MONETARY THEORIES

In discussing the theories that justify the use of monetary policy, it is best to differentiate the long run from the short run. We will see that money has no effect on the real economy (such as employment and output) in the long run but can have an effect in the short run.

The Short Run Versus the Long Run: What’s the Difference?

One of the important concepts covered earlier in the book is the comparison between the short-

We now build on the AD/AS model by explaining how changes in the money supply, which directly affect the aggregate demand curve, might change prices and output in the economy. Let’s begin by looking at the long run, which is the analysis most commonly associated with the classical theory.

The Long Run: The Classical Theory

Classical economists focused on long-

equation of exchange The heart of classical monetary theory uses the equation M × V = P × Q, where M is the supply of money, V is the velocity of money (the average number of times per year a dollar is spent on goods and services, or the number of times it turns over in a year), P is the price level, and Q is the economy’s real output level.

A product of the classical theory is the quantity theory of money, which is defined by the equation of exchange:

M × V = P × Q

where M is the supply of money, V is the velocity of money (the average number of times per year a dollar is spent on goods and services), P is the price level, and Q is the economy’s real output level. Note that the right side of the equation—

In the long run, when the economy is at full employment, the implications for monetary policy are straightforward. Because velocity (V) is assumed to be fixed by existing monetary institutions (e.g., the amount of cash you use on a monthly basis is generally consistent), and real aggregate output (Q) is assumed to be fixed at full employment, any change in the money supply (M) will translate directly to a change in prices (P), or in other words, inflation.

IRVING FISHER (1867–1947)

Irving Fisher was one of the ablest mathematical economists of the early 20th century. He was a staunch advocate of monetary reform, and his theories influenced economists as different as John Maynard Keynes and Milton Friedman.

Born in upstate New York in 1867, Fisher studied mathematics, science, and philosophy at Yale University. In 1905 Fisher was in a phone booth in Grand Central Terminal in New York City when someone stole his briefcase, which contained his manuscript of The Nature of Capital and Income, one of the first economics books about the stock market. He rewrote the book over the next year, making copies of each chapter as it was finished and always closing the doors to phone booths after that.

Monetarists owe a great debt to Fisher’s next great book, The Purchasing Power of Money, in which he offered an “equation of exchange”: MV = PT (where T is the number of transactions taking place, or output). Classical economists have used variations of the formula to suggest that inflation is caused by increases in the money supply.

Fisher was prim and straight-

But among his many skills and interests, Fisher was a successful inventor and businessman. In 1925 he patented the “visible card index” system, an early version of the Rolodex, and earned a fortune. Unfortunately, within a few years he would lose everything in the stock market crash of 1929, an event that he famously failed to predict. His insistence of an imminent recovery during the early Depression years caused irreparable damage to a well-

Information from Robert Allen, Irving Fisher: A Biography (Cambridge, MA: Blackwell), 1993.

