7.1 The Accumulation of Capital

218

The Solow growth model is designed to show how growth in the capital stock, growth in the labour force, and advances in technology interact in an economy, and how they affect a nation’s total output of goods and services. We build this model in a series of steps. Our first step is to examine how the supply and demand for goods determine the accumulation of capital. In this first step, we assume that the labour force and technology are fixed. We then relax these assumptions, by introducing changes in the labour force later in this chapter and by introducing changes in technology in the next.

The Supply and Demand for Goods

219

The supply and demand for goods played a central role in our static model of the economy in Chapter 3. The same is true for the Solow model. By considering the supply and demand for goods, we can see what determines how much output is produced at any given time and how this output is allocated among alternative uses.

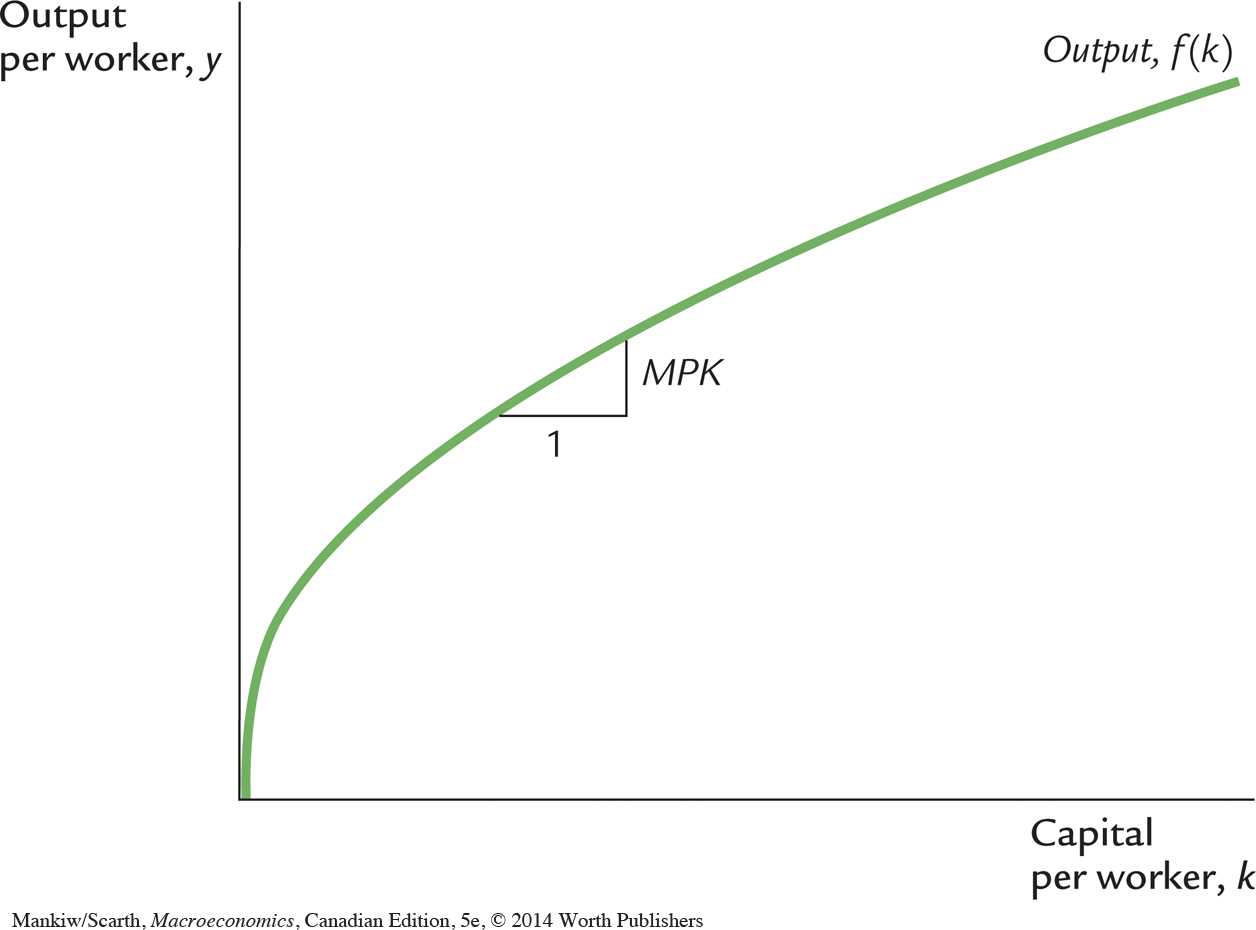

The Supply of Goods and the Production Function The supply of goods in the Solow model is based on the production function, which states that output depends on the capital stock and the labour force:

Y = F(K, L).

