods, services, and assets. If the U.S. dollar rises against the euro (the dollar appreciates), American products will become more expensive to Europeans relative to European products. So Europeans will buy less from the United States and will acquire fewer dollars in the foreign exchange market: the quantity of U.S. dollars demanded falls as the number of euros needed to buy a U.S. dollar rises. If the U.S. dollar falls against the euro (the dollar depreciates), American products will become relatively cheaper for Europeans. Europeans will respond by buying more from the United States and acquiring more dollars in the foreign exchange market: the quantity of U.S. dollars demanded rises as the number of euros needed to buy a U.S. dollar falls.

A similar argument explains why the supply curve of U.S. dollars in Figure 34-5 slopes upward: the more euros required to buy a U.S. dollar, the more dollars Americans will supply. Again, the reason is the effect of the exchange rate on relative prices. If the U.S. dollar rises against the euro, European products look cheaper to Americans—

The equilibrium exchange rate is the exchange rate at which the quantity of a currency demanded in the foreign exchange market is equal to the quantity supplied.

The equilibrium exchange rate is the exchange rate at which the quantity of U.S. dollars demanded in the foreign exchange market is equal to the quantity of U.S. dollars supplied. In Figure 34-5, the equilibrium is at point E, and the equilibrium exchange rate is 0.80. That is, at an exchange rate of €0.80 per US$1, the quantity of U.S. dollars supplied to the foreign exchange market is equal to the quantity of U.S. dollars demanded.

To understand the significance of the equilibrium exchange rate, it’s helpful to consider a numerical example of what equilibrium in the foreign exchange market looks like. A hypothetical example is shown in Table 34-4. The first row shows European purchases of U.S. dollars, either to buy U.S. goods and services or to buy U.S. assets. The second row shows U.S. sales of U.S. dollars, either to buy European goods and services or to buy European assets. At the equilibrium exchange rate, the total quantity of U.S. dollars Europeans want to buy is equal to the total quantity of U.S. dollars Americans want to sell.

|

European purchases of U.S. dollars (trillions of U.S. dollars) |

To buy U.S. goods and services: 1.0 |

To buy U.S. assets: 1.0 |

Total purchases of U.S. dollars: 2.0 |

|

U.S. sales of U.S. dollars (trillions of U.S. dollars) |

To buy European goods and services: 1.5 |

To buy European assets: 0.5 |

Total sales of U.S. dollars: 2.0 |

|

|

U.S. balance of payments on current account: –0.5 |

U.S. balance of payments on financial account: +0.5 |

|

TABLE 19-

Remember that the balance of payments accounts divide international transactions into two types. Purchases and sales of goods and services are counted in the current account. (Again, we’re leaving out transfers and factor income to keep things simple.) Purchases and sales of assets are counted in the financial account. At the equilibrium exchange rate, then, we have the situation shown in Table 34-4: the sum of the balance of payments on current account plus the balance of payments on financial account is zero.