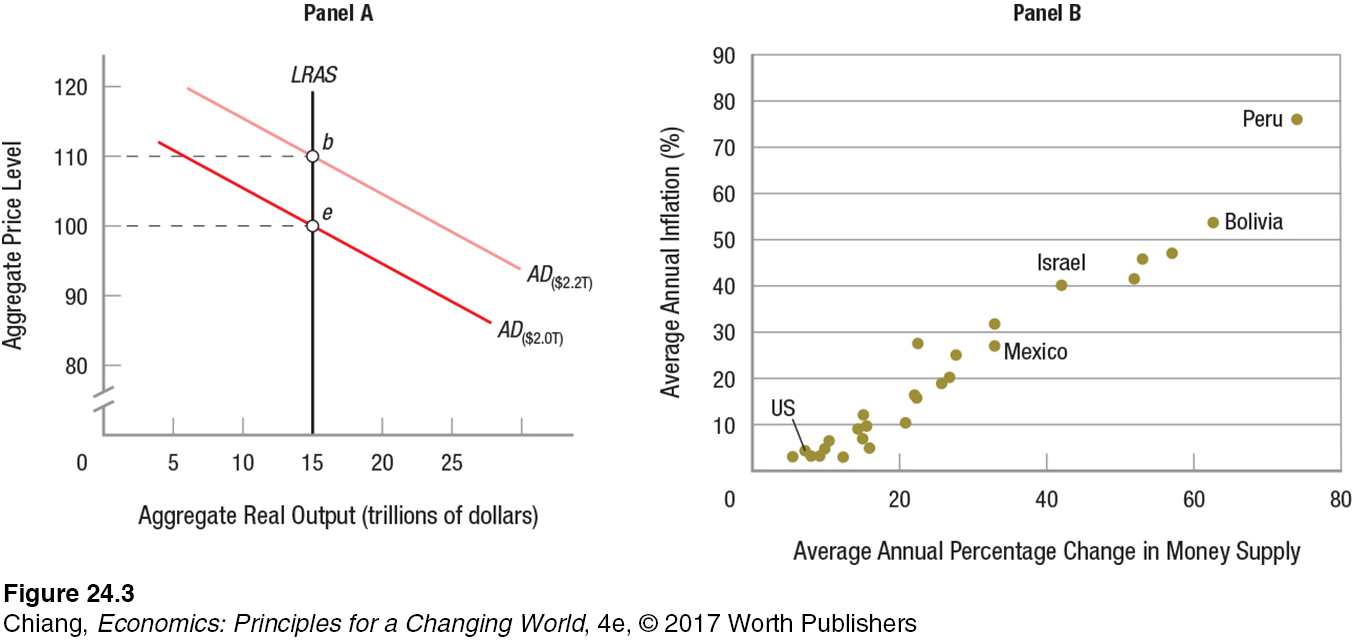

Suppose you sell your grandma’s old LP records on eBay. Last month you listed five records for sale and sold them at an average winning bid of $20 each. Now suppose that this month a 10% increase in the money supply causes more people to want to buy records. If you again list only five records for sale, what will likely happen? There is more money to spend on the same amount of goods. Buyers might bid up the price to, say, $22. In the end, prices rise in the exact proportion to the rise in the money supply. This is the essence of the classical theory—

Panel A of Figure 3 illustrates how the quantity theory works within an aggregate demand and supply model. The economy is initially in long-

The quantity theory of money provides a good explanation of the long-

Short-Run Effects of Monetary Policy

If the short-

Money Illusion and Sticky Wages and Prices Suppose you continue to sell your grandma’s records on eBay, listing five for sale each month. And every month, you notice that the average winning bids keep rising, first to $22, then to $25, then to $30, or even higher. This increase in the sales price makes you happy because you feel richer each month compared to the previous month. You think you are benefiting from the growing popularity of your grandma’s good taste in music.

How would you use your additional income? Most people would spend it by going out to eat more or buying more clothes. This extra spending (by you and everyone who feels richer) results in a temporary increase in economic output. But then you notice that the items you typically buy each month start increasing in price, so much so that despite earning more money, you end up buying about the same amount of goods as you did before. In other words, after prices caught up, you’re no better off than when you made only $20 per record. What you have discovered is that grandma’s records are not growing in popularity. Rather, growth in the money supply is causing an increase in all prices. You misperceived that you were wealthier when you really were not.

MILTON FRIEDMAN (1912–2006)

NOBEL PRIZE

Milton Friedman may be the best-

Born in 1912 in Brooklyn, New York, to poor immigrant parents, Friedman was awarded a scholarship to Rutgers University but paid for his additional expenses by waiting on tables and clerking in a store. He eventually went on to graduate school at the University of Chicago to study economics, and then to Columbia University.

In 1946 he accepted a professorship at the University of Chicago where he delved into the role of money in business cycles. In 1950 Friedman worked in Paris for the Marshall Plan, studying a precursor to the Common Market. He came to believe in the importance of flexible exchange rates between members of the European community.

Friedman’s views were explicitly counter to the Keynesian belief in a range of activist government policies to stabilize the economy. Friedman emphasized the importance of monetary policy in determining the level of economic activity, and advocated a consistent policy of steady growth in the money supply to encourage stability and economic growth.

Friedman was awarded the Nobel Prize in Economics in 1976 for his work on monetary theories and also for his concept of “permanent income,” the idea that people based their savings habits on the typical amount they earn instead of on increases or decreases they may view as temporary.

money illusion A misperception of wealth caused by a focus on increases in nominal income but not increases in prices.

The example above illustrates the misperceptions in wealth that occur when the money supply grows, and is known as money illusion. But money illusion is not the only distinguishing factor between the short run and the long run. Another short-

Keynesian Model Developed by John Maynard Keynes during the Great Depression of the 1930s, Keynesian analysis has had a profound effect on policymakers and economists that continues today. According to Keynesian theory, an increase in the money supply leads more people to buy interest-

However, Keynesians believed that this outcome occurs only when the economy is healthy. During times of recession, people become fearful and don’t buy as much, leading to massive excess capacity for businesses. Reducing interest rates might not lead to greater investment, because firms are unable to sell what they were currently producing. With a decline in business expectations, firms would be reluctant to invest more.

liquidity trap When interest rates are so low, people hold on to money rather than invest in bonds due to their expectations of a declining economy or an unforeseen event such as war.