The Solow growth model assumes that the production function has constant returns to scale. This assumption is often considered realistic, and as we will see shortly, it helps simplify the analysis. Recall that a production function has constant returns to scale if

zY = F(zK, zL)

for any positive number z. That is, if both capital and labour are multiplied by z, the amount of output is also multiplied by z.

Production functions with constant returns to scale allow us to analyze all quantities in the economy relative to the size of the labour force. To see that this is true, set z = 1/L in the equation above to obtain

Y/L = F(K/L, 1).

This equation shows that the amount of output per worker Y/L is a function of the amount of capital per worker K/L. (The number “1” is, of course, constant and thus can be ignored.) The assumption of constant returns to scale implies that the size of the economy—as measured by the number of workers—does not affect the relationship between output per worker and capital per worker.

Because the size of the economy does not matter, it will prove convenient to denote all quantities in per-worker terms. We designate quantities per worker with lowercase letters, so y = Y/L is output per worker, and k = K/L is capital per worker. We can then write the production function as

y = f(k),

where we define f(k) = F(k,1). Figure 7-1 illustrates this production function.

The slope of this production function shows how much extra output a worker produces when given an extra unit of capital. This amount is the marginal product of capital MPK. Mathematically, we write

MPK = f(k + 1) −f(k).

Note that in Figure 7-1, as the amount of capital increases, the production function becomes flatter, indicating that the production function exhibits diminishing marginal product of capital. When k is low, the average worker has only a little capital to work with, so an extra unit of capital is very useful and produces a lot of additional output. When k is high, the average worker already has a lot of capital, so an extra unit increases production only slightly.

