18.2 Residential Investment

In this section we consider the determinants of residential investment. We begin by presenting a simple model of the housing market. Residential investment includes the purchase of new housing both by people who plan to live in it themselves and by landlords who plan to rent it to others. To keep things simple, however, it is useful to imagine that all housing is owner-occupied.

The Stock Equilibrium and the Flow Supply

There are two parts to the model. First, the market for the existing stock of houses determines the equilibrium housing price. Second, the housing price determines the flow of residential investment.

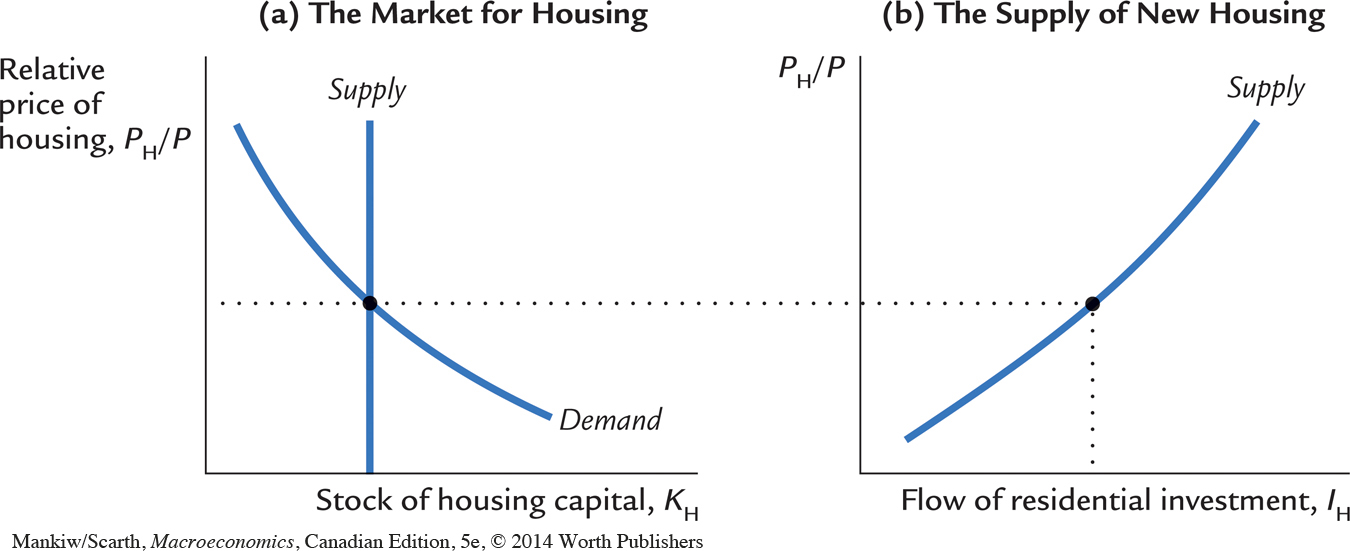

Panel (a) of Figure 18-5 shows how the relative price of housing PH/P is determined by the supply and demand for the existing stock of houses. At any point in time, the supply of houses is fixed. We represent this stock with a vertical supply curve. The demand curve for houses slopes downward, because high prices cause people to live in smaller houses, to share residences, or sometimes even to become homeless. The price of housing adjusts to equilibrate supply and demand.

624

Panel (b) of Figure 18-5 shows how the relative price of housing determines the supply of new houses. Construction firms buy materials and hire labour to build houses, and then sell the houses at the market price. Their costs depend on the overall price level P (which reflects the cost of wood, bricks, plaster, etc.), and their revenue depends on the price of houses PH. The higher the relative price of housing, the greater the incentive to build houses, and the more houses are built. The flow of new houses—residential investment—therefore depends on the equilibrium price set in the market for existing houses.

This model of residential investment is similar to the q theory of business fixed investment. According to q theory, business fixed investment depends on the market price of installed capital relative to its replacement cost; this relative price, in turn, depends on the expected profits from owning installed capital. According to this model of the housing market, residential investment depends on the relative price of housing. The relative price of housing, in turn, depends on the demand for housing, which depends on the imputed rent that individuals expect to receive from their housing. Hence, the relative price of housing plays much the same role for residential investment as Tobin’s q does for business fixed investment.