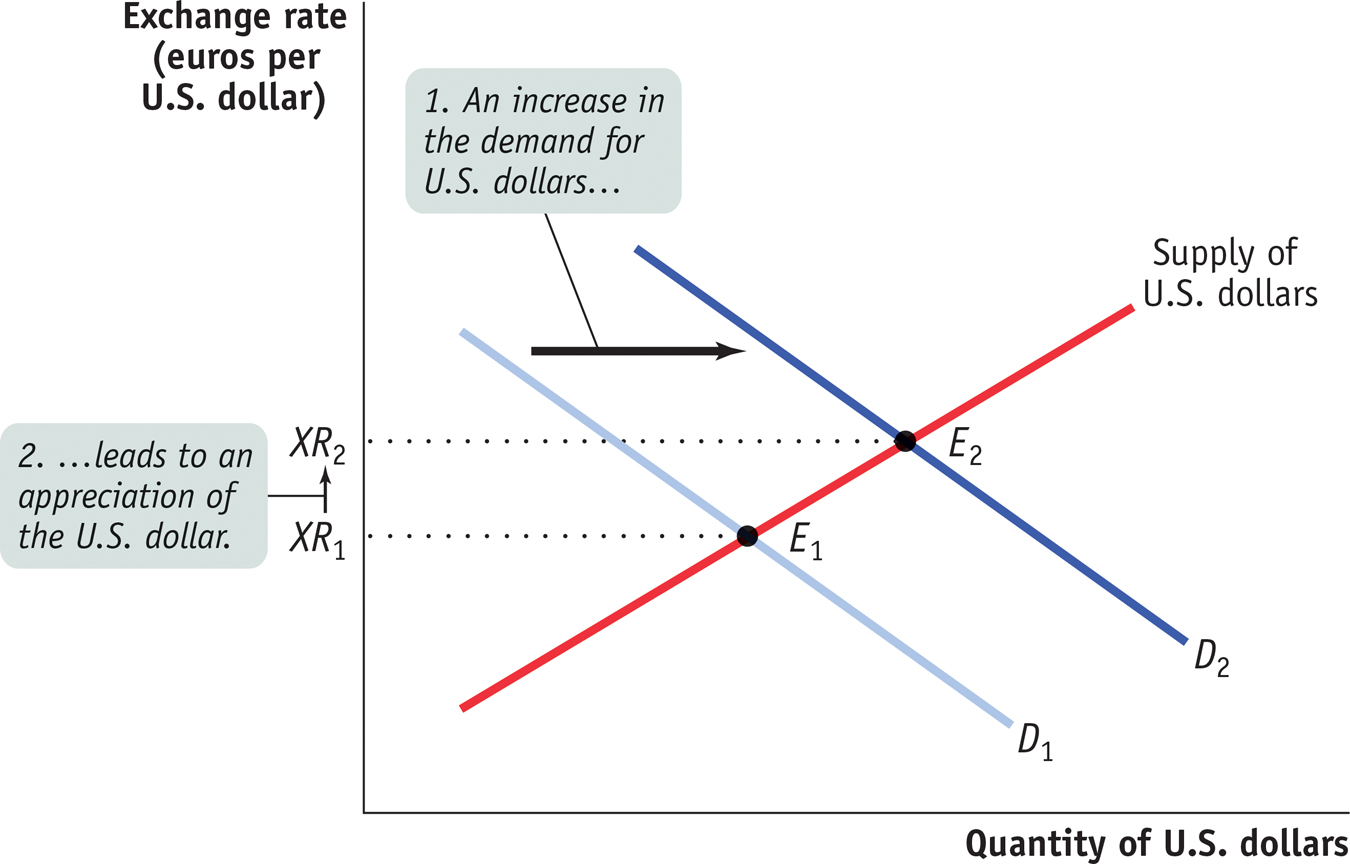

Now let’s briefly consider how a shift in the demand for U.S. dollars affects equilibrium in the foreign exchange market. Suppose that for some reason capital flows from Europe to the United States increase—

What are the consequences of this increased capital inflow for the balance of payments? The total quantity of U.S. dollars supplied to the foreign exchange market still must equal the total quantity of U.S. dollars demanded. So the increased capital inflow to the United States—

|

European purchases of U.S. dollars (trillions of U.S. dollars) |

To buy U.S. goods and services: 0.75 (down 0.25) |

To buy U.S. assets: 1.5 (up 0.5) |

Total purchases of U.S. dollars: 2.25 |

|

U.S. sales of U.S. dollars (trillions of U.S. dollars) |

To buy European goods and services: 1.75 (up 0.25) |

To buy European assets: 0.5 (no change) |

Total sales of U.S. dollars: 2.25 |

|

|

U.S. balance of payments on current account: –1.0 (down 0.5) |

U.S. balance of payments on financial account: +1.0 (up 0.5) |

|

TABLE 19-

Table 34-5 shows a hypothetical example of how this might work. Europeans are buying more U.S. assets, increasing the balance of payments on financial account from 0.5 to 1.0. This is offset by a reduction in European purchases of U.S. goods and services and a rise in U.S. purchases of European goods and services, both the result of the dollar’s appreciation. So any change in the U.S. balance of payments on financial account generates an equal and opposite reaction in the balance of payments on current account. Movements in the exchange rate ensure that changes in the financial account and in the current account offset each other.