220

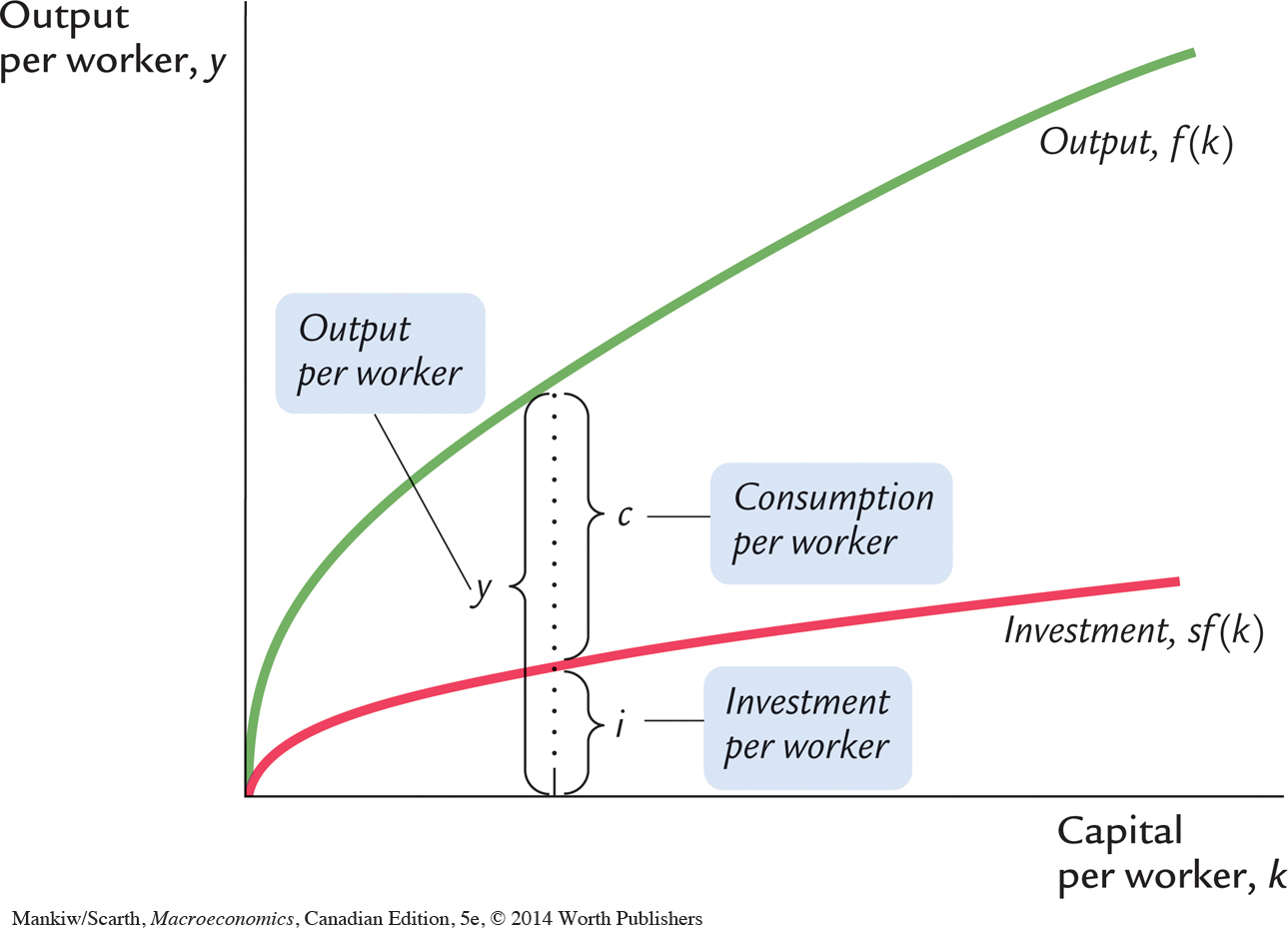

The Demand for Goods and the Consumption Function The demand for goods in the Solow model comes from consumption and investment. In other words, output per worker y is divided between consumption per worker c and investment per worker i:

y = c + i.

This equation is the per-worker version of the national accounts identity for the economy. Notice that it omits government purchases (which for present purposes we can ignore) and net exports (because we are assuming a closed economy).

The Solow model assumes that each year people save a fraction s of their income and consume a fraction (1 − s). We can express this idea with the following consumption function:

c = (1 − s)y,

where s, the saving rate, is a number between zero and one. Keep in mind that various government policies can potentially influence a nation’s saving rate, so one of our goals is to find what saving rate is desirable. For now, however, we just take the saving rate s as given.

To see what this consumption function implies for investment, substitute (1 – s)y for c in the national accounts identity:

y = (1 − s)y + i.

221

Rearrange the terms to obtain

i = sy.

This equation shows that investment equals saving, as we first saw in Chapter 3. Thus, the rate of saving s is also the fraction of output devoted to investment.

We have now introduced the two main ingredients of the Solow model—the production function and the consumption function—which describe the economy at any moment in time. For any given capital stock k, the production function y = f(k) determines how much output the economy produces, and the saving rate s determines the allocation of that output between consumption and investment.

Growth in the Capital Stock and the Steady State

At any moment, the capital stock is a key determinant of the economy’s output, but the capital stock can change over time, and those changes can lead to economic growth. In particular, two forces influence the capital stock: investment and depreciation. Investment is expenditure on new plant and equipment, and it causes the capital stock to rise. Depreciation is the wearing out of old capital, and it causes the capital stock to fall. Let’s consider each of these forces in turn.

As we have already noted, investment per worker i equals sy. By substituting the production function for y, we can express investment per worker as a function of the capital stock per worker:

i = sf(k).

This equation relates the existing stock of capital k to the accumulation of new capital i. Figure 7-2 shows this relationship. This figure illustrates how, for any value of k, the amount of output is determined by the production function f(k), and the allocation of that output between consumption and saving is determined by the saving rate s.