Further, when interest rates fall to very low levels, Keynes argued that people simply hoard money because it’s not worth holding bonds that pay so little interest. Keynes referred to this phenomenon as the liquidity trap. In a liquidity trap, an increase in the money supply does not result in a decrease in interest rates; thus, there is no change in investment, and consequently no change in income or output. Monetary policy is totally ineffective. This was one reason Keynes argued that fiscal policy, especially government spending, was needed to get the economy out of the Depression.

Monetarist Model Milton Friedman challenged the Keynesian view by arguing that government spending inherent to fiscal policy must be financed either by increased taxation and/or increased borrowing. His monetarist theory states that higher taxation means consumers and firms have less money to consume and invest, while increased borrowing leads to higher interest rates, which also reduces consumption and investment. Thus, monetarists believe that the crowding out effect makes fiscal policy ineffective.

Friedman pioneered the notion that consumption is not only based on income, but also on wealth, an idea he referred to as the permanent income hypothesis.

With Friedman’s approach, when the money supply increases, interest rates fall, and individuals rebalance their asset portfolios by exchanging money for other assets, including real estate and consumer durables such as cars and recreational equipment. Therefore, falling interest rates will lead to higher investment and/or consumption. This leads to an increase in aggregate demand and ultimately an increase in income, output, and/or the price level.

Therefore, monetarists believe that monetary policy can be effective in the short run. But, like classical economists, monetarists believe that an increase in money will ultimately increase prices in the long run. As Milton Friedman famously remarked: “Inflation is always and everywhere a monetary phenomenon.”

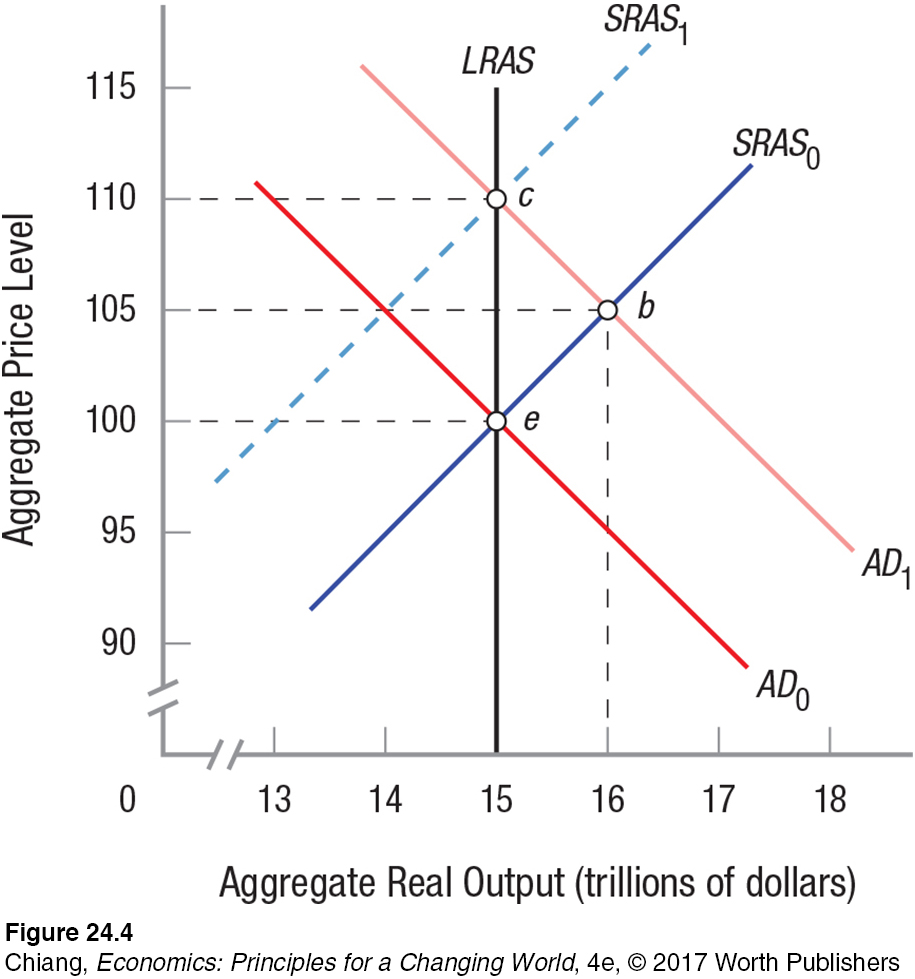

Figure 4 illustrates the monetarist approach that a change in output will occur only in the short run. The economy is initially in long-

Summary of the Effectiveness of Monetary Policy

Let’s summarize the theories of the effectiveness of monetary policy.