Let’s briefly run this process in reverse. Suppose there is a reduction in capital flows from Europe to the United States—

Inflation and Real Exchange Rates

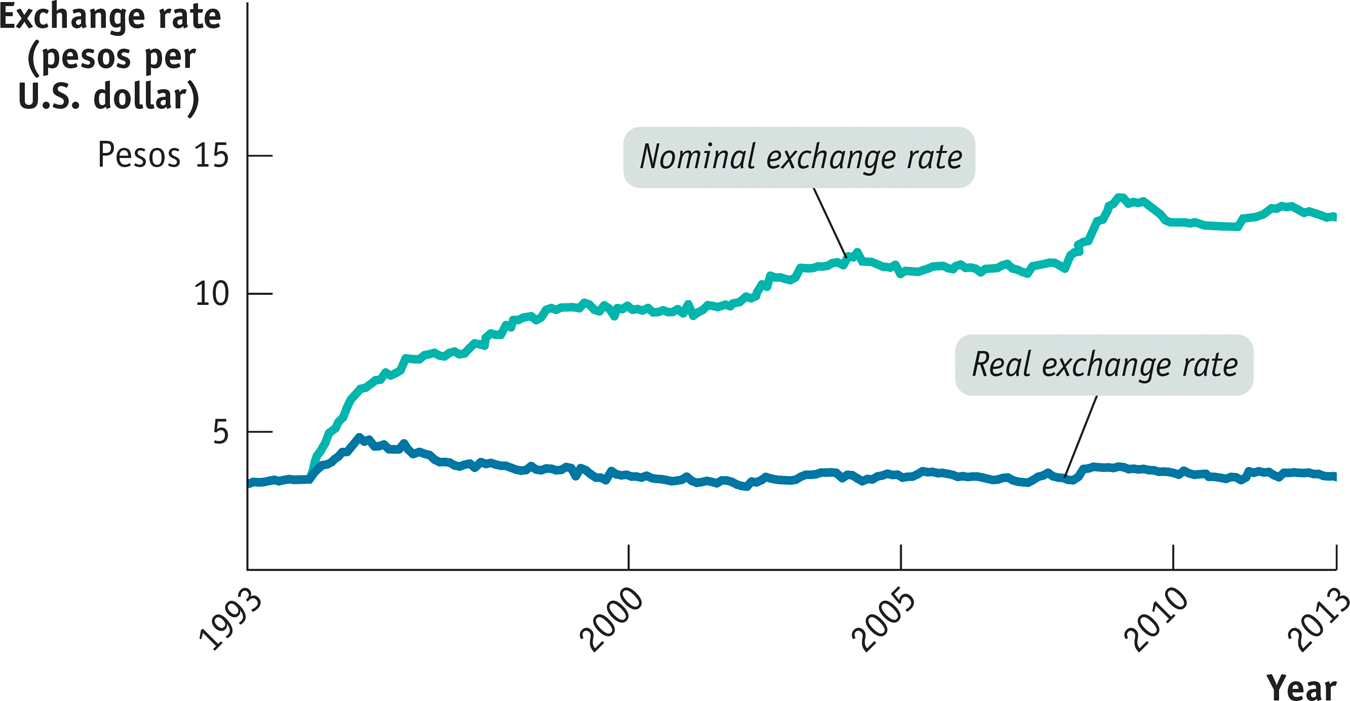

In 1993 one U.S. dollar exchanged, on average, for 3.1 Mexican pesos. By 2013, the peso had fallen against the dollar by more than 75%, with an average exchange rate in 2013 of 12.8 pesos per dollar. Did Mexican products also become much cheaper relative to U.S. products over that 20-

Real exchange rates are exchange rates adjusted for international differences in aggregate price levels.