Changes in Housing Demand

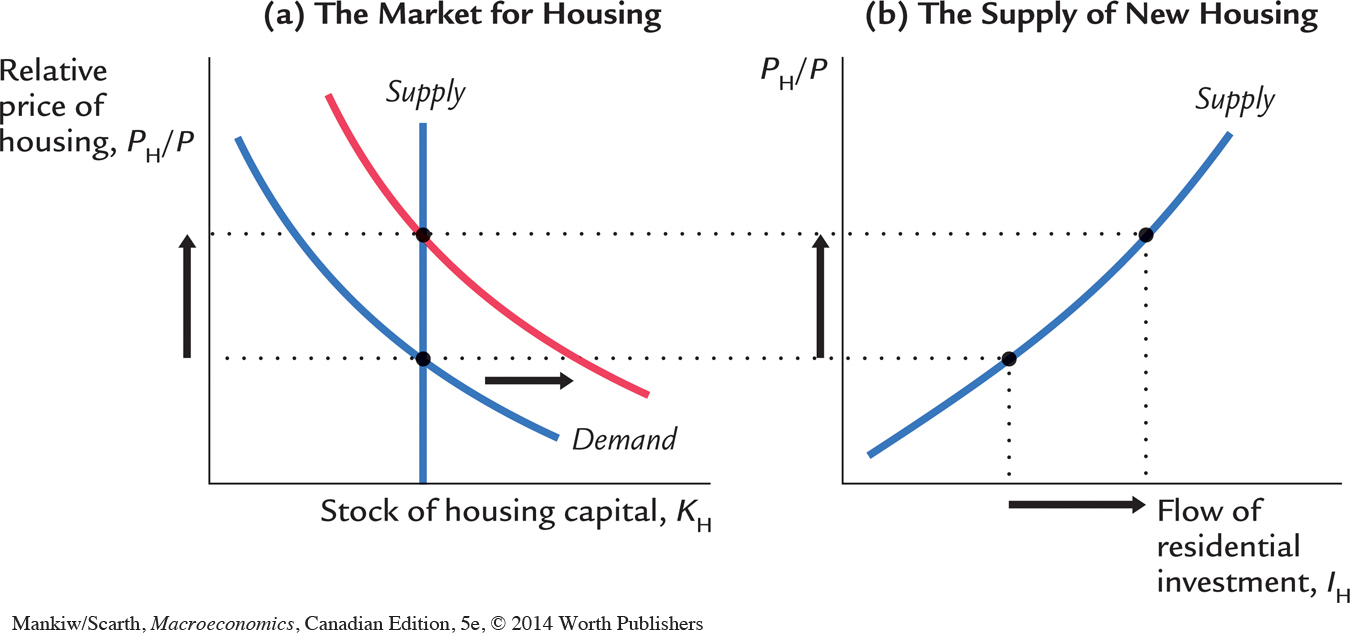

When the demand for housing shifts, the equilibrium price of housing changes, and this change in turn affects residential investment. The demand curve for housing can shift for various reasons. An economic boom raises national income and therefore the demand for housing. A large increase in the population, perhaps because of immigration, also raises the demand for housing. Panel (a) of Figure 18-6 shows that an expansionary shift in demand raises the equilibrium price. Panel (b) shows that the increase in the housing price increases residential investment.

625

One important determinant of housing demand is the real interest rate. Many people take out loans—mortgages—to buy their homes; the interest rate is the cost of the loan. Even the few people who do not have to borrow to purchase a home will respond to the interest rate, because the interest rate is the opportunity cost of holding their wealth in housing rather than putting it in a bank. A reduction in the interest rate therefore raises housing demand, housing prices, and residential investment.

Another important determinant of housing demand is credit availability. When it is easy to get a loan, more households buy their own homes, and they buy larger ones than they otherwise might, thus increasing the demand for housing. When credit conditions become tight, fewer people buy their own homes or trade up to larger ones, and the demand for housing falls.

An example of this phenomenon occurred during the first decade of the 2000s in the United States. Early in this decade, interest rates were low, and mortgages were easy to obtain. Many households with questionable credit histories—called subprime borrowers—were able to get mortgages with small down payments. Not surprisingly, the housing market boomed. Housing prices rose, and residential investment was strong. A few years later, however, it became clear that the situation had gotten out of hand, because many of these subprime borrowers could not keep making their mortgage payments. When interest rates rose and credit conditions tightened, housing demand and housing prices fell dramatically. When the housing market turned down in 2007 and 2008, the result was a significant downturn in the overall economy, which was discussed in a Case Study in Chapter 11.

626

FYI

What Price House Can You Afford?

When someone takes out a mortgage to buy a house in Canada, the bank often places a ceiling on the size of the loan. That ceiling depends on the person’s income and the market interest rate. A typical bank requirement is that the monthly mortgage payment—including both interest and repayment of principal—not exceed 30 percent of the borrower’s monthly income.

Table 18-1 shows how the interest rate affects monthly payments on a $100,000 25-year mortgage, and how the interest rate affects the minimum annual income that is required before banks will grant a mortgage.

| Interest Rate | Monthly Payment | Annual Income Required |

| 5% | $582 | $23,280 |

| 6 | 640 | 25,600 |

| 7 | 700 | 28,000 |

| 8 | 763 | 30,520 |

| 9 | 828 | 33,120 |

| 10 | 894 | 35,760 |

| 11 | 963 | 38,520 |

| 12 | 1,032 | 41,280 |

As you can see, small changes in the interest rate can have a large influence on who can buy a home. For example, an increase in the interest rate from 5 percent to 7 percent raises the monthly payment on a typical mortgage by 20 percent. It also cuts out of the mortgage market all families in the $23,280–$28,000 income range. An increase in the interest rate therefore reduces housing demand, which in turn depresses housing prices and residential investment.

The Tax Treatment of Housing

Just as the tax laws affect the accumulation of business fixed investment, they also affect the accumulation of residential investment. In this case, however, their effects are nearly the opposite. Rather than discouraging investment, as the corporate profit tax does for businesses, the personal income tax encourages households to invest in housing.

One can view a homeowner as a landlord with himself as a tenant. But he is a landlord with a special tax treatment. The Canadian personal income-tax system does not require him to pay tax on the imputed rental income (the rent he “pays” himself). Nor does he have to pay any capital gains tax when the value of his home increases. Many economists have criticized the tax treatment of homeownership. They believe that, because of this subsidy, Canada invests too much in housing compared to other forms of capital.