Long Run: Changes in the money supply show up directly as increases in the price level because both velocity and output are considered fixed in the equation of exchange (M × V = P × Q). Because classical economists focused on the long run, they saw no use for monetary policy.

Short Run: Keynes believed that when the economy is well below full employment, monetary policy is ineffective because investment is more influenced by business expectations about the economy than interest rates. Further, Keynes suggested that once interest rates get very low, monetary policy might confront a “liquidity trap,” where money is just hoarded. Thus, Keynesians favor fiscal policy to move the economy toward full employment.

Monetarists, on the other hand, do see a role for monetary policy. In the short run, changes in the money supply reduce interest rates, which in turn stimulate both investment and consumption. Consumer spending is related to wealth (not just income), and changes in interest rates lead to changes in consumer spending for durable goods.

A summary of the three theories is provided in Table 1.

| TABLE 1 | SUMMARY OF MONETARY THEORIES | |||||

| Short Run | Long Run | |||||

| Classical Theory | Monetary policy is ineffective. The economy always self- |

Economy self- |

||||

| Keynesian Theory | Fiscal policy is effective, while monetary policy is ineffective in times of deep recession. | Economy adjusts to long- |

||||

| Monetarist Theory | Fiscal policy is ineffective because government spending crowds out consumption and investment, while monetary policy is effective. | Economy adjusts to long- |

||||

Monetary Policy and Economic Shocks

Our discussion thus far suggests that the Fed’s approach to monetary policy should be based on both short-

Economists generally agree that, in the long run, the Fed should focus on price stability because low rates of inflation have been shown to create the best environment for long-

We have seen from the equation of exchange that, in the long run, aggregate supply is vertical and fixed at full employment output. Thus, changes in the supply of money lead to changes in the price level.

But in the short run, demand and supply shocks to the economy may require differing approaches to monetary policy. The direction of monetary policy and its extent depend on whether it focuses on the price level or income and output, and whether the shock to the economy comes from the demand or the supply side.