222

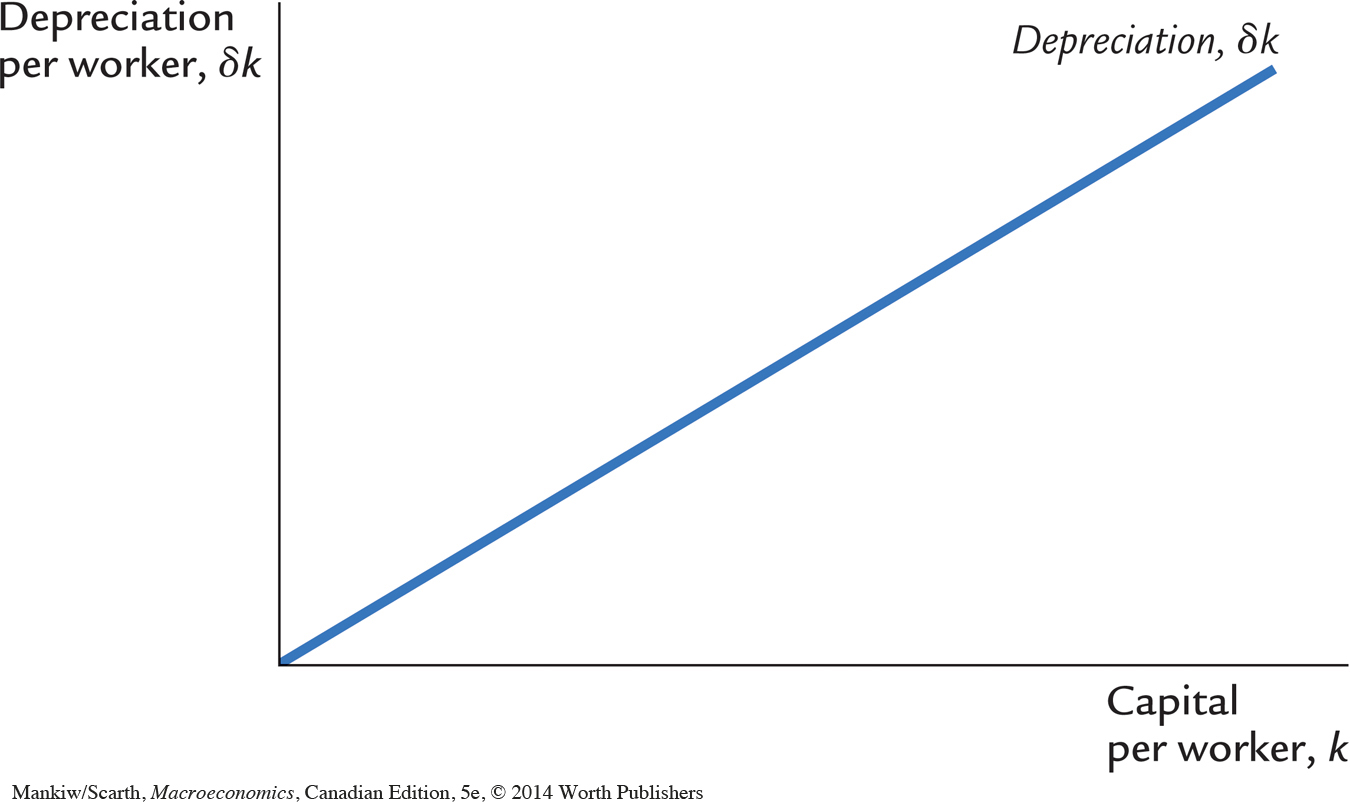

To incorporate depreciation into the model, we assume that a certain fraction δ of the capital stock wears out each year. Here δ (the lowercase Greek letter delta) is called the depreciation rate. For example, if capital lasts an average of 25 years, then the depreciation rate is 4 percent per year (δ = 0.04). The amount of capital that depreciates each year is δk. Figure 7-3 shows how the amount of depreciation depends on the capital stock.

We can express the impact of investment and depreciation on the capital stock with this equation:

Change in Capital Stock = Investment − Depreciation

Δk = i − δk,

where Δk is the change in the capital stock between one year and the next. Because investment i equals sf(k), we can write this as

Δk = sf(k) −δk.