To take account of the effects of differences in inflation rates, economists calculate real exchange rates, exchange rates adjusted for international differences in aggregate price levels. Suppose that the exchange rate we are looking at is the number of Mexican pesos per U.S. dollar. Let PUS and PMex be indexes of the aggregate price levels in the United States and Mexico, respectively. Then the real exchange rate between the Mexican peso and the U.S. dollar is defined as:

To distinguish it from the real exchange rate, the exchange rate unadjusted for aggregate price levels is sometimes called the nominal exchange rate.

To understand the significance of the difference between the real and nominal exchange rates, let’s consider the following example. Suppose that the Mexican peso depreciates against the U.S. dollar, with the exchange rate going from 10 pesos per U.S. dollar to 15 pesos per U.S. dollar, a 50% change. But suppose that at the same time the price of everything in Mexico, measured in pesos, increases by 50%, so that the Mexican price index rises from 100 to 150. At the same time, suppose that there is no change in U.S. prices, so that the U.S. price index remains at 100. Then the initial real exchange rate is:

After the peso depreciates and the Mexican price level increases, the real exchange rate is:

In this example, the peso has depreciated substantially in terms of the U.S. dollar, but the real exchange rate between the peso and the U.S. dollar hasn’t changed at all. And because the real peso–

To see why, consider again the example of a hotel room. Suppose that this room initially costs 1,000 pesos per night, which is $100 at an exchange rate of 10 pesos per dollar. After both Mexican prices and the number of pesos per dollar rise by 50%, the hotel room costs 1,500 pesos per night—

The same is true for all goods and services that enter into trade: the current account responds only to changes in the real exchange rate, not the nominal exchange rate. A country’s products become cheaper to foreigners only when that country’s currency depreciates in real terms, and those products become more expensive to foreigners only when the currency appreciates in real terms. As a consequence, economists who analyze movements in exports and imports of goods and services focus on the real exchange rate, not the nominal exchange rate.

Figure 34-7 illustrates just how important it can be to distinguish between nominal and real exchange rates. The line labeled “Nominal exchange rate” shows the number of pesos it took to buy a U.S. dollar from 1993 to 2013. As you can see, the peso depreciated massively over that period. But the line labeled “Real exchange rate” shows the real exchange rate: it was calculated using Equation 34-

Purchasing Power Parity

The purchasing power parity between two countries’ currencies is the nominal exchange rate at which a given basket of goods and services would cost the same amount in each country.

A useful tool for analyzing exchange rates, closely connected to the concept of the real exchange rate, is known as purchasing power parity. The purchasing power parity between two countries’ currencies is the nominal exchange rate at which a given basket of goods and services would cost the same amount in each country. Suppose, for example, that a basket of goods and services that costs $100 in the United States costs 1,000 pesos in Mexico. Then the purchasing power parity is 10 pesos per U.S. dollar: at that exchange rate, 1,000 pesos = $100, so the market basket costs the same amount in both countries.