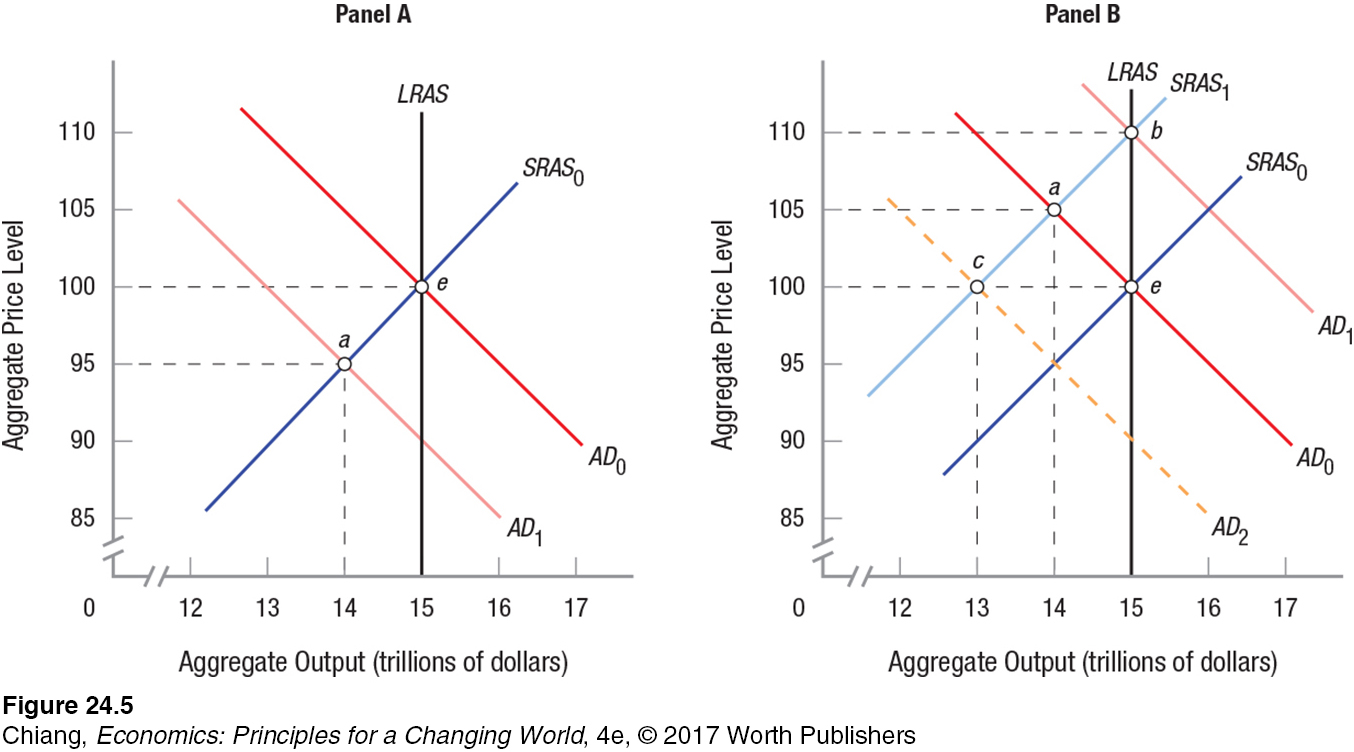

Demand Shocks Demand shocks to the economy can come from reductions in consumer demand, investment, government spending, or exports, or from an increase in imports. For example, the economy faced a demand shock in 2008 when households, fearing unemployment after the housing bubble burst, increased saving and reduced spending. Let’s consider an economy that is initially in full employment equilibrium at point e in panel A of Figure 5. A demand shock then reduces aggregate demand to AD1. At the new equilibrium (point a), the price level and output both fall.

An expansionary monetary policy will increase the money supply, lower interest rates, and thereby shift aggregate demand back to AD0, restoring employment and output to full employment levels. In this case, targeting either a stable price level (100) or the original income and output level ($15 trillion) will bring the economy back to the same point of equilibrium, point e, where both targets are reached.

A positive demand shock produces a corresponding, though opposite, result. The positive demand shock will jolt output and the price level upward. Contractionary monetary policy will reduce both of them, restoring the economy to its original equilibrium.

For demand shocks, therefore, no conflict arises between the twin goals of monetary policy. Not only is the objective of full employment compatible with the objective of stable prices, but by the Fed targeting either one of these objectives, the other objective also will be achieved.

Supply Shocks Supply shocks can hit the economy for many reasons, including changes in resource costs such as a drought causing a rise in food prices, changes in inflationary expectations, or changes in technology. Looking at panel B of Figure 5, let us again consider an economy initially in full employment equilibrium at point e. Assume that a negative shock to the economy, say, a spike in crop prices, shifts short-

This doubly negative result means that a supply shock is very difficult to counter. The Fed could use expansionary monetary policy to shift AD0 to AD1; this would restore the economy to full employment output of $15 trillion (point b), but at an even higher price level (110). Alternatively, the Fed could focus on price level stability, using contractionary monetary policy to shift aggregate demand to AD2, but this would further deepen the recession by pushing output down to $13 trillion (point c).

For a negative supply shock, not only has price level stability worsened, but so has output and income. Contrast this with the situation earlier, when a demand shock worsened the economy for one of its targets, but improved it for the other. Supply shocks are difficult to counteract because of their doubly negative results.

Implications for Short-

CHECKPOINT

MONETARY THEORIES

The classical equation of exchange is M × V = P × Q. In the long run, velocity (V) and output (Q) are assumed to be fixed. Therefore, changes in the money supply translate directly into changes in the price level: ΔM = ΔP.

In the short run, Keynesian monetary analysis suggests that changes in the money supply change interest rates, leading to changes in investment and aggregate demand when the economy is healthy. However, in a deep recession, changes in the money supply have no effect on the real economy.

Monetarists suggest that in the long run, the economy functions in the way that classical economists described, but they see monetary policy affecting interest rates in the short run, which in turn affects investment and/or consumption.

In the long run, the Fed targets price stability. Low rates of inflation are most conducive to long-

run economic health. Monetary policy can offset demand shocks because the objective of full employment is compatible with the objective of stable prices.

Supply shocks present a more challenging problem for monetary policy. A negative supply shock reduces output but increases the price level. Expansionary monetary policy to increase output further increases the price level, and contractionary policy to reduce the price level worsens the recession.

QUESTION: A common debate on dealing with rising national debt involves those who prefer a smaller government (reduced taxation with a dramatic reduction in government spending) versus those who prefer increased government spending funded by higher taxes. Which general theories described in this section best resemble the two sides of the debate?

Answers to the Checkpoint questions can be found at the end of this chapter.

Those who prefer a large government role in the economy would best resemble Keynesians who believe in fiscal policy to increase aggregate demand. Keynesians would support raising tax revenues to reduce the debt. Those who advocate for a smaller government might be considered monetarists, who believe that fiscal policy tends to crowd out consumption and investment. Monetarists would support a reduction in spending to reduce the debt. Those who do not believe in either fiscal or monetary policy interventions might resemble classical theorists who believe that the economy should be left to market forces, and that the government should be as small as possible.