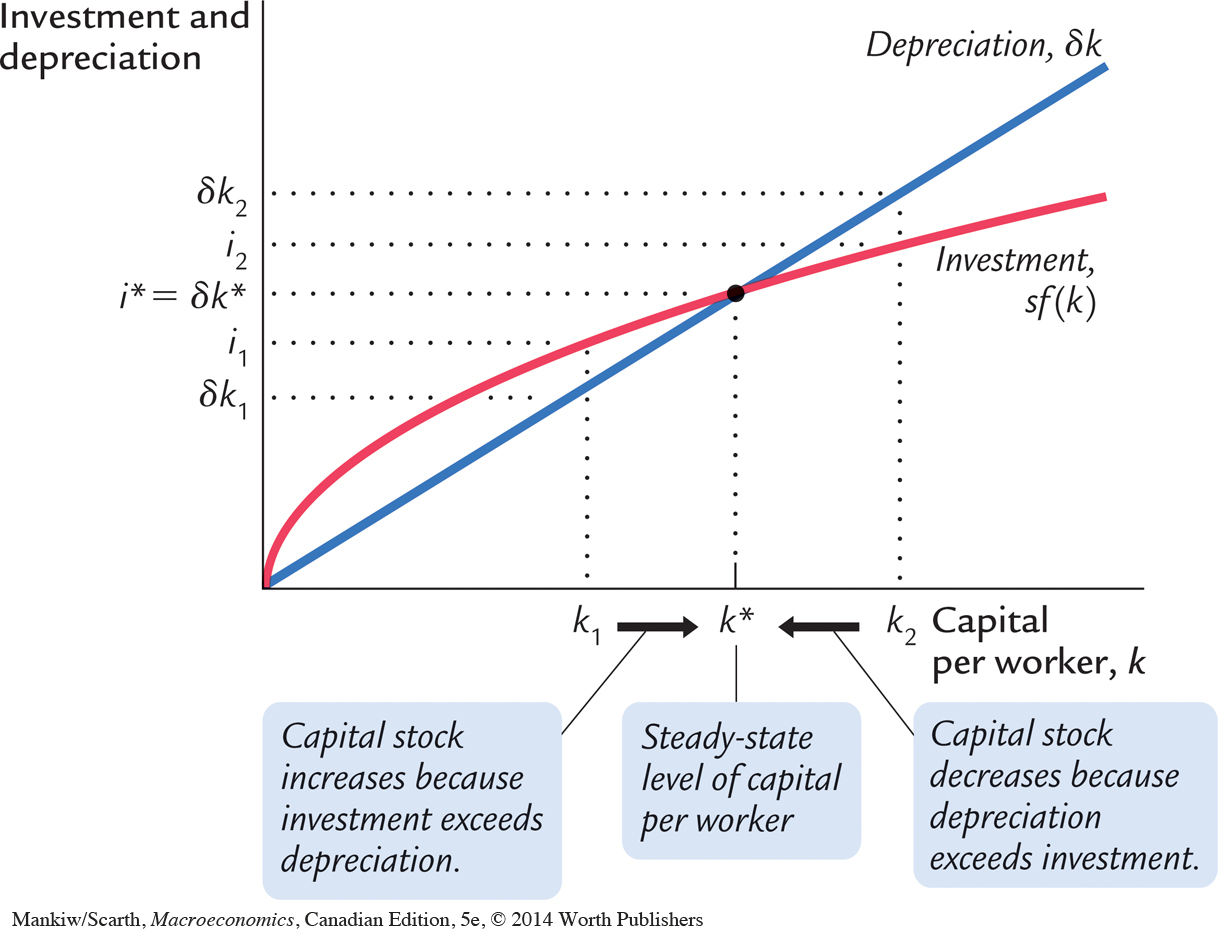

Figure 7-4 graphs the terms of this equation—investment and depreciation—for different levels of the capital stock k. The higher the capital stock, the greater are the amounts of output and investment. Yet the higher the capital stock, the greater also is the amount of depreciation.

As Figure 7-4 shows, there is a single capital stock k* at which the amount of investment equals the amount of depreciation. If the economy finds itself at this level of the capital stock, the capital stock will not change because the two forces acting on it—investment and depreciation—just balance. That is, at k*, Δk = 0, so the capital stock k and output f(k) are steady over time (rather than growing or shrinking). We therefore call k* the steady-state level of capital.

223

The steady state is significant for two reasons. As we have just seen, an economy at the steady state will stay there. In addition, and just as important, an economy not at the steady state will go there. That is, regardless of the level of capital with which the economy begins, it ends up with the steady-state level of capital. In this sense, the steady state represents the long-run equilibrium of the economy.

To see why an economy always ends up at the steady state, suppose that the economy starts with less than the steady-state level of capital, such as level k1 in Figure 7-4. In this case, the level of investment exceeds the amount of depreciation. Over time, the capital stock will rise and will continue to rise—along with output f(k)—until it approaches the steady state k*.

Similarly, suppose that the economy starts with more than the steady-state level of capital, such as level k2. In this case, investment is less than depreciation: capital is wearing out faster than it is being replaced. The capital stock will fall, again approaching the steady-state level. Once the capital stock reaches the steady state, investment equals depreciation, and there is no pressure for the capital stock to increase or decrease.

Approaching the Steady State: A Numerical Example

Let’s use a numerical example to see how the Solow model works and how the economy approaches the steady state. For this example, we assume that the production function is

Y = K1/2L1/2.

224

From Chapter 3, you will recognize this as the Cobb–Douglas production function with the capital share parameter a equal to 1/2. To derive the per-worker production function f(k), divide both sides of the production function by the labour force L:

Rearrange to obtain

Because y = Y/L and k = K/L, this becomes

y = k1/2.

This equation can also be written as

This form of the production function states that output per worker is equal to the square root of the amount of capital per worker.

To complete the example, let’s assume that 30 percent of output is saved (s = 0.3), that 10 percent of the capital stock depreciates every year (δ = 0.1), and that the economy starts off with 4 units of capital per worker (k = 4). Given these numbers, we can now examine what happens to this economy over time.

We begin by looking at the production and allocation of output in the first year, when the economy has 4 units of capital. Here are the steps we follow:

According to the production function, the 4 units of capital per worker (k) produce 2 units of output per worker.

Because 30 percent of output is saved and invested and 70 percent is consumed, i = 0.6 and c = 1.4.

Because 10 percent of the capital stock depreciates, δk = 0.4.

With investment of 0.6 and depreciation of 0.4, the change in the capital stock is Δk = 0.2.

Thus, the economy begins its second year with 4.2 units of capital per worker.

We can do the same calculations for each subsequent year. Table 7-2 shows how the economy progresses year by year. Every year, because investment exceeds depreciation, new capital is added and output grows. Over many years, the economy approaches a steady state with 9 units of capital per worker. In this steady state, investment of 0.9 exactly offsets depreciation of 0.9, so that the capital stock and output are no longer growing.

