Distinguishing Between Long-Run Growth and Short-Run Fluctuations

When considering changes in real GDP, it is important to distinguish long-run growth from short-run fluctuations due to the business cycle. Both the production possibilities curve model and the aggregate demand–aggregate supply model can help us do this.

The points along a production possibilities curve are achievable if there is efficient use of the economy’s resources. If the economy experiences a macroeconomic fluctuation due to the business cycle, such as unemployment due to a recession, production falls to a point inside the production possibilities curve. On the other hand, long-run growth will appear as an outward shift of the production possibilities curve.

Page 399

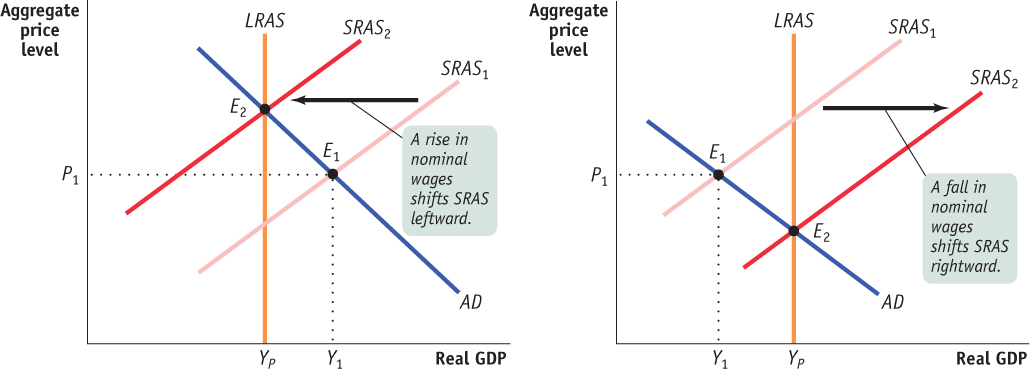

In the aggregate demand–aggregate supply model, fluctuations of actual aggregate output around potential output are illustrated by shifts of aggregate demand or short-run aggregate supply that result in a short-run macroeconomic equilibrium above or below potential output. In both panels of Figure 40.6, E1 indicates a short-run equilibrium that differs from long-run equilibrium due to the business cycle. In the case of short-run fluctuations like these, adjustments in nominal wages will eventually bring the equilibrium level of real GDP back to the potential level. By contrast, we saw in Figure 40.5 that long-run economic growth is represented by a rightward shift of the long-run aggregate supply curve and corresponds to an increase in the economy’s level of potential output.

Page 400

| Figure 40.6 | From the Short Run to the Long Run |

Figure 40.6: From the Short Run to the Long RunIn panel (a), the initial equilibrium is E1. At the aggregate price level, P1, the quantity of aggregate output supplied, Y1, exceeds potential output, YP. Eventually, low unemployment will cause nominal wages to rise, leading to a leftward shift of the short-run aggregate supply curve from SRAS1 to SRAS2 and a long-run equilibrium at E2. In panel (b), the reverse happens: at the short-run equilibrium, E1, the quantity of aggregate output supplied is less than potential output. High unemployment eventually leads to a fall in nominal wages over time and a rightward shift of the short-run aggregate supply curve. The end result is long-run equilibrium at E2.