Calculations of purchasing power parities are usually made by estimating the cost of buying broad market baskets containing many goods and services—

!worldview! FOR INQUIRING MINDS: Burgernomics

For a number of years the British magazine The Economist has produced an annual comparison of the cost in different countries of one particular consumption item that is found around the world—

Table 34-6 shows the Economist estimates for selected countries as of July 2014, ranked in increasing order of the dollar price of a Big Mac. The countries with the cheapest Big Macs, and therefore by this measure with the most undervalued currencies, are India and China, both developing countries. But not all developing countries have low-

|

|

Big Mac price |

Local currency per dollar |

||

|---|---|---|---|---|

|

Country |

In local currency |

In U.S. dollars |

Implied PPP |

Actual exchange rate |

|

India |

Rupee 105 |

1.75 |

21.90 |

60.09 |

|

China |

Yuan 16.9 |

2.73 |

3.52 |

6.20 |

|

Mexico |

Peso 42 |

3.25 |

8.76 |

12.93 |

|

Britain |

£ 2.89 |

4.93 |

0.60 |

0.59 |

|

United States |

$4.80 |

4.80 |

1.00 |

1.00 |

|

Japan |

¥ 370 |

3.64 |

77.16 |

101.53 |

|

Euro area |

€ 3.68 |

4.95 |

0.77 |

0.74 |

|

Brazil |

Real 13 |

5.86 |

2.71 |

2.22 |

|

Switzerland |

SFr 6.16 |

6.83 |

1.28 |

0.90 |

TABLE 19-

And topping the list, with a Big Mac some 75% more expensive than in the United States, is Switzerland—