Assumptions:  s = 0.3; δ = 0.1; initial k = 4.0

s = 0.3; δ = 0.1; initial k = 4.0 |

||||||

| Year | k | y | c | i | δk | Δk |

| 1 | 4.000 | 2.000 | 1.400 | 0.600 | 0.400 | 0.200 |

| 2 | 4.200 | 2.049 | 1.435 | 0.615 | 0.420 | 0.195 |

| 3 | 4.395 | 2.096 | 1.467 | 0.629 | 0.440 | 0.189 |

| 4 | 4.584 | 2.141 | 1.499 | 0.642 | 0.458 | 0.184 |

| 5 | 4.768 | 2.184 | 1.529 | 0.655 | 0.477 | 0.178 |

| . | ||||||

| . | ||||||

| . | ||||||

| 10 | 5.602 | 2.367 | 1.657 | 0.710 | 0.560 | 0.150 |

| . | ||||||

| . | ||||||

| . | ||||||

| 25 | 7.321 | 2.706 | 1.894 | 0.812 | 0.732 | 0.080 |

| . | ||||||

| . | ||||||

| . | ||||||

| 100 | 8.962 | 2.994 | 2.096 | 0.898 | 0.896 | 0.002 |

| . | ||||||

| . | ||||||

| . | ||||||

| ∞ | 9.000 | 3.000 | 2.100 | 0.900 | 0.900 | 0.000 |

Following the progress of the economy for many years is one way to find the steady-state capital stock, but there is another way that requires fewer calculations. Recall that

Δk = sf(k) −δk.

225

This equation shows how k evolves over time. Because the steady state is (by definition) the value of k at which Δk = 0, we know that

0 = sf(k*) − δk*,

or, equivalently,

This equation provides a way of finding the steady-state level of capital per worker, k*. Substituting in the numbers and production function from our example, we obtain

Now square both sides of this equation to find

k* = 9.

226

The steady-state capital stock is 9 units per worker. This result confirms the calculation of the steady state in Table 7-2.

CASE STUDY

The Miracle of Japanese and German Growth

Japan and Germany are two success stories of economic growth. Although today they are economic superpowers, in 1945 the economies of both countries were in shambles. World War II had destroyed much of their capital stocks. In the decades after the war, however, these two countries experienced some of the most rapid growth rates on record. Between 1948 and 1972, output per person grew at 8.2 percent per year in Japan and 5.7 percent per year in Germany, compared to only 4.1 percent per year in Canada.

Are the postwar experiences of Japan and Germany so surprising from the standpoint of the Solow growth model? Consider an economy in steady state. Now suppose that a war destroys some of the capital stock. (That is, suppose the capital stock drops from k* to k1 in Figure 7-4.) Not surprisingly, the level of output falls immediately. But if the saving rate—the fraction of output devoted to saving and investment—is unchanged, the economy will then experience a period of high growth. Output grows because, at the lower capital stock, more capital is added by investment than is removed by depreciation. This high growth continues until the economy approaches its former steady state. Hence, although destroying part of the capital stock immediately reduces output, it is followed by higher than normal growth. The “miracle’’ of rapid growth in Japan and Germany, as it is often described in the business press, is what the Solow model predicts for countries in which war has greatly reduced the capital stock.

How Saving Affects Growth

The explanation of Japanese and German growth after World War II is not quite as simple as suggested in the preceding case study. Another relevant fact is that both Japan and Germany save and invest a higher fraction of their output than does the United States—the country to which the performance of others is usually compared. To understand more fully the international differences in economic performance, we must consider the effects of different saving rates.

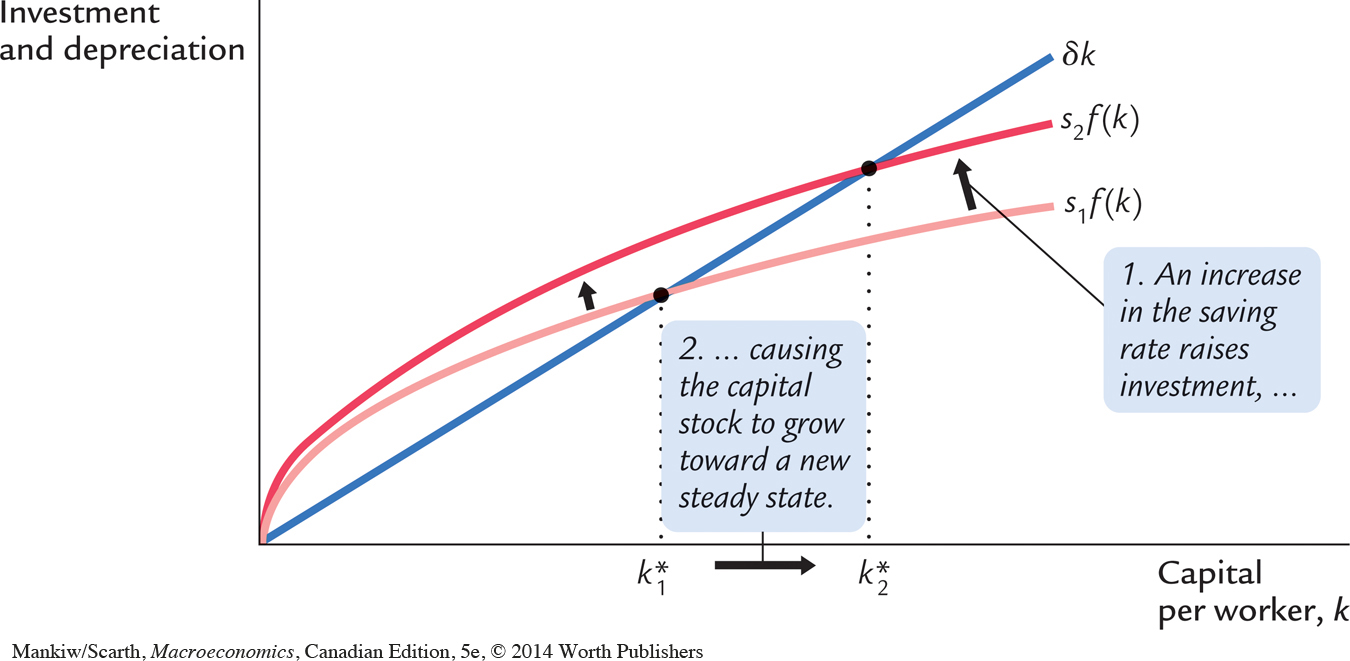

Consider what happens to an economy when its saving rate increases. Figure 7-5 shows such a change. The economy is assumed to begin in a steady state with saving rate s1 and capital stock k*1. When the saving rate increases from s1 to s2, the sf(k) curve shifts upward. At the initial saving rate s1 and the initial capital stock k*1, the amount of investment just offsets the amount of depreciation. Immediately after the saving rate rises, investment is higher, but the capital stock and depreciation are unchanged. Therefore, investment exceeds depreciation. The capital stock will gradually rise until the economy reaches the new steady state k*2, which has a higher capital stock and a higher level of output than the old steady state.

227

The Solow model shows that the saving rate is a key determinant of the steady-state capital stock. If the saving rate is high, the economy will have a large capital stock and a high level of output in the steady state. If the saving rate is low, the economy will have a small capital stock and a low level of output in the steady state. This conclusion sheds light on many discussions of fiscal policy. As we saw in Chapter 3, a government budget deficit can reduce national saving and crowd out investment. Now we can see that the long-run consequences of a reduced saving rate are a lower capital stock and lower national income. This is why many economists are critical of persistent budget deficits.

What does the Solow model say about the relationship between saving and economic growth? Higher saving leads to faster growth in the Solow model, but only temporarily. An increase in the rate of saving raises growth until the economy reaches the new steady state. If the economy maintains a high saving rate, it will also maintain a large capital stock and a high level of output, but it will not maintain a high rate of growth forever. Policies that alter the steady-state growth rate of income per person are said to have a growth effect; we will see examples of such policies in the next chapter. By contrast, a higher saving rate is said to have a level effect, because only the level of income per person—not its growth rate—is influenced by the saving rate in the steady state.

Now that we understand how saving and growth interact, we can more fully explain the impressive economic performance of Germany and Japan after World War II. Not only were their initial capital stocks low because of the war, but their steady-state capital stocks were high because of their high saving rates. Both of these facts help explain the rapid growth of these two countries in the 1950s and 1960s.