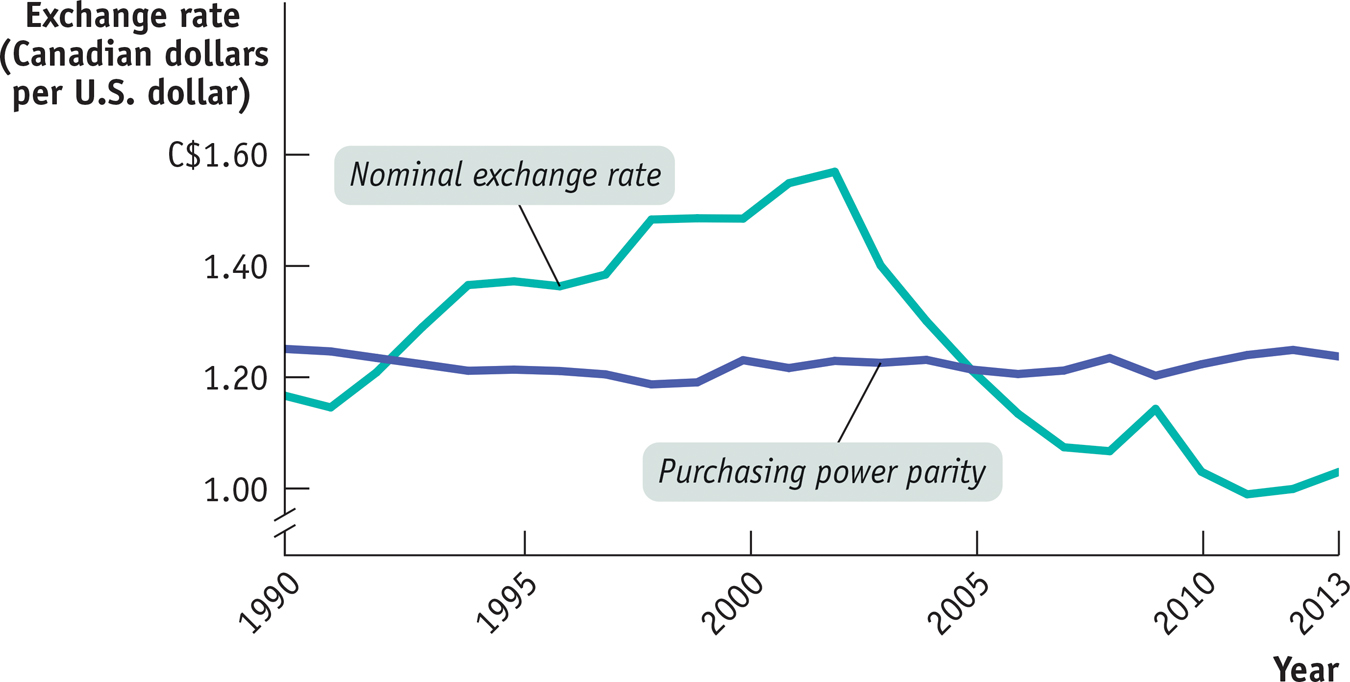

Nominal exchange rates almost always differ from purchasing power parities. Some of these differences are systematic: in general, aggregate price levels are lower in poor countries than in rich countries because services tend to be cheaper in poor countries. But even among countries at roughly the same level of economic development, nominal exchange rates vary quite a lot from purchasing power parity. Figure 34-8 shows the nominal exchange rate between the Canadian dollar and the U.S. dollar, measured as the number of Canadian dollars per U.S. dollar, from 1990 to 2013, together with an estimate of the purchasing power parity exchange rate between the United States and Canada over the same period.

The purchasing power parity didn’t change much over the whole period because the United States and Canada had about the same rate of inflation. But at the beginning of the period the nominal exchange rate was below purchasing power parity, so a given market basket was more expensive in Canada than in the United States. By 2002 the nominal exchange rate was far above the purchasing power parity, so a market basket was much cheaper in Canada than in the United States.

Over the long run, however, purchasing power parities are pretty good at predicting actual changes in nominal exchange rates. In particular, nominal exchange rates between countries at similar levels of economic development tend to fluctuate around levels that lead to similar costs for a given market basket. In fact, by July 2005 the nominal exchange rate between the United States and Canada was C$1.22 per US$1—

!worldview! ECONOMICS in Action: Low-

Low-

Does the exchange rate matter for business decisions? And how. Consider what European auto manufacturers were doing in 2008. One report from the University of Iowa summarized the situation as follows:

While luxury German carmakers BMW and Mercedes have maintained plants in the American South since the 1990s, BMW aims to expand U.S. manufacturing in South Carolina by 50% during the next 5 years. Volvo of Sweden is in negotiations to build a plant in New Mexico. Analysts at Italian carmaker Fiat determined that it needs to build a North American factory to profit from the upcoming relaunch of its Alfa Romeo model. Tennessee recently closed a deal with Volkswagen to build a $1 billion factory by offering $577 million in incentives.

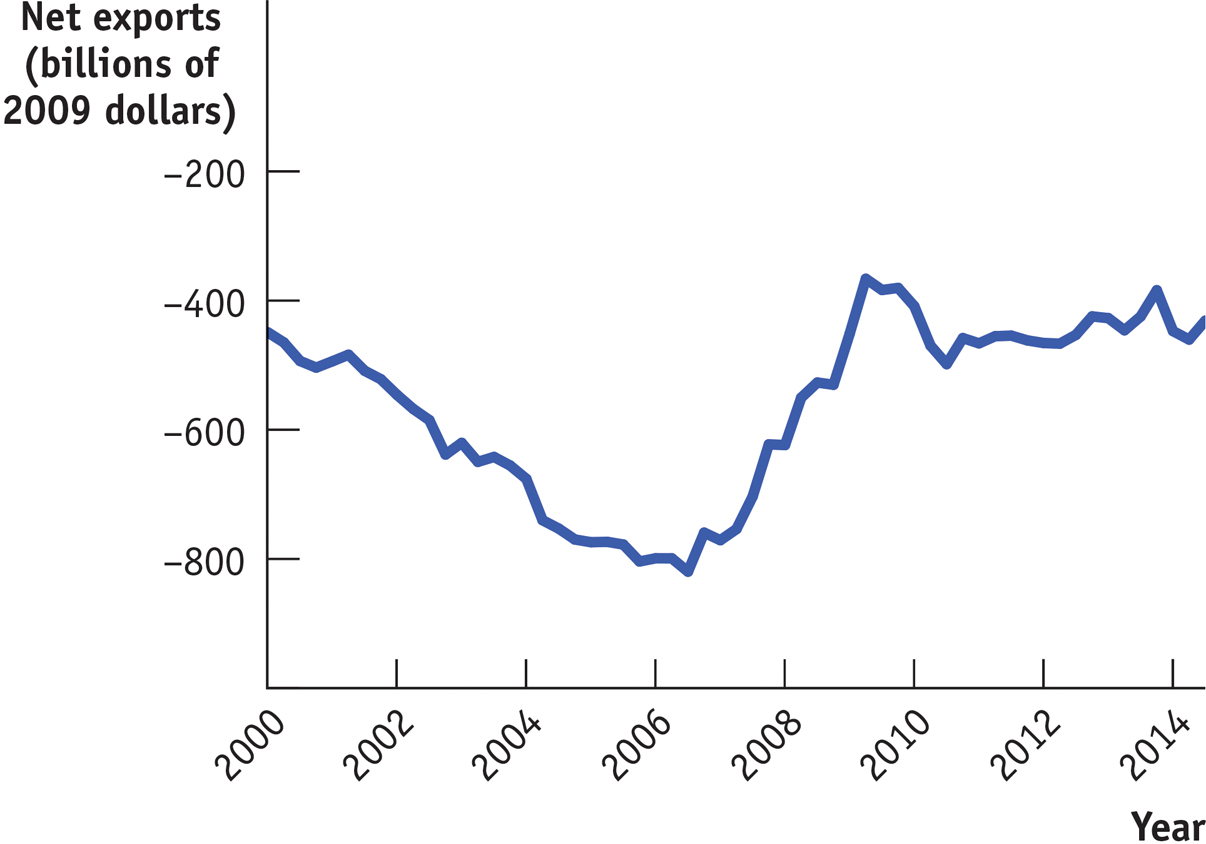

Why were European automakers flocking to America? To some extent because they were being offered special incentives, as the case of Volkswagen in Tennessee illustrates. But the big factor was the exchange rate. In the early 2000s one euro was, on average, worth less than a dollar; by the summer of 2008 the exchange rate was around €1 = $1.50. This change in the exchange rate made it substantially cheaper for European car manufacturers to produce in the United States than at home—

Automobile manufacturing wasn’t the only U.S. industry benefiting from the weak dollar; across the board, U.S. exports surged after 2006 while import growth fell off. Figure 34-9 shows one measure of U.S. trade performance, real net exports of goods and services: exports minus imports, both measured in 2009 dollars. As you can see, this balance, after a long slide, turned sharply upward in 2006. There was a modest reversal in 2009–

Quick Review

Currencies are traded in the foreign exchange market, which determines exchange rates.

Exchange rates can be measured in two ways. To avoid confusion, economists say that a currency appreciates or depreciates. The equilibrium exchange rate matches the supply and demand for currencies on the foreign exchange market.

To take account of differences in national price levels, economists calculate real exchange rates. The current account responds only to changes in the real exchange rate, not the nominal exchange rate.

Purchasing power parity is the nominal exchange rate that equalizes the price of a market basket in the two countries. While the nominal exchange rate almost always differs from purchasing power parity, purchasing power parity is a good predictor of actual changes in the nominal exchange rate.

34-2

Question 19.3

Mexico discovers huge reserves of oil and starts exporting oil to the United States. Describe how this would affect the following.

The nominal peso–

U.S. dollar exchange rate Mexican exports of other goods and services

Mexican imports of goods and services

Question 19.4

A basket of goods and services that costs $100 in the United States costs 800 pesos in Mexico, and the current nominal exchange rate is 10 pesos per U.S. dollar. Over the next five years, the cost of that market basket rises to $120 in the United States and to 1,200 pesos in Mexico, although the nominal exchange rate remains at 10 pesos per U.S. dollar. Calculate the following.

The real exchange rate now and five years from now, if today’s price index in both countries is 100

Purchasing power parity today and five years from now

Solutions appear at back of book.