228

CASE STUDY

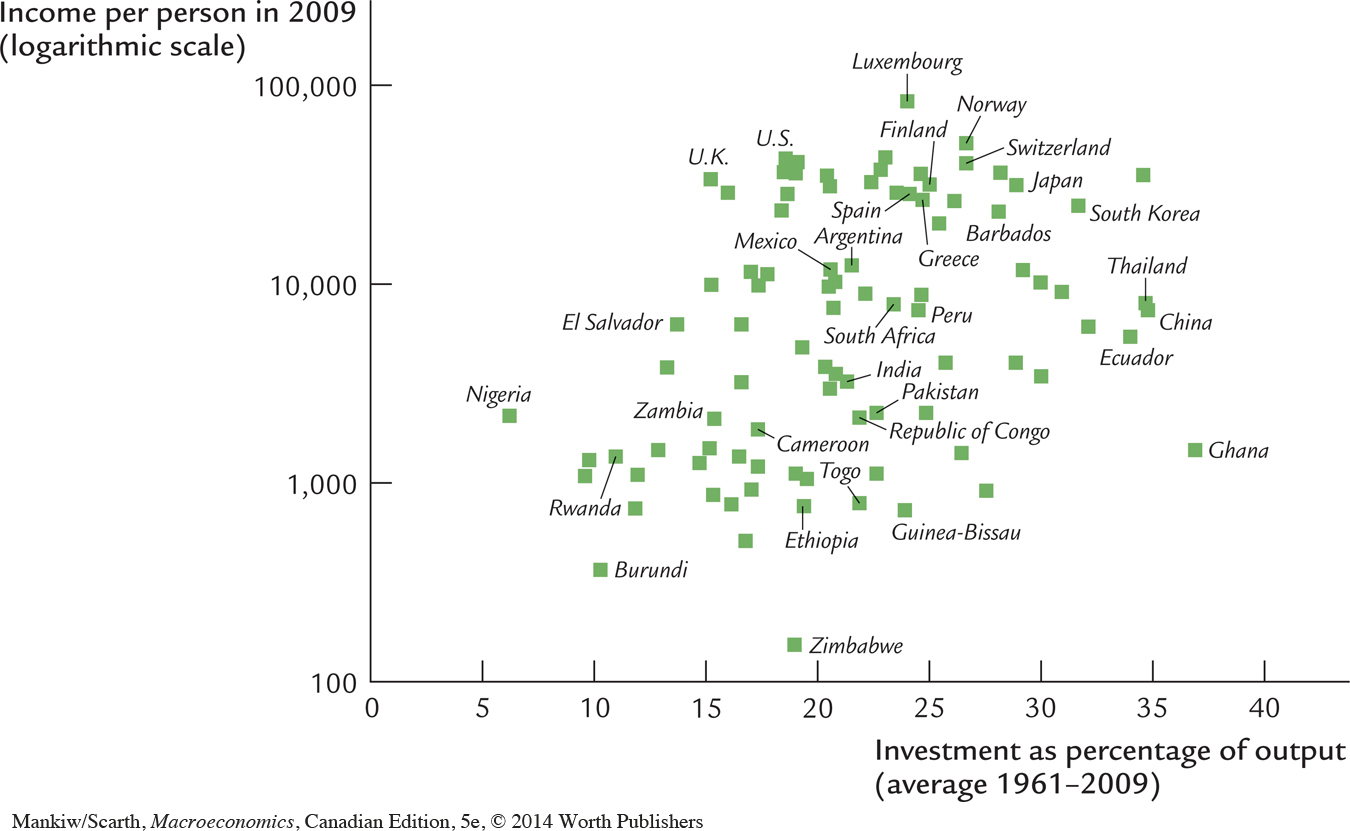

Saving and Investment Around the World

We started this chapter with an important question: Why are some countries so rich while others are mired in poverty? Our analysis has taken us a step closer to the answer. According to the Solow model, if a nation devotes a large fraction of its income to saving and investment, it will have a high steady-state capital stock and a high level of income. If a nation saves and invests only a small fraction of its income, its steady-state capital and income will be low.

Let’s now look at some data to see if this theoretical result in fact helps explain the large international variation in standards of living. Figure 7-6 is a scatterplot of data from about 100 countries. (The figure includes most of the world’s economies. It excludes major oil-producing countries and countries that were communist during much of this period, because their experiences are explained by their special circumstances.) The data show a positive relationship between the fraction of output devoted to investment and the level of income per person. That is, countries with high rates of investment, such as Canada and Japan, usually have high incomes, whereas countries with low rates of investment, such as Eithiopia and Burundi, have low incomes. Thus, the data are consistent with the Solow model’s prediction that the investment rate is a key determinant of whether a country is rich or poor.

229

The strong correlation shown in this figure is an important fact, but it raises as many questions as it resolves. One might naturally ask, why do rates of saving and investment vary so much from country to country? There are many potential answers, such as tax policy, retirement patterns, the development of financial markets, and cultural differences. In addition, political stability may play a role: not surprisingly, rates of saving and investment tend to be low in countries with frequent wars, revolutions, and coups. Saving and investment also tend to be low in countries with poor political institutions, as measured by estimates of official corruption. A final interpretation of the evidence in Figure 7-6 is reverse causation: perhaps high levels of income somehow foster high rates of saving and investment. Unfortunately, there is no consensus among economists about which of the many possible explanations is most important.

The association between investment rates and income per person is strong, and it is an important clue to why some countries are rich and others poor, but it is not the whole story. The correlation between these two variables is far from perfect. The United States and Peru, for instance, have had similar investment rates, but income per person is more than eight times higher in the United States. There must be other determinants of living standards beyond saving and investment. Later in this chapter and in the next one, we return to the international differences in income per person to see what other variables enter the picture.